In the following discussion we shall—for the sake of

exposition—use a very simple example to illustrate the issues

involved in model selection and inference post model selection. These

issues, however, clearly persist also in more complicated situations

such as, e.g., nonlinear models, time series models, etc. Consider the

linear regression model

Suppose now that the parameter of interest is the coefficient α

in (1) and that we are undecided whether or not to include the

regressor xt2 in the model a priori. (The

case where a general linear function A(α,β)′,

e.g., a predictor, rather than α is the quantity of interest is

quite similar and is briefly discussed in Remark 4.5.) In other words,

we have to decide on the basis of the data whether to fit the

unrestricted (full) model or the restricted model with β = 0. We

shall denote the two competing candidate models by U and

R (for unrestricted and restricted,

respectively). For any given value of the parameter vector

(α,β), the most parsimonious true model will be denoted by

M0 and is given by

,

respectively. The least-squares estimator for α in the restricted

model will be denoted by

.

We shall decide between the competing models U and R

depending on whether the test statistic

otherwise. This is a traditional pretest procedure based on

the likelihood ratio, but it is worth noting that in the simple example

discussed here it coincides exactly with Akaike's minimum AIC rule

in case

.

(We note here in passing that there is a close connection between

pretest procedures and information criteria in general; see Remark 4.2.)

In fact, in the present example it seems that there is little choice

with regard to the model selection procedure other than the choice of

c, as it is hard to come up with a reasonable model selection

procedure that is not based on the likelihood ratio statistic (at least

asymptotically). Now that we have defined the model selection procedure

,

the resulting post-model-selection estimator for the parameter of interest

α will be denoted by

The following simple observations will be useful: The finite-sample

distribution of

is a convex combination of the conditional distributions, where the

conditioning is on the outcome of the model selection procedure

where Φ(·) denotes the standard normal cumulative

distribution function (c.d.f.). Cf. Leeb and Pötscher (2003a, Sect. 3.1) and Leeb (2003b, Sect. 3.1).

The subsequent discussion is cast in terms of consistent versus

conservative model selection procedures, because this is entrenched

terminology.8

However, despite this

terminology, one should not lose sight of the fact that we are given

only one sample of

in the present example) and we are

interested in the finite-sample properties of this procedure. Any given

model selection procedure can now equally well be embedded as a member

into a sequence of consistent model selection procedures or into a

sequence of conservative procedures for the purpose of asymptotic

analysis (by appropriately defining the model selection procedures at

the other—fictitious—sample sizes). Of course, the

finite-sample properties of the given model selection procedure are

unaffected by our choice of the embedding asymptotic framework. Hence,

when talking about consistent or conservative sequences of model

selection procedures we are in fact not talking about different

procedures but rather about different asymptotic frameworks and their

comparative (dis)advantages in revealing the finite-sample properties

of a given procedure.

2.1. The Consistent Model Selection Framework

As mentioned in the introduction, proceeding with inference post

model selection “as usual” (i.e., as if the selected model

were given a priori) is often defended by the argument that a

consistent model selection procedure has been used and hence

asymptotically the selected model would coincide with the most

parsimonious true model, supposedly allowing one to use the standard

asymptotic results that apply in case of an a priori fixed model. We

now look more closely at the merit of such an argument.

We assume in this section that the cutoff point c in the

definition of the model selection procedure

is chosen to depend on sample size n such that

.

Then it is well known (see Bauer, Pötscher,

and Hackl, 1988; and also Remark 4.3) that the model selection

procedure is a consistent procedure in the sense that

holds for every α, β; i.e., the probability of revealing the

most parsimonious true model tends to unity as sample size increases.

Because the event

is clearly contained in the event

,

the consistency property expressed in (4) moreover immediately entails

that

holds for every α, β, where

denotes the least-squares estimator in the most parsimonious true model.

Although this latter “estimator” is infeasible as it makes

use of the unknown information whether or not β = 0, relation (5)

shows that the post-model-selection estimator

is a feasible version in the sense that both estimators coincide with

probability tending to unity as sample size increases. An immediate

consequence of (5) is that the (pointwise) asymptotic distributions of

are identical, regardless of whether M0 = U

or M0 = R. This latter property, which is

sometimes called the “oracle” property (Fan

and Li, 2001), obviously holds for post-model-selection estimators

obtained through consistent model selection procedures in general; cf.

Pötscher (1991, Lemma 1) for a formal

statement.

9 This property of consistent

model selection procedures has already been observed by Hannan and

Quinn (1979, p. 191). It has since been

rediscovered several times in special instances; cf. Ensor and Newton

(1988, Theorem 2.1); Bunea (2004, Sect. 4).

