Introduction

This study explores whether the relationships between internal social capital – both family social capital (the strength of relationships among family members) and non-family social capital (the strength of relationships among non-family members) – and innovation are strengthened or weakened by family involvement in the top management team (TMT) of family firms.

In the business literature, social capital has been identified as social resources that firms utilise to achieve sustainable success and competitive advantage. Thus, social capital appears to be linked to the development of firms’ innovation, as it supports creativity and inspires new knowledge and ideas (Youndt, Subramaniam, & Snell, Reference Youndt, Subramaniam and Snell2004; Subramaniam & Youndt, Reference Subramaniam and Youndt2005; Aragón-Correa, García-Morales, & Cordón-Pozo, Reference Aragon-Correa, García-Morales and Cordon-Pozo2007). Innovation is essentially a collaborative effort, and social capital arises as a result of collaboration among people who share their ideas, perspectives, and trust through networks of interaction and learning (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Wright, Cullen, & Miller, Reference Wright, Cullen and Miller2001; Adler & Kwon, Reference Adler and Kwon2002; Yli-Renko, Autio, & Tontti, Reference Yli-Renko, Autio and Tontti2002; Moran, Reference Moran2005; Subramaniam & Youndt, Reference Subramaniam and Youndt2005). According to Subramaniam and Youndt (Reference Subramaniam and Youndt2005), communication, the fluid diffusion of information, and the sharing and assimilation of knowledge may be the key not only for creating innovative capabilities but also for developing ‘dynamic capabilities’ that enable organisations to shift their competitive focus and achieve new forms of competitive advantage (Teece, Pisano, & Shuen, Reference Teece, Pisano and Shuen1997; Blyler & Coff, Reference Blyler and Coff2003).

Social capital in family firms is especially important because the strong relational ties among family members could significantly alter relationships within the organisation (internal social capital) and between the organisation and external parties (external social capital) (Adler & Kwon, Reference Adler and Kwon2002; Arregle, Hitt, Sirmon, & Very, Reference Arregle, Hitt, Sirmon and Very2007). The influence of social capital on a family firm’s innovation has been extensively discussed, since social capital is a tacit resource and, consequently, is difficult to manage and measure (Carmona-Lavado, Cuevas-Rodríguez, & Cabello-Medina, Reference Carmona-Lavado, Cuevas-Rodriguez and Cabello-Medina2010). While some prior studies highlight the potential of organisational relationships to stimulate innovation (e.g., Le Breton-Miller & Miller, Reference Le Breton-Miller and Miller2006; Pearson, Carr, & Shaw, Reference Pearson, Carr and Shaw2008; Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2014), others suggest that such relationships could constrain innovation and cause competitive disadvantages (e.g., Dunn, Reference Dunn1996; Adler & Kwon, Reference Adler and Kwon2002; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015). Thus, social capital as a driver of innovation in family firms is a promising research area since the effects of family involvement and interpersonal relationships on innovation are not well understood yet (De Massis, Kotlar, & Frattini, Reference De Massis, Kotlar and Frattini2013c).

Consistent with social capital theory and following the notion of relational embeddedness, in this study, we focus on internal social capital (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Yli-Renko, Autio, & Sapienza, Reference Yli-Renko, Autio and Sapienza2001), which is defined as the knowledge embedded within, available through, and utilised in the interactions among individuals and their interrelationship networks inside family firms. We maintain that feelings of mutual identification and unwritten social norms of reciprocity could help in building social capital relations among family firm members. In this sense, intra-firm collaboration is considered important for innovations (e.g., Gupta, Tesluk, & Taylor, Reference Gupta, Tesluk and Taylor2007). However, prior studies that analyse the effect of internal social capital on innovation have taken into account only family social capital (e.g., Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Tsai & Ghoshal, Reference Tsai and Ghoshal1998; Moran, Reference Moran2005; Subramaniam & Youndt, Reference Subramaniam and Youndt2005). To the best of the authors’ knowledge, very few studies analyse the relationships between internal social capital and innovation in the context of family firms by taking into account the two main social groups that there exist within most family firms, namely, the family members’ group and the non-family members’ group (e.g., McCollom, Reference McCollom1992; Ram, Reference Ram2001; Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007), which do not have necessarily have similar dynamics, relationships, and interactions (Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2013, Reference Sanchez-Famoso, Maseda and Iturralde2014). Moreover, it is estimated that over 80% of the people employed in family businesses are not family members (Mitchell, Morse, & Sharma, Reference Mitchell, Morse and Sharma2003).

The extant literature highlights that family firms cannot be interpreted to be homogenous in terms of strategic behaviour (Botero, Thomas, Graves, & Fediuk, Reference Botero, Thomas, Graves and Fediuk2013), given that strategic decision making in family firms is strongly influenced by the family (Sciascia & Mazzola, Reference Sciascia and Mazzola2008; Nordqvist & Melin, Reference Nordqvist and Melin2010; Basco & Voordeckers, Reference Basco and Voordeckers2015). The TMT is responsible for innovation-related decisions in firms (Talke, Salomo, & Rost, Reference Talke, Salomo and Rost2010; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015), and its composition may influence innovation processes (Hambrick & Mason, Reference Hambrick and Mason1984; Hambrick, Reference Hambrick2007), especially in family small and medium-sized enterprises (SMEs), where senior managers not only ratify and direct their firm’s strategy, but also participate more directly in the day-to-day implementation of that strategy (Lubatkin, Simsek, Ling, & Veiga, Reference Lubatkin, Simsek, Ling and Veiga2006; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015).

Building on these arguments from prior research, this study explores whether the relationships between innovation and internal social capital (both family social capital and non-family social capital) are strengthened or weakened by family involvement in the TMT of family firms, since the senior managers are responsible for innovation-related decisions, and family involvement in management reflects family participation in strategic decision making.

This study seeks to contribute to the debate on social capital as a determinant of innovation in family firms by exploring two research questions. (1) Is the relationship between family social capital and innovation strengthened or weakened by family involvement in TMT? and (2) Is the relationship between non-family social capital and innovation strengthened or weakened by family involvement in TMT? These questions are important because the results of this study could contribute to an understanding of how innovation could be optimised within both family and non-family groups. Therefore, our study contributes to the literature on social capital, family firms, and TMT in Continental European non-listed family firms by addressing calls for empirical testing (Basco & Voordeckers, Reference Basco and Voordeckers2015; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015), and providing evidence regarding the link between internal social capital and family firm innovation, as well as the extent to which TMT affects the relationships between both family and non-family social capital towards innovation in family firms, which has seldom been empirically tested.