So far the preceding discussion seems to support the argument that

proceeding “as usual” with inference post consistent model

selection is justified. In particular, it seems to suggest that the

usual construction of confidence sets remains valid post consistent

model selection. Furthermore, observe that (5) entails that the

post-model-selection estimator

is asymptotically normally distributed and is as “efficient”

as the maximum likelihood estimator based on the full model if the full

model is the most parsimonious true model (i.e., if β ≠ 0), and is

more “efficient” (namely, as “efficient” as the

maximum likelihood estimator based on the restricted model) if the

restricted model is the most parsimonious one (i.e., if β = 0).

This seems too good to be true, and, in fact, it is! Although the

result in (5) is mathematically correct, it is a delusion to believe

that it carries much statistical meaning. Before we explore this in

detail, a little reflection shows that the post-model-selection estimator

is nothing else than a variant of Hodges' so-called superefficient

estimator (cf. Lehmann and Casella, 1998, pp.

440–443).

10 Hodges' estimator

(with a = 0 in the notation of Lehmann and

Casella, 1998) is a post-model-selection estimator based on a model

selection procedure that consistently chooses between an N(0,1)

and an N(θ,1) distribution.

It is remarkable that

estimators such as Hodges' estimator, which was constructed in

1951 as an artificial counterexample to the belief that any

asymptotically normally distributed estimator has an asymptotic

variance that can not fall below the (asymptotic)

Cramér–Rao bound, have nowadays come to some prominence in

the guise of post-model-selection estimators based on a consistent

model selection procedure (and of other related estimators; see Section

3). It is equally remarkable that some of the lessons learned from

Hodges' counterexample seem not to have been received in the model

selection literature in the intervening years:

11 Exceptions are Hosoya (1984),

Shibata (1986), Pötscher (1991), and Kabaila (1995,

1996), who explicitly note this

problem.

The actual finite-sample behavior of

is not properly reflected by the (pointwise) asymptotic results;

in fact, these results can be highly misleading regardless of

the sample size and tend to paint an overly optimistic picture of the

performance of the estimator. Mathematically speaking, the culprit is

nonuniformity (w.r.t. the true parameter vector (α,β)) in the

convergence of the finite-sample distributions to the corresponding

asymptotic distributions; cf. the warning already issued in Pötscher

(1991) in the discussion following Lemma 1 and

also in Section 4, Remark (iii), of that paper.

In the simple example discussed here even a finite-sample analysis is

possible that allows us to nicely showcase the problems involved.

12 For a detailed treatment of the

finite-sample properties of post-model-selection estimators in linear

regression models see Leeb and Pötscher (2003a), Leeb (2003a,

2003b).

We begin with a closer look

at the probability

of selecting the most parsimonious true model. From (3) this probability

equals Φ(c) − Φ(−c) if β = 0,

which—in accordance with (4)—goes to unity as sample size

increases because we have assumed c → ∞ in this section.

In case β ≠ 0, the probability equals

and—again in accordance with (4)—converges to unity as

n → ∞. This is so because

,

so that the arguments of the Φ-functions in this formula converge

either both to +∞ or both to −∞. Nevertheless, the

probability of selecting the most parsimonious true model can be very

small for any given sample size if β ≠ 0 is close to

zero. In that case, we see that this probability is close to 1 −

(Φ(c) − Φ(−c)), which in turn

is close to zero because of c → ∞. More precisely,

if β ≠ 0 equals

,

then—despite (4)—the probability of selecting the most

parsimonious true model in fact converges to zero!

13 Slightly more general conditions under which this is true

are given in Proposition A.1 in Appendix A.

That is, the

consistent model selection procedure is completely “blind”

to certain deviations from the restricted model that are of the order

.

In particular, this reveals that the convergence in (4) is decidedly

nonuniform w.r.t. β: In other words, for the asymptotics to

“kick in” in (4) arbitrarily large sample sizes are needed

depending on the value of the parameter β. This means that

,

although being consistent for M0, is not

uniformly consistent (not even locally). (This is in fact true

for any consistent model selection procedure; see Remark 4.4.)

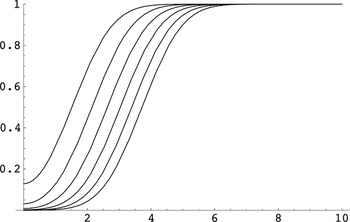

We illustrate

this now numerically. In the following discussion, it proves useful to

write γ as shorthand for

,

i.e., to reparameterize β as

.

As a function of γ, the probability of selecting the unrestricted

model (which is the most parsimonious true model in case β ≠ 0) is

pictured in Figure 1. Recall that with the choice

our model selection procedure coincides with the minimum BIC method.

Finite-sample model selection probability. The probability of

selecting the unrestricted model as a function of

for various values of n, where we have taken

.

Starting from the top, the curves show

for n = 10k for k =

1,2,…,6. Note that

is independent of α and symmetric around zero in β or,

equivalently, γ.