Our analysis is based on the data from 344 questionnaires completed by managers in 172 Spanish family firms. This sample, which is designed to be representative of the Spanish economy, comes from medium-sized firms, all of which are non-listed. We treat internal social capital and innovation at the firm level (Leana & Van Buren, Reference Leana and Van Buren1999), reflecting the perceptions of individual managers about the collective relationships and innovation in their firms (De Clercq, Dimov, & Thongpapanl, Reference De Clercq, Dimov and Thongpapanl2013). Our study makes an important contribution because it analyses the effect of internal social capital, taking into account both family and non-family social capital, on family firm innovation, as well as how those relationships are moderated by family management. This issue is especially important because of the central roles both family and non-family members play in family firms (e.g., Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007; Sharma, Reference Sharma2008) and the fact that these groups coexist in the majority of family firms (e.g., Mitchell, Morse, & Sharma, Reference Mitchell, Morse and Sharma2003; Vandekerkhof, Steijvers, Hendriks, & Voordeckers, 2015). Therefore, we enhance the understanding of the family-specific factors that affect innovation in family firms. In particular, we explore whether high family involvement in management makes it more or less possible to identify, understand, and use the specialisations of family and non-family members for innovation. Consequently, we test heterogeneity across family firms (Melin & Nordqvist, Reference Melin and Nordqvist2007; De Massis, Kotlar, Chua, & Chrisman, Reference De Massis, Kotlar, Chua and Chrisman2014; Nordqvist, Sharma, & Chirico, Reference Nordqvist, Sharma and Chirico2014; Chrisman, Chua, De Massis, Frattini, & Wright, Reference Chrisman, Chua, De Massis, Frattini and Wright2015) and offer an enriched perspective on the development of innovation in family firms with high or low family involvement in management. Thus, this study contributes to the family business literature by examining different types of family firms instead of treating them as a homogeneous group.

The rest of this paper is organised as follows. In the following section, we discuss the concept and dimensions of internal social capital in the context of family firms, innovation, and family involvement in management. In the third section, we propose and test a specific model to explain the role of family involvement in management with regard to the relationships between firm innovation and both family social capital and non-family social capital. In the final section, we discuss the results and the main conclusions, as well as their implications, and present directions for future research.

Theoretical Framework

Social capital, firm innovation, and family management

According to Coleman (Reference Coleman1990), Nahapiet and Ghoshal (Reference Nahapiet and Ghoshal1998), and Tsai and Ghoshal (Reference Tsai and Ghoshal1998), the concept of social capital encompasses the social interactions, network ties, trusting relations, and value systems that facilitate creativity in a group context. Social capital reflects the value of relationships and includes the interrelationship network and the assets that could be mobilised through that network (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Pearson, Carr, & Shaw, Reference Pearson, Carr and Shaw2008; Carr, Cole, Kirk-Ring, & Blettner, Reference Carr, Cole, Kirk-Ring and Blettner2011). It involves relationships among the individuals working in the organisation (internal social capital) as well as between the organisation and external parties (external social capital) (Adler & Kwon, Reference Adler and Kwon2002).

Several scholars propose that social capital facilitates the development of a distinctive knowledge base, thereby providing a foundation for the creation of firm innovation and competitive advantages (e.g., Adler & Kwon, Reference Adler and Kwon2002; Calantone, Cavusgil, & Zhao, Reference Calantone, Cavusgil and Zhao2002; Yli-Renko, Autio, & Tontti, Reference Yli-Renko, Autio and Tontti2002; Hult, Hurley, & Knight, Reference Hult, Hurley and Knight2004; Song & Thieme, Reference Song and Thieme2006). Additionally, social capital facilitates innovation by motivating cooperation and coordination among different members of the firm (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Adler & Kwon, Reference Adler and Kwon2002; Levin & Cross, Reference Levin and Cross2004; Leana & Pil, Reference Leana and Pil2006). According to Baregheh, Rowley, and Sambrook’s (Reference Baregheh, Rowley and Sambrook2009) and Craig and Moores’s (Reference Craig and Moores2006), innovation is a multi-stage process whereby organisations transform ideas into new/improved products, services, or processes in order to advance, compete, and differentiate themselves successfully in the marketplace. Hence, innovation is an essential process for the success, survival, and renewal of organisations. The exchange of ideas and knowledge and the existence of certain relationships among employees contribute to enhancing a firm’s ability to identify and develop new opportunities that could not be identified and developed otherwise (Subramaniam & Youndt, Reference Subramaniam and Youndt2005; Carrasco-Hernández & Jiménez-Jiménez, Reference Carrasco-Hernandez and Jimenez-Jimenez2013). Leana and Pil (Reference Leana and Pil2006) argue that social capital is not just the network itself or the links among the people that constitute it; rather, it is the resources created by the existence and characteristics of these links, such as information sharing and trust. Thus, intra-firm collaboration is considered important for innovation because network relationships provide channels through which knowledge can flow (e.g., Kostova & Roth, Reference Kostova and Roth2003; Subramaniam & Youndt, Reference Subramaniam and Youndt2005; Gupta, Tesluk, & Taylor, Reference Gupta, Tesluk and Taylor2007). Intra-organisational knowledge sharing also influences a firm’s capacity to innovate because it supports creativity and inspires new knowledge and ideas (Song & Thieme, Reference Song and Thieme2006; Aragon-Correa, García-Morales, & Cordon-Pozo, Reference Aragon-Correa, García-Morales and Cordon-Pozo2007).

Although social capital exists in all types of organisations, family firms – firms in which a family possesses a significant ownership stake and in whose operations multiple family members are involved (Sirmon, Arregle, Hitt, & Webb, Reference Sirmon, Arregle, Hitt and Webb2008; Chirico, Sirmon, Sciascia, & Mazzola, Reference Chirico, Sirmon, Sciascia and Mazzola2011) – share many similarities. Social structures and affective commitments are particularly salient in family firms because of the intersection of the family and business systems (e.g., Sirmon & Hitt, Reference Sirmon and Hitt2003). Family firms have their own idiosyncratic characteristics, such as family language, motivation, loyalty, and trust, which allow their members to communicate more efficiently and exchange more information with greater privacy (Tagiuri & Davis, Reference Tagiuri and Davis1996; Anderson & Reeb, Reference Anderson and Reeb2003; Botero et al., Reference Botero, Thomas, Graves and Fediuk2013; Vallejo-Martos & Puentes-Poyatos, Reference Vallejo-Martos and Puentes-Poyatos2014). Habbershon, Williams, and MacMillan (Reference Habbershon, Williams and MacMillan2003) refer to the idiosyncratic bundle of resources and capabilities possessed by family firms and resulting from familial interactions as the ‘familiness’ of the firm. Thus, family involvement is an important factor, which influences the interactions between the firm and family (Zahra, Reference Zahra2005). Family involvement may provide a firm with unique abilities to act idiosyncratically (Chrisman & Patel, Reference Chrisman and Patel2012) and, thereby, influence innovative decision making (Chrisman et al., Reference Chrisman, Chua, De Massis, Frattini and Wright2015). This idea agrees with existing studies on family firm innovation, which suggest that the development of new products, services, and processes results from creative cooperation (Nahapiet, Reference Nahapiet2009) and family involvement (e.g., Le Breton-Miller & Miller, Reference Le Breton-Miller and Miller2006; Zahra, Neubaum, & Larrañeta, Reference Zahra, Neubaum and Larrañeta2007).

Although the majority of family firms involve a family group as well as a non-family group (Mitchell, Morse, & Sharma, Reference Mitchell, Morse and Sharma2003; Miller, Le Breton-Miller, Minichilli, Corbetta, & Pittino, Reference Miller, Le Breton-Miller, Minichilli, Corbetta and Pittino2014), which form two distinct but complementary groups that coexist in family businesses (Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2013, Reference Sanchez-Famoso, Maseda and Iturralde2014), few analytical studies in the extant family firm literature consider these two social groups separately (e.g., McCollom, Reference McCollom1992; Ram, Reference Ram2001; Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007; Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2014). With respect to the relationship between family and non-family social capital and innovation, Sanchez-Famoso, Maseda, & Iturralde (Reference Sanchez-Famoso, Maseda and Iturralde2014) show that family social capital encourages a culture of long-term goal orientation, trust, and mutual understanding, while non-family social capital also has a positive effect on family firm innovation because of the diversity and professionalism of the non-family group members. Further, Sanchez-Famoso, Maseda, & Iturralde (Reference Sanchez-Famoso, Maseda and Iturralde2014) research suggests that non-family social capital could have a greater influence on family firm innovation.

Moderating effects of family involvement in management

Recent research has focussed on family firms as heterogeneous organisations since the relationships within them are not expected to be the same (e.g., Astrachan, Klein, & Smyrnios, Reference Astrachan, Klein and Smyrnios2002; Sharma, Reference Sharma2004; Miller & Le Breton-Miller, Reference Miller and Le Breton-Miller2006; Melin & Nordqvist, Reference Melin and Nordqvist2007; Howorth, Rose, Hamilton, & Westhead, Reference Howorth, Rose, Hamilton and Westhead2010; Chrisman et al., 2015; De Massis et al., Reference De Massis, Kotlar, Chua and Chrisman2014; Nordqvist, Sharma, & Chirico, Reference Nordqvist, Sharma and Chirico2014). In other words, while sharing several characteristics, family firms are not homogeneous in all aspects. They vary significantly regarding their goals, motivations, and uniformity of relationships (Miller & Le Breton-Miller, Reference Miller and Le Breton-Miller2006; Chrisman et al., Reference Chrisman, Chua, De Massis, Frattini and Wright2015). Melin and Nordqvist (Reference Melin and Nordqvist2007) identify different types of family firms based on family involvement, business, and family differences. Similarly, De Massis et al. (Reference De Massis, Kotlar, Chua and Chrisman2014) discuss why family involvement may be used to explain family firms’ heterogeneity. Moreover, family SMEs are governed and managed through key personal relationships among family and non-family members that could affect intra-organisational and inter-organisational relationships (Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007).

The TMT – defined as the chief executive officer (CEO) and the senior managers who directly report to the CEO (Boeker, Reference Boeker1997) – is widely recognised as one of the most important decision-making units in organisations (Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015; Vandekerkhof et al., Reference Vandekerkhof, Steijvers, Hendriks and Voordeckers2015), which is responsible for innovation-related decisions in firms (Talke, Salomo, & Rost, Reference Talke, Salomo and Rost2010). Hence, the involvement of family members in the TMT may have distinct consequences for the innovation of family firms (e.g., Miller, Le Breton-Miller, Lester, & Cannella, Reference Miller, Le Breton-Miller, Lester and Cannella2007; Westhead & Howorth, Reference Westhead and Howorth2007; Howorth et al., Reference Howorth, Rose, Hamilton and Westhead2010). In Hambrick and Mason’s (Reference Hambrick and Mason1984) work, in which they analysed ‘upper echelons perspective’, they pointed out that organisational outcomes could be predicted from managerial backgrounds, which are reflected in strategic outcomes. Therefore, TMT composition could influence innovation processes and outcomes (Hambrick & Mason, Reference Hambrick and Mason1984; Hambrick, Reference Hambrick2007; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015), especially in family SMEs, where senior managers direct the firm’s strategy and participate directly in the implementation of that strategy (Lubatkin et al., Reference Lubatkin, Simsek, Ling and Veiga2006). However, TMT research in the context of family firms remains scarce, despite the fact that these managers are closer to the firm’s existing competencies and, therefore, are knowledgeable about when and how to exploit them (Lubatkin et al., Reference Lubatkin, Simsek, Ling and Veiga2006; Basco & Voordeckers, Reference Basco and Voordeckers2015).

Family firms that pursue an innovative strategy need to be receptive to environmental change, and the inclusion of non-family managers could widen the available pool of expertise in the TMT (Chirico & Salvato, Reference Chirico and Salvato2008; Block, Reference Block2010; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015; Vandekerkhof et al., Reference Vandekerkhof, Steijvers, Hendriks and Voordeckers2015). Non-family involvement in management signals an inclusive working environment where multiple perspectives are appreciated and considered (Kellermanns & Eddleston, Reference Kellermanns and Eddleston2004). Moreover, family managers and non-family managers are socialised in different ways, and this different socialisation experience is likely to have an influence on a firm’s strategy (Block, Reference Block2011). The dispersion of power across family and non-family managers could lead to the modernisation of the firm’s objectives and strategies.

The authors are aware that there are contrary arguments. For example, family involvement could orient the firm management to a long-term future, and innovation use could be related to long-term decisions. However, the extant research reveals the negative consequences arising from family involvement in management, which could be especially relevant when such involvement is very high (De Massis, Kotlar, Campopiano, & Cassia, Reference De Massis, Kotlar, Campopiano and Cassia2015), suggesting that the higher level of non-family members in TMT means that internal social capital positively influences family firm innovation (Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015). In the context of social capital, family involvement in management could reduce the benefits of family social capital and non-family social capital for innovation in several ways. First, family members who are involved in day-to-day management tend to acquire and develop specific, in-depth knowledge (e.g., Carney, Reference Carney2005) within a narrow market niche (Cabrera-Suarez, De Saa-Perez, & Garcia-Almeida, Reference Cabrera-Suarez, De Saa-Perez and Garcia-Almeida2001; Westhead & Howorth, Reference Westhead and Howorth2006). This could lead to a desire to accommodate other team members for the ‘good’ of the team (Amason & Sapienza, Reference Amason and Sapienza1997) and ‘groupthinking’ (Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007), thereby compromising the people’s ability to generate alternative ideas (Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007). Consequently, excessive levels of family involvement in the TMT could result in the limited availability of diverse knowledge and multiple perspectives, which would limit innovation (Ruekert & Walker, Reference Ruekert and Walker1987; Handler, Reference Handler1992; Howorth et al., Reference Howorth, Rose, Hamilton and Westhead2010).