Figure 1 confirms that the probability of

selecting the correct model can be very small if β ≠ 0 is of the

order

and also suggests that this effect even gets stronger as the sample size

increases. The latter observation is explained by the fact that the

probability of selecting the correct model converges to zero not only

for β ≠ 0 of the order

but even for β ≠ 0 of larger order, namely, for β of the form

;

cf. Proposition A.1 in Appendix A. Furthermore, we can also calculate, for

given β ≠ 0, how many data points are needed such that the

probability of selecting the correct (i.e., the unrestricted) model is at

least 0.9, say. With

as in Figure 1, we obtain: If

β/σβ = 1, then a sample of size n

≥ 8 is needed; if

,

one needs n ≥ 42; if

,

one needs n ≥ 207; and if

,

then n ≥ 977 is required. This demonstrates that the required

sample size heavily depends on the unknown β and increases without

bound as β gets closer to zero.

The phenomenon discussed here occurs only if the parameter β ≠

0 is “small” in absolute value in the sense that it goes to

zero of a certain order.

14 It can be

debated whether the β's giving rise to this phenomenon are

justifiably viewed as “small”: The phenomenon can, e.g.,

arise if β ≠ 0 satisfies

with |ζ| < 1 (cf. Proposition A.1 in Appendix A).

Although such sequences of β's converge to zero by the

assumption

maintained in Section 2.1, the “nonzeroness” of any such

β can be detected with probability approaching unity by a standard

test with fixed significance level or equivalently, with fixed cutoff

point, and thus such β's could justifiably be classified as

“far” from zero. (In more mathematical terms,

Pn,α,β is not contiguous w.r.t.

Pn,α,0 for such β's.) By the

way, this also nicely illustrates that the consistent model selection

procedure is (not surprisingly) less powerful in detecting β ≠ 0

compared with the conservative procedure with a fixed value of

c, the reason being that the consistent procedure has to let

the significance level of the test approach zero to asymptotically

avoid choosing a model that is too large. (This loss of power is not

specific to the consistent model selection procedure discussed here but

is typical for consistent model selection procedures in

general.)

It might then be tempting to argue that in such a

case erroneously selecting the restricted model is not necessarily

detrimental as the restricted model is only “marginally”

misspecified: In particular, the estimator

is consistent, even uniformly consistent (cf. Proposition A.9 in Appendix

A), and satisfies

as n → ∞ (where OP is

understood relative to Pn,α,β for

fixed α and β). However, given that the consistent model

selection procedure is “blind” to deviations from the

restricted model of the order

(and even to deviations of larger order), it should not come as a

surprise that the phenomenon discussed previously crops up again in the

distribution of

.

Recall that, as a consequence of (5),

is asymptotically normally distributed with mean zero and variance equal

to the asymptotic variance of the restricted least-squares estimator if

β = 0 and equal to the asymptotic variance of the unrestricted

least-squares estimator if β ≠ 0. However, in finite

samples—regardless of how large—we get a completely different

picture: From Leeb (2003b), we obtain that the

finite-sample density of

is given by

where φ(·) denotes the standard normal probability

density function (p.d.f.). Furthermore, we have used

Δ(a,b) as shorthand for Φ(a +

b) − Φ(a − b), where Φ

denotes the standard normal c.d.f. Note that

Δ(a,b) is symmetric in its first argument. The

finite-sample density of

does not depend on α and is the sum of two terms: The first

term is the density of

multiplied by the probability of selecting the restricted model. The

second term is a “deformed” version of the density of

,

where the deformation factor is given by the 1 −

Δ(·,·)-term.

15 In light

of (2), the first term is actually the conditional density of

given the event that the pretest does not reject multiplied by the

probability of this event. Because the test statistic is independent of

(Leeb and Pötscher, 2003a, Proposition

3.1), this conditional density reduces to the unconditional one.

Similarly, the second term is the conditional density of

given that the pretest rejects multiplied by the probability of this event.

Because the test statistic is typically correlated with

,

the conditional density is not normal, which is reflected by the

“deformation” factor.

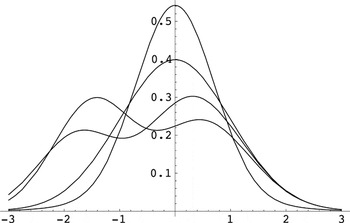

gives an example of the possible shapes of the density of

.

Finite-sample densities. The density

gn,α,β of

for various values of β/σβ. For the graphs,

we have taken n = 100,

,

and σα2 = 1. The four curves correspond to

β/σβ equal to 0, 0.21, 0.25, and 0.5 and are

discussed in the text.