Second, high family involvement in management could lead to a more collectivistic orientation of senior managers, which would encourage them to consider the effect of their actions on other family members and would reduce the firm’s risk exposure in order to preserve family wealth (Cabrera-Suarez & Martin-Santana, Reference Cabrera-Suarez and Martin-Santana2013) and to maintain a familial atmosphere (Berrone, Cruz, Gomez-Mejia, & Larraza-Kintana, Reference Berrone, Cruz, Gomez-Mejia and Larraza-Kintana2010), thereby leading to resistance towards nonfamily managers. However, the generational perspective maintains that the degree of collectivistic orientation and that of risk exposure change as the firm moves through generations (Gersick, Davis, Hampton, & Lansberg, Reference Gersick, Davis, Hampton and Lansberg1997). In their analysis of Polish family firms, Kowalewski, Talavera, and Stetsyuk (Reference Kowalewski, Talavera and Stetsyuk2010) show that the social capital provided by first-generation managers is likely to benefit firms, resulting in better performance, because of the managers’ expertise with respect to the firm. It has been shown that first-generation family founders and managers have the necessary background to create a business (Aldrich & Cliff, Reference Aldrich and Cliff2003) because, in the first generation, family managers usually perceive a high level of commitment and trust (Vallejo-Martos & Puentes-Poyatos, Reference Vallejo-Martos and Puentes-Poyatos2014), which pushes them towards similar perspectives and common shares, that is, for new ways of doing thing (Kepner, Reference Kepner1991). These first-generation family founders and managers are often the driving force behind innovation. However, as the number of family members involved in management increases, different perspectives arise, and these differences can engender conflict (Gersick et al., Reference Gersick, Davis, Hampton and Lansberg1997). As Kellermanns, Eddleston, Barnett, and Pearson’s (Reference Kellermanns, Eddleston, Barnett and Pearson2008) work pointed out, such conflict persists and surfaces in most aspects of their relationship, including those of both family and non-family members. They can generate tension, irritation, suspicion, and resentment among organisational members, undermining the potential advantages of group interaction and reducing the family firm’s effectiveness by preventing cross-understanding of different individual team members (Chirico & Salvato, Reference Chirico and Salvato2016).

Third, innovation entails a greater involvement of specialised human capital, managerial talent, and expertise, which are normally not available within the family group, especially in family SMEs (Chrisman & Patel, Reference Chrisman and Patel2012). Therefore, a high degree of family management can deliver weaker collective cognition and disband family managers in the discussions, developments, and decisions affecting both the family and business (Kellermanns & Eddleston, Reference Kellermanns and Eddleston2004; Miller & Le Breton-Miller, Reference Miller and Le Breton-Miller2005; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015). Therefore, problems that are frequently present in family firms, such as centrality of control, conflicts of opinions, and resistance to ideas about new products, services, and processes, are likely to be mitigated when both family and non-family members are involved in management. In addition, non-family managers may contribute significantly by advising on family topics that affect the enterprise over time (Basco & Voordeckers, Reference Basco and Voordeckers2015).

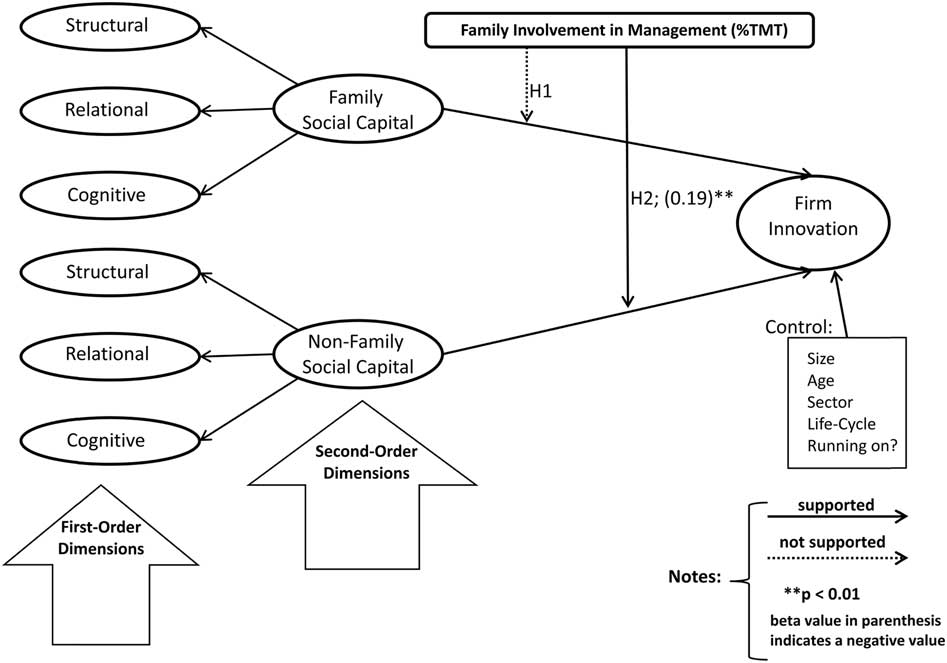

We agree with Vandekerkhof et al. (Reference Vandekerkhof, Steijvers, Hendriks and Voordeckers2015) that non-family managers are important stakeholders who could add knowledge, solve family succession problems, or even mediate family conflict (Dyer, Reference Dyer1989; Klein & Kozlowski, Reference Klein and Kozlowski2000; Sonfield & Lussier, Reference Sonfield and Lussier2009; Block, Reference Block2011; Basco & Voordeckers, Reference Basco and Voordeckers2015). The inclusion of non-family members in the management team increases the social capital of firms (Portes, Reference Portes1998), and it facilitates the acquisition and promotion of information from diverse sources (Blyler & Coff, Reference Blyler and Coff2003), with a positive effect on innovation. The information base of non-family managers is expected to be different and higher than that of family managers, thereby affecting new products, services, and/or processes (Shane, Reference Shane2003). Considering these arguments, we propose the following hypotheses (see Figure 1).

Hypothesis 1 : Family management has a negative effect in the positive relationships between family social capital and family firm innovation. Specifically, the greater the family members’ control of business operations, the weaker the positive effect of family social capital would be on family firm innovation.

Hypothesis 2 : Family management has a negative effect in the positive relationship between non-family social capital and family firm innovation. Specifically, the greater the family members’ control of business operations, the weaker the positive effect of non-family social capital would be on family firm innovation.

Figure 1 Standardised path loading for hypothesised model

Methodology

Sample and data collection

We chose Spanish firms for this study because according to the estimates provided by the Spanish Family Enterprise Institute (2009), there are around 2.9 million family enterprises (out of a total of 3.4 million enterprises) in Spain, which generate 70% of the total Spanish gross domestic product (GDP) and employ nearly 13.9 million people (representing around 75% of total private employment in Spain). The final report of the European expert group in the field of family enterprises (GEEF, 2009) reports that in most nations for which the data were compiled (the United States, Europe, Asia, and Australia), more than 60% of all firms were classified as family firms. These data show that Spain has more family enterprises than the average share.

Given the lack of a reliable business census that clearly distinguishes between family and non-family firms in Spain, we used the Iberian Balance Sheet Analysis System (SABI)Footnote 1 database to establish the population of family businesses in this study. We used demographic parameters (Shanker & Astrachan, Reference Shanker and Astrachan1996) to identify the sample used in this study. To obtain a sample, we selected the following types of firms from the SABI database: (1) non-listed Spanish companies with more than 10 employees – because the presence of at least 10 employees could reinforce communication at work (Sorenson, Reference Sorenson2012); (2) companies that provided financial information for (at least) the last 5 years; (3) companies not affected by special situations such as insolvency, wind-up, liquidation, or zero activity (in order to obtain a sample that was representative of the population); and (4) companies in which at least 51% of the firm is owned by members of the same family (Westhead & Howorth, Reference Westhead and Howorth2006). These criteria were applied to the SABI database, along with an exhaustive review of shareholder structures (percentage of common stock) and composition (names and surnames of shareholders)Footnote 2 . From the original dataset of 26,064 Spanish enterprises that fell within the set parameters, 1,122 enterprises met the specified family criteria.

It was necessary to survey firms because secondary data for Spanish non-listed family firms were not readily available, especially in relation to the factors of theoretical interest in this study (relationships within the family group, relationships within the non-family group, and innovation perceptions). The CEOs of the selected firms were sent letters in December 2012, requesting the participation of one family member as well as one non-family member (both with managerial functions) in the study. In the letter, we explained that a professional survey research firm would get in touch with them in the following 30–60 days to conduct telephonic interviews in order to complete the questionnaires. To ensure a high response rate and reliable and accurate responses, the CEOs were promised that the information about the respondents and the company would remain strictly confidential. Additionally, they were promised a summary of the study’s results. Two weeks after the first letters were sent, another set of letters was sent to remind them about the study. Finally, in January 2013, 1 week after the reminders were sent, a professional survey research firm was commissioned to conduct telephonic interviews. In each surveyed family firm, the professional survey research firm encouraged participation provided a reminder about the importance and purpose of the study, and guaranteed confidentiality. Information was collected from a family member (to collect information about the relationships among family members and innovation) and from a non-family member (to collect information about relationships among non-family members), both with managerial functions. Since people with managerial functions are directly involved in day-to day operations and have first-hand information about what is going on, they are the appropriate respondents for studies of firm-level processes such as social capital and innovation. We also looked for family firms in which more than one family member and more than one non-family member worked in order to understand the relationships among family members and among non-family members (Sorenson, Reference Sorenson2012). The professional research company assisted us in meeting this requirement by asking the family member and/or the non-family member (with managerial functions) whether there were at least two family members and/or two non-family members working in the family firm. As Brass, Galaskiewicz, Greve, and Tsai (Reference Brass, Galaskiewicz, Greve and Tsai2004: 801) point out, ‘when two individuals interact, they not only represent an interpersonal tie, but they also represent the groups of which they are members’.

After reviewing the most relevant literature on the topics relevant to this study, the questionnaire was designed in three parts. The first part requested general information about the family firm. The second part contained questions addressed to family members, and the final part included questions addressed to the non-family members of the family firm. The questionnaire consisted of closed questions, using Likert-type scales (ranging from ‘strongly disagree’ to ‘strongly agree’), and dichotomous questions. We tested the questionnaire in seven family firms from different industrial sectors, conducting face-to-face interviews, first with a family member and subsequently with a non-family member in each firm (both with managerial functions). Their comments on the survey content, item wording, terminology, and clarity were incorporated into a revised instrument. The refined instrument was piloted on eight family firms, with one family member and one non-family member with managerial functions in each firm, and final revisions were made. These revision efforts created a highly reliable instrument (Cronbach’s α ranging from 0.71 to 0.85) (see Appendix I).

Measurement of model variables

For this study, the majority of the items were measured using 5-point Likert scales ranging from one (strongly disagree) to five (strongly agree). Consistent with our research focus and similar prior approaches assessing firm-level phenomena based on individual-level responses (e.g., De Clerq, Dimov, & Thongpapanl, 2010), the survey questions were worded in order to capture the attitudes and behaviours occurring at the firm level rather than at the managerial level (Brass et al., Reference Brass, Galaskiewicz, Greve and Tsai2004; Whetten, Felin, & King, Reference Whetten, Felin and King2009). Thus, in relation to the questions on social capital and firm innovation, the respondents offered opinions about the interactions and relationships within their firm in general, instead of focussing on their own individual situations.

Firm innovation (dependent variable)

There are several important limitations associated with using objective measures of innovation in non-listed firms. The first is the use of the number of patents as an indicator of innovation, because of the difference between innovation and invention (Edwards & Gordon, Reference Edwards and Gordon1984), the inability to capture all the innovations that are actually made (Acs & Audretsch, Reference Acs and Audretsch2005), and the uncertainty about the propensity to register patents (Scherer, Reference Scherer1983; Edwards & Gordon, Reference Edwards and Gordon1984). Second, some objective measures of innovation in private firms were not available or were difficult to obtain (Acquaah, Reference Acquaah2011). Third, prior empirical studies have shown that innovation is a multidimensional concept, and that it is difficult to reduce this concept to a simple measure (e.g., Subramaniam & Youndt, 2005). With these factors in mind, and given that perceptual measures are generally recommended for studies of human behaviour (Howard, Reference Howard1994; Spector, Reference Spector1994; Basco & Voordeckers, Reference Basco and Voordeckers2015) and are widely used in studies on innovation, we decided to use subjective (self-reported) measures of innovation, taking into account prior research (Miller & Friesen, Reference Miller and Friesen1983; Uzzi & Lancaster, Reference Uzzi and Lancaster2003; Jansen, Van Den Bosch, & Volverda, Reference Jansen, Van Den Bosch and Volverda2006; García-Morales, Lloréns-Montes, & Verdú-Jover, Reference García-Morales, Lloréns-Montes and Verdú-Jover2008; Basco & Voordeckers, Reference Basco and Voordeckers2015).