Two of the densities in Figure 2 are

unimodal: The one with the larger mode arises for

β/σβ = 0 and is quite close to the (normal)

density of

corresponding to the restricted model. The reason for this is that the

probability Δ(0,c) of selecting the restricted model is

large, namely, 0.968, and hence the first term in (6) is the dominant

one. The density with the smaller mode arises for

β/σβ = 0.5 and closely resembles the density of

corresponding to the unrestricted model. The reason here is (i) that the

probability of selecting the unrestricted model is large, namely, 0.998,

and hence the second term in (6) is dominant and (ii) that this dominant

term is approximately Gaussian; more precisely, the second term in (6) is

approximately equal to φ(u)(1 − Δ(7 +

0.98u,3)), which differs from φ(u) in absolute value

by less than 0.002. The bimodal densities correspond to the cases

β/σβ = 0.21 and β/σβ =

0.25. In both cases, the left-hand mode reflects the contribution of the

first term in (6) whereas the right-hand mode reflects the contribution of

the second term. The height of the left-hand mode is proportional to the

probability of selecting the restricted model, which is larger for

β/σβ = 0.21 than for

β/σβ = 0.25. In summary, we see that the

finite-sample distribution of

depends heavily on the value of the unknown parameter β

(through β/σβ) and that it is far from its

Gaussian large-sample limit distribution for certain values of β.

The same phenomenon is also found if we repeat the calculations for

other sample sizes n, regardless of how large n is.

In other words: Although the distribution of

is approximately Gaussian for each given (α,β) and

sufficiently large sample size, the amount of data required to achieve

a given accuracy of approximation depends on the unknown β.

In the example presented in Figure 2, a sample

size of 100 appears to be sufficient for the normal approximation

predicted by pointwise asymptotic theory to be reasonably accurate in

the cases β/σβ = 0 and

β/σβ = 0.5, whereas it is clearly

insufficient in case β/σβ = 0.21 or

β/σβ = 0.25.

How can this be reconciled with the result mentioned earlier that

has an asymptotic normal distribution with mean zero and appropriate

variance? The crucial observation again is that this limit result is a

pointwise one; i.e., it holds for each fixed value of the

parameter vector (α,β) individually but does not hold

uniformly w.r.t. (α,β) (in fact, not even locally uniformly):

While it is easy to see that for every

the density gn,α,β(u) given

by (6) converges to the appropriate normal density for each fixed

(α,β), it is equally easy to see (cf. Proposition A.2 in

Appendix A) that (6) has a different asymptotic behavior if, e.g.,

with γ ≠ 0. In this case (6) converges to a shifted

version of the density of the asymptotic distribution of

,

the shift being controlled by γ. Yet another asymptotic behavior

is obtained if we consider

with γn → ∞ (or

γn → −∞) but

γn = o(c). Then

gn,α,β(u) even converges

to zero for every

!

That is, the distribution of

does not “stabilize” as sample size increases

but—loosely speaking—“escapes” to ∞ or

−∞ (depending on the sign of γn);

in fact,

or −∞ in Pn,α,β-probability.

More complicated asymptotic behavior is in fact possible and is described in

Proposition A.2 in Appendix A.

16 A quick

alternative argument showing that the convergence of the finite-sample

c.d.f.s of post-model-selection estimators is typically not uniform

runs as follows: Equip the space of c.d.f.s with a suitable metric

(e.g., a metric that generates the topology of weak convergence).

Observe that the finite-sample c.d.f.s typically depend continuously on

the underlying parameters, whereas their (pointwise) limits typically

are discontinuous in the underlying parameters. This shows that the

convergence can not be uniform.

(To simplify matters the

rather special case ρ

∞ = 0 is excluded from the

preceding discussion; cf. Remark 4.6 for some comments on this case.

However, note that Proposition A.2 also covers the case

ρ

∞ = 0.)

We are now in a position to analyze the actual coverage properties of

confidence intervals that are constructed “as usual,”

thereby ignoring the presence of model selection (this step seemingly

being justified by a reference to (5)). Let

denote the “naive” confidence interval that is given by the

usual confidence interval in the restricted (unrestricted) model if the

restricted (unrestricted) model is selected. That is,

if

and

if

where 1 − η denotes the nominal coverage probability

and zη is the (1 − η/2) quantile of

a standard normal distribution. In view of (2), the actual

coverage probability satisfies

Using the remark in note 15 in the notes section, it is an elementary

calculation to obtain

Note that the coverage probability does not depend on α and is

symmetric around zero as a function of β. Because of (5) and the

attending discussion, pointwise asymptotic theory tells us that the

coverage probability

converges to 1 − η for every (α,β). However, the plots

of the coverage probability given in Figure 3

speak another language.

Finite-sample coverage probabilities. The coverage probability of the

“naive” confidence interval

with nominal confidence level 1 − η = 0.95 as a function of

for various values of n, where we have taken

and ρ = 0.7. The curves are given for n = 10k

for k = 1,2,…,7; larger sample sizes correspond to curves

with a smaller minimal coverage probability.

We see that the actual coverage probability of the

“naive” interval

is often far below its nominal level of 0.95, sometimes falling below 0.3.