Social capital

Prior studies of social capital failed to consider the three dimensions of social capital identified by Nahapiet and Ghoshal (Reference Nahapiet and Ghoshal1998). In order to understand social capital fully, it is important to produce internal social capital indicators that cover all three dimensions of social capital. The family social capital and non-family social capital constructs are second-order reflective factors (Casanueva-Rocha, Castro-Abancens, & Galan-Gonzalez, Reference Casanueva-Rocha, Castro-Abancéns and Galan-González2010; Carr et al., Reference Carr, Cole, Kirk-Ring and Blettner2011; Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2013) that include the structural, relational, and cognitive dimensions commonly used in the literature (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Tsai & Ghoshal, Reference Tsai and Ghoshal1998; Bolino, Turnley, & Bloodgood, Reference Bolino, Turnley and Bloodgood2002; Inkpen & Tsang, Reference Inkpen and Tsang2005). Both family and non-family social capital are independent variables. The structural dimension is the extent to which group members are connected (Inkpen & Tsang, Reference Inkpen and Tsang2005). Following Pearson, Carr, and Shaw, (Reference Pearson, Carr and Shaw2008), we looked for information about social interactions among the members of the family group and non-family group. We asked the respondents questions that referenced the focus reported in Tsai and Ghoshal (Reference Tsai and Ghoshal1998). The relational dimension focusses on the quality of the group members’ connections. This dimension includes trust and trustworthiness (Nahapiet & Ghoshal, Reference Nahapiet and Ghoshal1998; Tsai & Ghoshal, Reference Tsai and Ghoshal1998). When individuals trust one another, they are more likely to cooperate with the collective actions of the firm (Fukuyama, Reference Fukuyama1995), as trust is an essential component of effective collaboration (Leana & Van Buren, Reference Leana and Van Buren1999). Coleman (Reference Coleman1988) acknowledges the central role of trust in social capital. The respondents were asked questions based on the research of Cuevas-Rodriguez, Cabello-Medina, and Carmona-Lavado (Reference Cuevas-Rodriguez, Cabello-Medina and Carmona-Lavado2014) and Tsai and Ghoshal (Reference Tsai and Ghoshal1998). The cognitive dimension focusses on the extent to which a group’s members share a common perspective or understanding (Inkpen & Tsang, Reference Inkpen and Tsang2005). Following Pearson, Carr, and Shaw, (Reference Pearson, Carr and Shaw2008), we evaluated the groups’ shared vision and purpose, as well as their unique language and culture. We asked the family members and non-family members questions based on the research of Nahapiet and Ghoshal (Reference Nahapiet and Ghoshal1998) and Tsai and Ghoshal (Reference Tsai and Ghoshal1998).

Family involvement in management

This moderator variable was measured as the percentage of family members constituting the TMT (e.g., Miller et al., Reference Miller, Le Breton-Miller, Lester and Cannella2007; Zahra, Neubaum, & Larrañeta, Reference Zahra, Neubaum and Larrañeta2007; Mazzola, Sciascia, & Kellermanns, Reference Mazzola, Sciascia and Kellermanns2013). It was calculated as the number of family top managers divided by the total size of the firm’s TMT. This fraction was then multiplied by 100 (Zahra, Neubaum, & Larrañeta, Reference Zahra, Neubaum and Larrañeta2007).

Control variables

We acknowledge the importance of factors that could affect a family firm’s innovation by including several specific control variables (business size, business age, business sector, life stage, and long-term orientation)Footnote 3 in our model. Although there are undoubtedly many other factors, these specific variables were chosen because of their importance. First, business size is included because prior research has demonstrated that a family firm’s size could be linked to its greater or lesser tendency for innovation (e.g., Bantel & Jackson, Reference Bantel and Jackson1989). Business size was measured using the natural log of total assets. Second, business age was measured using the natural log of a firm’s age, calculated as the difference between the year in which the survey was conducted (2013) and the year in which the firm was founded. Third, the influence of the business sector on innovation was captured using the operationalisation of the business sector as a dummy variable, which was coded 1 for manufacturing firms and 0 for service firms following the Spanish industrial classification method (National Classification of Economic Activities: CNAE)Footnote 4 . Fourth, the respondents provided the life stage using Adizes’s (Reference Adizes1979) framework. According to Dyer (Reference Dyer1986), it is common to find family firms with more innovative perspectives during the first and second stages of their lifecycle. Finally, because our firms are all family owned (i.e., most of the equity is owned by a family), we controlled for long-term orientation. When a family focusses on the long term, the business is more secure, and the firm is often less willing to undergo innovation. In this context, we asked the family members whether they would like the next generations to continue running the firm (yes/no) (Vallejo-Martos, Reference Vallejo-Martos2009).

Of the 769 firms that were contacted, 232 completed the survey. However, given the multiple-informant design of the survey, family firms with only one respondent were removed from the sample. Consequently, 60 family firms were eliminated from further consideration (28 family firms in which only a family member responded, and 32 family firms in which only a non-family member responded). A total of 172 questionnaires were found to be complete. The response rate was 22.37%, which is similar to that of other studies in the Spanish context (e.g., Cruz & Nordqvist, Reference Cruz and Nordqvist2012; Vallejo-Martos & Puentes-Poyatos, Reference Vallejo-Martos and Puentes-Poyatos2014). The overall sampling error was 6.53%, with a confidence level of 95%, and p=q=0.50. With regard to the respondents, in the family group, 50.50% were CEOs, and 49.50% were managers from different areas. In the non-family group, 49.50% of the respondents were financial managers, 41.70% were managers from other areas, and 8.80% were CEOs. A brief analysis of our sample shows that only 6% of the family firms have been in existence for less than 10 years (these are mainly the family firms in the sample of consolidated companies). In other words, most of the firms in our sample have passed through their early years and have had the opportunity to establish relationships among their employees.

With regard to firm size, 23% of the firms have between 10 and 50 employees, 72% have between 50 and 250 employees, and only 5% have over 250 employees. Thus, most of the sample firms are SMEsFootnote 5 . In terms of firm size, the sample has an average size of 93 employees and a median of 67. When we consider the generations involved in joint management, the firms are managed by only one generation in 56% of the cases, by two generations in 40% of the cases, and by three or more generations in 4% of the cases. With regard to the generation of the firms, 37% are in their first generation, 41% are in their second generation, 12% are in their third generation, 8% are in their fourth generation, and 2% are in their fifth or older generation. Finally, 48% of the firms in the sample belong to the manufacturing sector and 52% to the service sector (see Table 1). Therefore, the descriptive statistics for our sample are in line with those of prior studies on Spanish non-listed family firms (e.g., Cabrera-Suarez, Deniz-Deniz, & Martin-Santana, Reference Cabrera-Suarez, Deniz-Deniz and Martin-Santana2015; Deniz-Deniz & Cabrera-Suarez, Reference Deniz-Deniz and Cabrera-Suarez2005). Table 2 presents the descriptive statistics and correlations for all the variables analysed in this studyFootnote 6 .

Table 1 Sample characteristics

Table 2 Descriptive statistics and correlations

Notes. n=172. Correlations greater than І0.19І are significant at p<.01. Correlations greater than І0.14І are significant at p<.05

To assess non-response bias, we randomly selected 50 non-responding firms. Using the Kolmogorov–Smirnov two-sample test (Siegel & Castellan, Reference Siegel and Castellan1988) between responding and non-responding firms (whose data was taken from the SABI database), the non-response analysis found no statistically significant differences with respect to firm size, age, performance, annual sales volume, number of employees, or sector.

Data analysis

The proposed models were tested using structural equation modelling (SEM). Although SEM is an increasingly popular approach in business research and the related social sciences, family firm researchers have used this method sparingly (Wilson, Whitmoyer, Pieper, Astrachan, Hair, & Sarstedt, Reference Wilson, Whitmoyer, Pieper, Astrachan, Hair and Sarstedt2014). Several family firm researchers have called for the use of more sophisticated and rigorous statistical analysis techniques, including SEM (e.g., Westhead & Howorth, Reference Westhead and Howorth2006; Debicki, Matherne, Kellermanns, & Chrisman, Reference Debicki, Matherne, Kellermanns and Chrisman2009; Dyer & Dyer, Reference Dyer and Dyer2009). In fact, with regard to statistics in family firm research, SEM represents an advanced version of the general linear modelling procedures (e.g., multiple regression analysis) (Astrachan, Patel, & Wanzenried, Reference Astrachan, Patel and Wanzenried2014). Lei and Wu (Reference Lei and Wu2007) claim that SEM can be used to assess ‘whether a hypothesised model is consistent with the data collected to reflect [the] theory’ (p. 34). In particular, partial least squares structural equation modelling (PLS-SEM), which is a variance-based technique, is preferred to covariance-based techniques (e.g., AMOS, EQS) and linear modelling (e.g., multiple regression analysis) in several contexts: first, when dealing with latent constructs that cannot be observed or measured directly (Astrachan, Patel, & Wanzenried, Reference Astrachan, Patel and Wanzenried2014); second, when the moderating effects are being analysed (Chin, Marcolin, & Newsted, Reference Chin, Marcolin and Newsted2003); third, when multiple items have been used to represent each construct (Baron & Kenny, Reference Baron and Kenny1986; McClelland & Judd, Reference McClelland and Judd1993; Iacobucci, Saldanha, & Deng, Reference Iacobucci, Saldanha and Deng2007); and finally, when the data are not normally distributed, and the sample size is small (Alavifar, Karimimalayer, & Anuar, Reference Alavifar, Karimimalayer and Anuar2012; Astrachan, Patel, & Wanzenried, Reference Astrachan, Patel and Wanzenried2014). PLS-SEM should be applied for samples with fewer than 250 observations.

We used two methods to analyse the data collected in this research. On the one hand, SPSS software was used to compute the descriptive statistics (means, standard deviations) and the correlation matrix. On the other hand, partial least squares (PLS) was used in addition to SPSS to calculate the reliability and validity indexes of the variables and to test the research hypotheses through SEM. Specifically, we used SmartPLS 2.0.M3 software (Ringle, Wende, & Will, Reference Ringle, Wende and Will2005) for Windows.

Overall, the hypotheses described in this study represent the moderating or interaction effects. To test these moderated relationships, a well-known technique was applied: the product-indicator approach (Henseler & Fassott, Reference Henseler and Fassott2010). This approach involves a straightforward modelling of the moderating effects when the moderator linearly influences the strength of the moderated direct relationship (Henseler & Fassott, Reference Henseler and Fassott2010).

Results

A PLS model is analysed and interpreted in two stages: (1) assessment of the reliability and validity of the measurement model; and (2) assessment of the structural model (Hair, Hult, Ringle, & Sarstedt, Reference Hair, Hult, Ringle and Sarstedt2014). This sequence ensures that the constructs’ measures are valid and reliable before attempting to draw conclusions regarding the relationships among the constructs (Barclay, Higgins, & Thompson, Reference Barclay, Higgins and Thompson1995).

Validity of measurement model

In order to evaluate the measurement model, we need to analyse the following aspects of all the first- and second-order reflective latent variables intervening in the proposed model: individual item reliability, construct reliability, convergent validity, and discriminant validity (Hair et al., Reference Hair, Hult, Ringle and Sarstedt2014).

Individual item reliability

Individual item reliability is considered to be adequate when an item has a factor loading greater than 0.60 (Bagozzi & Yi, Reference Bagozzi and Yi1988). Table 3 shows the results of the individual item reliability test. In this study, all the indicators and dimensions surpass the basic level of 0.60.

Table 3 Validation of the final model (reliability and convergent validity of first-and second-order reflective factors)

Notes. CA=Cronbach's α; CR=composite reliability; AVE=average variance extracted

***p<.001.

Construct reliability and convergent validity

We used two indicators of internal consistency to evaluate construct reliability: Cronbach’s α and Fornell and Larcker’s (Reference Fornell and Larcker1981) composite reliability indicator. We followed the criterion proposed by Nunnally (Reference Nunnally1987), who considers 0.70 to be the minimum acceptable reliability value. Since the values of all the constructs exceed 0.70, we can validate the reliability of our latent variables. Moreover, we checked the significance of the loadings with a bootstrap procedure (5,000 sub-samples) for obtaining t-statistic values. They are all found to be significant. With regard to convergent validity, we examined the average variance extracted (AVE) (Fornell & Larcker, Reference Fornell and Larcker1981). In order for convergent validity to exist, this indicator should take on values greater than 0.50, which means that 50% or more of the indicator variance should be accounted for. In Table 3, we report the Cronbach’s α, composite reliability, AVE, and R 2 values.