Figure 3 also suggests that this phenomenon gets

more pronounced when sample size increases! In fact, it is not difficult to

see that the minimal coverage probability of

converges to zero as sample size increases and not to the nominal coverage

probability 1 − η as one might have hoped for (except possibly in

the relatively special case ρ∞ = 0); cf. also Kabaila

(1995). To see this, note that

where α is arbitrary and γn is chosen

such that γn → ∞ (or

γn → −∞) and

γn = o(c). (The r.h.s. in the

preceding inequality does actually not depend on α in view of

(10).) Because

converges to zero as discussed earlier (cf. Proposition A.1 in Appendix A),

we arrive—using (9) and (10)—at

the last equality being true because

|γn| → ∞ (and because

we have excluded the case ρ∞ = 0).

We finally illustrate the impact of model selection on the (scaled)

bias and the (scaled) mean-squared error of the estimator (again

excluding for simplicity of discussion the case ρ∞

= 0). Let Bias denote the expectation and MSE the

second moment of

.

We discuss the bias first. An explicit formula for the bias can be

obtained from (6) by a tedious but straightforward computation and

is given by

A pointwise (i.e., for fixed (α,β)) asymptotic analysis tells

us that this bias vanishes asymptotically.

17 Although this fits in nicely with (5), it is not a direct

consequence of (5). The crucial point here is that

converges to zero exponentially fast for fixed β ≠ 0; see, e.g.,

Lemma B.1 in Leeb and Pötscher (2003a).

In

Figure

4 we have computed this bias numerically as a function of

.

Note that the bias is independent of α and antisymmetric around

zero in β or, equivalently, γ (and hence is shown only for

γ ≥ 0).

Finite-sample bias. The expectation of

,

i.e., the (scaled) bias of the post-model-selection estimator for α,

as a function of

for various values of n, where we have taken

,

ρ = 0.7, and σα2 = 1. The curves are

given for n = 10k for k =

1,2,…,7; larger sample sizes correspond to curves with larger

maximal absolute biases.

Figure 4 demonstrates that—contrary

to the prediction of pointwise asymptotic theory—the bias can be

quite substantial if β is of the order

and that this effect gets more pronounced as the sample size increases

(the reason for this discrepancy again being nonuniformity in the

pointwise asymptotic results). An asymptotic analysis of (11) using

with γ ≠ 0 shows that the bias converges to

−σα ρ∞γ (see

Proposition A.4 in Appendix A for more information). Note that this

limit corresponds to the “envelope” of the finite-sample

bias curves (for all n) as indicated in Figure 4. Furthermore, if

with γn → ∞ (or

γn → −∞) but

γn = o(c), the asymptotic

analysis in Proposition A.4 even shows that the bias converges to

±∞, the sign depending on the sign of

γn. As a consequence, the maximal absolute bias

in fact grows without bound as sample size increases!

Turning to the MSE we encounter a similar situation. Using

the fact that the test statistic

is independent of

(e.g., Leeb and Pötscher, 2003a,

Proposition 3.1) and that

,

the MSE can be computed explicitly to be

Alternatively, the preceding formula can also be obtained by brute

force integration from the density (6) or from Theorems 2.2 and 4.1 in

Magnus (1999). The MSE is

independent of α. A pointwise asymptotic analysis tells us that

MSE converges to the asymptotic variance

if β = 0 and to the asymptotic variance

if β ≠ 0.

18 Although this is again

in line with (5) it is again not a direct consequence of (5) but follows

from the exponential decay of

for fixed β ≠ 0; cf. note 17. Furthermore, the fact that the

pointwise limit of the MSE coincides with the asymptotic

variance of the infeasible “estimator”

is not particular to the consistent model selection procedure discussed

here. It is true for consistent model selection procedures in general,

provided the probability of selecting an incorrect model converges to

zero sufficiently fast, which is typically the case; see Nishii (1984) for some results in this direction. Of

course, being only pointwise limit results, these results are subject

to the criticism put forward in the present paper.

Again,

however, the finite-sample mean-squared error exhibits a totally

different behavior, regardless how large sample size is (as a result of

nonuniformity in the pointwise asymptotics). This can be gleaned from

Figure 5: The maximal mean-squared error is

much larger than the mean-squared error of the unrestricted

least-squares estimator that is constant and equal to

σ

α2 = 1. As

Figure

5 suggests, the maximal mean-squared error diverges to infinity

as sample size increases, whereas the mean-squared error of

stays bounded (it converges to σα,∞2).

This is well known for the Hodges estimator (e.g., Lehmann and Casella, 1998, p. 442). For the mean-squared

error of

this follows of course immediately from the fact noted previously that

the bias diverges to ±∞ when setting

with γn → ∞ (or

γn → −∞) but

γn = o(c). (The phenomenon

that the maximal absolute bias and hence the maximal mean-squared error

diverge to infinity holds for post-model-selection estimators based on

consistent model selection procedures in general; see Remark 4.1,

Appendix C; and Yang (2003).)

Finite-sample mean-squared error. The second moment of

,

i.e., the (scaled) mean-squared error of the post-model-selection estimator

for α, as a function of

for various values of n, where we have taken

,

ρ = 0.7, and σα2 = 1. The curves are

given for n = 10k for k =

1,2,…,7; larger sample sizes correspond to curves with larger

maximal mean-squared error.

2.2. The Conservative Model Selection Framework

Generally speaking, post-model-selection estimators based on

conservative model selection procedures are subject to phenomena

similar to the ones observed in Section 2.1 for post-model-selection

estimators based on consistent procedures. In particular, the

finite-sample behavior of both types of post-model-selection estimators

is governed by exactly the same formulas, because the finite-sample

behavior is clearly not much impressed by what we fancy about the

behavior of the model selection procedure at fictitious sample sizes

other than n (e.g., what we fancy about the behavior of the

cutoff point c as a function of n). Cf. the

discussion immediately preceding Section 2.1. Not surprisingly, some

differences arise in the asymptotic theory.

In this section we consider the same model selection procedure and

post-model-selection estimator

as before, except that we now assume the cutoff point c to be

independent of sample size n.

19 We

could allow more generally for a sample-size-dependent c that,

e.g., converges to a positive real number. See Leeb and Pötscher

(2003a, Remark 6.2).

This results in a

conservative model selection procedure (that is not consistent).

20 For a detailed treatment of the

finite-sample and asymptotic properties of post-model-selection

estimators based on a conservative model selection procedure see

Pötscher (1991), Leeb and Pötscher

(2003a), and Leeb (2003a, 2003b).

As just noted, the finite-sample distribution, the expectation, and the

second moment of

are again given by (6), (11), and (12), respectively. Also, the

model selection probabilities and the coverage probability of the

“naive” confidence interval are given by the same formulas

as before. As a consequence, all conclusions drawn from the

finite-sample formulas in Section 2.1 remain valid here: The

finite-sample distribution of the post-model-selection estimator is

often decidedly nonnormal, and the standard asymptotic approximations

derived on the presumption of an a priori given model are

inappropriate. In particular, the actual coverage probability of the

“naive” confidence interval is often much smaller than the

nominal coverage probability. Finally, the bias can be substantial, and

the mean-squared error can by far exceed the mean-squared error of the

unrestricted estimator.

We briefly discuss the asymptotic behavior next.

21 Similar as for consistent model selection procedures in

fact all accumulation points of the model selection probabilities, the

finite-sample distributions, the bias, and the mean-squared error can

be characterized by a subsequence argument similar to Remark A.8; cf.

also Leeb and Pötscher (2003a, Remark

4.4(i)), and Leeb (2003b, Remark

5.5).

A much more detailed treatment covering more general

model selection procedures and more general models can be found in

Pötscher (

1991), Leeb and Pötscher

(

2003a), and Leeb (

2003a,

b). The pointwise

limiting behavior of the model selection probabilities can be easily read

off from the finite-sample formula (3):

if

,

reflecting the fact that the model selection procedure is conservative

but not consistent. As in the case of consistent model selection

procedures, this convergence is not uniform w.r.t. β. In contrast

to consistent model selection procedures (cf. Proposition A.1 in

Appendix A), the behavior under sample-size-dependent parameters

(αn,βn) is quite

simple: If

,

then

.

(If

,

then the limit is zero; i.e., the asymptotic behavior is identical to

the asymptotic behavior under fixed β ≠ 0.) In particular, the

asymptotic analysis confirms what we already know from the finite-sample

analysis, namely, that the probability of erroneously selecting the

restricted model can be substantial, namely, if |γ| is

small. However, in contrast to consistent model selection procedures,

this probability does not converge to unity as sample size increases.

It is also interesting to note that deviations from the restricted model

such as

with |ζ| < 1 and cn

→ ∞,

,

that can not be detected by a consistent model selection procedure using

cutoff point cn (cf. Proposition A.1 and note

14 in the notes section) can be detected with probability approaching unity

by a conservative procedure using a fixed cutoff point c.

Consequently and not surprisingly, conservative model selection

procedures are more powerful than consistent model selection procedures

in the sense that they are less likely to erroneously select an

incorrect model for large sample sizes. (Needless to say this advantage

of the conservative procedure is paid for by a larger probability of

selecting an overparameterized model.)

Turning to the post-model-selection estimator

itself, it is obvious that now conditions (4) and (5) are no longer

satisfied;

22 Nevertheless, it is easy to

see that

is consistent (cf. Pötscher, 1991, Lemma 2)

and, in fact, is uniformly consistent; see Proposition B.1 in Appendix

B.

as a consequence, and in contrast to the case of consistent

model selection procedures, the pointwise asymptotic distribution now

captures some of the effects of model selection and no longer coincides

with the usual asymptotic distribution that applies in the absence of model

selection. This can easily be seen from (2): Whereas in the case of

consistent model selection procedures, regardless of the value of β,

only one of the two terms in (2) survives asymptotically and the

corresponding conditioning event becomes a set of probability one

asymptotically and hence has no effect, for conservative procedures both

terms do not vanish in the limit if β = 0. Hence, the pointwise

asymptotic limit captures some of the effects of the model selection step,

at least in the case when the restricted model is correct. (In that sense

the asymptotic framework that views a given model selection procedure as

embedded in a sequence of conservative procedures has some advantage

over the framework considered in Section 2.1.) More precisely, the

pointwise asymptotic distribution of

has a density given by

σα,∞−1φ(u/σα,∞)

if β ≠ 0 and given by

if β = 0. Note that (13) bears some resemblance to the

finite-sample distribution (6). However, the pointwise asymptotic

distribution does not capture all the effects present in the

finite-sample distribution, especially if β ≠ 0; in particular,

the convergence is not uniform w.r.t. β (except in trivial cases

such as ρ∞ = 0); cf. Corollary 5.5 in Leeb and

Pötscher (2003a), Remark 6.6 in Leeb and

Pötscher (2003b), and note 16. A much

better approximation, capturing all the essential features of the

finite-sample distribution, is obtained by the asymptotic distribution

under sample-size dependent parameters

(αn,βn) with

:

This asymptotic distribution has a density of the form

This follows either as a special case of Proposition 5.1 of Leeb

(2003b) (cf. also Leeb and

Pötscher, 2003a, Proposition 5.3 and Corollary 5.4) or can

be gleaned directly from (6). (If

,

then the limit has the form

σα,∞−1φ(u/σα,∞).)

23 Here the convergence of the finite-sample

distribution to the asymptotic distribution is w.r.t. total variation

distance.

Observe that (14) follows the same formula as the

finite-sample density (6), except that σ

α and ρ

have been replaced by their respective limits

σ

α,∞ and ρ

∞ and that

has been replaced by γ.

Consider next the asymptotic behavior of the actual coverage

probability of the “naive” confidence interval

given by (7) and (8). The pointwise limit of the actual coverage

probability has been studied in Pötscher (1991, Sect. 3.3). In contrast to the case of

consistent model selection procedures, it turns out to be less than the

nominal coverage probability in case the restricted model is correct.

However, this pointwise asymptotic result, although hinting at the

problem, still gives a much too optimistic picture when compared with

the actual finite-sample coverage probability. The large-sample minimal

coverage probability of the “naive” confidence interval has

been studied in Kabaila and Leeb (2004).

Although it does not equal zero as in the case of consistent model

selection procedures, it turns out to be often much smaller than the

nominal coverage probability 1 − η (as in Figure 3); see Kabaila and Leeb (2004) for more details.

We finally turn to the bias and mean-squared error of

.

Under the sequence of parameters

(αn,βn) with

,

it is readily seen from (11) that the bias converges to

The pointwise asymptotics corresponds to the cases γ = 0 and

γ = ±∞ (with the convention that

±∞Δ(±∞,c) = 0 and

φ(±∞) = 0) and results in a zero limiting bias.

However, the maximal bias can be quite substantial if β is of the

order

.

In contrast to the case of consistent model selection procedures, the

maximal bias does not go to infinity (in absolute value) as n

→ ∞ but remains bounded. (It is perhaps somewhat

ironic—although not surprising—that consistent model

selection procedures that look perfect in a pointwise asymptotic

analysis lead in fact to more heavily distorted post-model-selection

estimators than conservative model selection procedures.) The limiting

mean-squared error under

(αn,βn) as before is

easily seen to be given by

the pointwise asymptotics again corresponding to the cases γ = 0

and γ = ±∞ (with the convention that

∞Δ(±∞,c) = 0 and

±∞φ(±∞) = 0). In contrast to the case of

consistent model selection procedures, the pointwise limit of

MSE captures some (but not all) of the effects of model

selection and hence no longer coincides with the asymptotic variance of

the infeasible “estimator”

.

Also, in contrast to the case of consistent model selection procedures,

the maximal mean-squared error does not go off to infinity as n

→ ∞, but rather it remains bounded; cf. also Remark 4.1.

2.3. Can One Estimate the Distribution of

Post-Model-Selection Estimators?

It transpires from the preceding discussion that the finite-sample

distributions (and also the asymptotic distributions) of

post-model-selection estimators depend on unknown parameters (i.e.,

β in the example discussed in this paper), often in a complicated

fashion. For inference purposes, e.g., for the construction of

confidence sets, estimators for these distributions would be desirable.

Consistent estimators for these distributions can typically be

constructed quite easily, e.g., by suitably replacing unknown

parameters in the large-sample limit distributions by estimators: In

the case of the consistent model selection procedure discussed in

Section 2.1 a consistent estimator for the finite-sample distribution of

is simply given by the normal distribution

N(0,σα2(1 −

ρ2)), i.e., by the distribution of

,

and by N(0,σα2), i.e., by the

distribution of

.

However, recall from Section 2.1 that the finite-sample distribution of

the post-model-selection estimator is not uniformly close to its pointwise

asymptotic limit. Hence the suggested estimator (being identical with

the pointwise asymptotic distribution except for replacing

σα,∞2 and

ρ∞2 by

σα2 and ρ2)

will—although being consistent—not be close to the

finite-sample distribution uniformly in the unknown parameters, thus

providing a rather useless estimator. In the case of conservative model

selection procedures consistent estimators for the finite-sample

distribution of the post-model-selection estimator can also be

constructed from the pointwise asymptotic distribution by suitably

plugging in estimators for unknown quantities; see Leeb and

Pötscher (2003b, 2004). However, again these estimators will be

quite useless for the same reason: As discussed in Section 2.2, the

convergence of the finite-sample distributions to their (pointwise)

large-sample limits is typically not uniform with respect to the

underlying parameters, and there is no reason to believe that this

nonuniformity will disappear when unknown parameter values in the

large-sample limit are replaced by estimators.

A natural reaction to the preceding discussion could be to try the

bootstrap or some related resampling procedure such as, e.g.,

subsampling. Consider first the case of a consistent model selection

procedure. Then, in view of (4) and (5), the bootstrap that resamples

from the residuals of the selected model certainly provides a

consistent estimator for the finite-sample distribution of the

post-model-selection estimator. Note that the consistent estimator

described in the preceding paragraph can be viewed as a (parametric)

bootstrap. The discussion in the previous paragraph then, however,

suggests that such estimators based on the bootstrap (or on other

resampling procedures such as subsampling), despite being consistent,

will be plagued by the nonuniformity issues discussed earlier. Next

consider the case where the model selection procedure is conservative

(but not consistent). Then the bootstrap will typically not even

provide consistent estimators for the finite-sample distribution of the

post-model-selection estimator, as the bootstrap can be shown to stay

random in the limit (Kulperger and Ahmed,

1992; Knight, 1999, Example 3):24

Kilian (1998)

claims the validity of a bootstrap procedure in the context of

autoregressive models that is based on a conservative model selection

procedure. Hansen (2003) makes a similar

claim for a stationary bootstrap procedure in the context of a

conservative model selection procedure. The preceding discussion

intimates that both these claims are at least unsubstantiated.

Basically the only way one can coerce the bootstrap into delivering a

consistent estimator is to resample from a model that has been selected

by an

auxiliary consistent model selection procedure. (The

construction of consistent estimators in Leeb and Pötscher,

2003b,

2004, alluded to

previously basically follows this route.) In contrast, subsampling will

typically deliver consistent estimators. However, the discussion in the

preceding paragraph strongly suggests that any such estimator will

again suffer from the nonuniformity defect.

A natural question then is how estimators (not necessarily derived

from the asymptotic distributions or from resampling considerations)

can be found that do not suffer from the nonuniformity defect. In other

words, we are asking for estimators

of the finite-sample c.d.f.

that are uniformly consistent, i.e., that satisfy for every

and every δ > 0

However, it turns out that no estimator

can satisfy this requirement (except possibly in the trivial case where

ρ∞ = 0). For conservative model selection

procedures this is proved in Leeb and Pötscher (2003a, 2004) in a more

general framework, including model selection by AIC from a quite

arbitrary collection of linear regression models. For a consistent

model selection procedure such a result is given in Leeb and

Pötscher (2002, Sect. 2.3). In fact,

these papers show that the situation is even more dramatic: For every

consistent estimator

even

holds for suitable δ > 0, and this result is even local in the

sense that it holds also if the supremum in the preceding display

extends only over suitable balls that shrink at rate

.

25 Similar “impossibility” results apply to

estimators of the model selection probabilities; see Leeb and

Pötscher (2004) in the case of

conservative procedures; for consistent procedures this argument can be

easily adapted by making use of Proposition A.1.

(These

“impossibility” results hold for randomized estimators of

Gn,α,β also.)

The preceding “impossibility” results establish in

particular that any proposal to estimate the distribution of

post-model-selection estimators by whatever resampling procedure

(bootstrap, subsampling, etc.) is doomed as any such estimator is

necessarily plagued by the nonuniformity defect (if it is consistent at

all). On a more general level, an implication of the preceding results

is that assessing the variability of post-model-selection estimators

(e.g., the construction of valid confidence intervals post model

selection) is a harder problem than perhaps expected.26

The confidence interval suggested in Hjort

and Claeskens (2003, p. 886) does not provide

a solution to this problem. As pointed out in Remark 3.5 of Kabaila and

Leeb (2004), the proposed interval

(asymptotically) coincides with the classical confidence interval

obtained from the overall model.