Discriminant validity

To assess discriminant validity, the AVE should be greater than the variance shared between a construct and the other constructs in the model (i.e., the squared correlation between two constructs). For adequate discriminant validity, the diagonal elements should be significantly greater than the off-diagonal elements in the corresponding rows and columns (Barclay, Higgins, & Thompson, Reference Barclay, Higgins and Thompson1995). This condition is satisfied for the reflective variables and second-order constructs in relation to the rest of the variables. In Table 4, we show the values resulting from these calculations.

Table 4 Average variance extracted and squared correlation – discriminant validity

Notes. Diagonal represents the square root of the average variance extracted, while above the diagonal, the shared variances (squared correlations) are represented

The results pertaining to individual item reliability, construct reliability, convergent validity, and discriminant validity reinforce the reflective nature of the family social capital and non-family social capital constructs (Coltman, Devinney, Midgley, & Venaik, Reference Coltman, Devinney, Midgley and Venaik2008).

Estimation of the structural model

Having established confidence in our measurement model, the bootstrap re-sampling procedure (5,000 subsamples) was used to generate the standard errors and the t-values, thereby allowing the β coefficients to be made statistically significant. In order to study the predictive relevance of our regression model, we used a Q 2 test (e.g., Fornell & Cha, Reference Fornell and Cha1994; Chin, Reference Chin1998). A Q 2 value is applicable only in dependent constructs, and when a value greater than 0 implies that the model offers predictive relevance. The results of our study confirm that our models offer satisfactory predictive relevanceFootnote 7 . Table 5 includes the hypothesised paths and five control variables (business size, business age, business sector, life stage, and long-term orientation). As shown in Table 5, in the first stage, we run the model to determine the influence of family social capital on family firm innovation. In the second stage, we run the model to determine the influence of non-family social capital on family firm innovation. In the third stage, we run the model with all the variables to determine the combined influence of family social capital and non-family social capital on innovation. The results confirm the influence of family social capital and non-family social capital on family firm innovation. Finally, in the fourth stage, we include the moderating variable (family involvement in management). As in the regression analysis, the predictor and moderator variables are multiplied to obtain the interaction terms. As suggested by Chin et al. (Reference Chin, Marcolin and Newsted2003), we mean-centred the indicators prior to multiplying them. The R 2 for this last stage is 0.34. The difference in R 2 provides the overall effect size (f 2 ) for the interaction effects. We find that the increase in R 2 attributable to the moderating effects is statistically significant (Tabachnick & Fidell, Reference Tabachnick and Fidell1996). Overall, based on Cohen (Reference Cohen1988), the interaction effects model – in which family involvement in the TMT moderates the relationships between internal social capital (both family social capital and non-family social capital) and family firm innovation – possesses a more significant, moderate explanatory power compared to the direct effects models (f 2 =0.08). The results related to the interaction effects are presented in the fourth column of Table 5. Thus, Hypothesis 1 is not supported by the results. Hypothesis 2 is supported, proving that family involvement in management moderates the relationship between non-family social capital and innovation.

Table 5 PLS path analysis results (standardised β coefficients)

Notes. β values in parentheses indicate a negative relationships

***p<.001; **p<.01; *p<.05; ^p<.10

Discussion

The primary objective of this study was to associate the social capital perspective with research on the potential implications that family involvement in management (specifically, the TMT) would have on the relationships between family and non-family social capital and firm innovation. We reviewed the extant literature on innovation to determine whether social capital could be considered an explanatory variable of innovation in family firms. Recent theoretical and empirical studies on family firms highlight the importance of internal social capital in providing a competitive advantage to family businesses (e.g., Hoffman, Hoelscher, & Sorenson, Reference Hoffman, Hoelscher and Sorenson2006; Sorenson, Goodpaster, Hedberg, & Yu, Reference Sorenson, Goodpaster, Hedberg and Yu2009; Carr et al., Reference Carr, Cole, Kirk-Ring and Blettner2011). To the best of our knowledge, very few studies have empirically focussed on the internal social capital generated in family firms while considering both family and non-family social capital (Sanchez-Famoso, Maseda, & Iturralde, Reference Sanchez-Famoso, Maseda and Iturralde2013, Reference Sanchez-Famoso, Maseda and Iturralde2014), and none have focussed on these relationships in family firms by taking into account the role of family involvement in management. Thus, this study is one of the first quantitative efforts to examine the relative contribution of family social capital and non-family social capital towards innovation in family firms, and the extent to which family involvement in management affects the relationships between both family and non-family social capital and family firm innovation (e.g.,Chrisman, Chua, & Litz, Reference Chrisman, Chua and Litz2003; Sharma, Reference Sharma2004; De Massis, Frattini, & Lichtenthaler, Reference De Massis, Frattini and Lichtenthaler2013a).

Specifically, we predicted that the more the number of family members in the TMT, the weaker would be the effect of both family and non-family social capital on innovation because of the general lack of professional competencies of family members in family SMEs, the barriers to increasing social capital, and the orientation towards non-economic goals. These disadvantages supersede the benefits of family involvement in management deriving from the relational, cognitive, and structural dimensions. These hypotheses were tested using survey data collected through telephonic interviews with the managers of 172 family SMEs, with responses from one family member and one non-family member per firm (344 respondents).

This study found one strongly significant relationship regarding the presence of family members in the TMT: family involvement in management weakens the effect of non-family social capital on innovation. This result is in line with the Vallejo-Martos and Puentes-Poyatos’s (Reference Vallejo-Martos and Puentes-Poyatos2014) results, in which they show that family firm owners who wish to achieve innovation need to ensure the involvement of different organisational members such as non-family managers. With regard to the influence that family involvement in management has on the relationship between family social capital and innovation, no strongly significant relationship was found (see Figure 1).

This study makes several contributions to the literature. First, innovation in family firms cannot be fully understood without accounting for the moderating effect of family involvement in management. In this sense, the results have demonstrated the importance of non-family managers in the firm: the greater the family involvement in management, the weaker the effect of non-family social capital is on innovation. This result confirms and adds more details to the findings of Westhead and Howorth (Reference Westhead and Howorth2006) regarding the negative relationship between family involvement in management and performance. An explanation for this could be that family members who are involved in management tend to acquire and develop specific, in-depth knowledge (Carney, Reference Carney2005), which is likely to make non-family managers feel less motivated, because the kinship group could limit the pool of experience and inclusion of multiple perspectives, in turn limiting innovation (Ruekert & Walker, Reference Ruekert and Walker1987; Handler, Reference Handler1992; Howorth et al., Reference Howorth, Rose, Hamilton and Westhead2010). This finding is in line with studies that test whether the presence of non-family members in the TMT has an important impact on the success and growth of the family business (e.g., Sharma, Reference Sharma2004; Sundaramurthy, Reference Sundaramurthy2008; Cabrera-Suarez & Martin-Santana, Reference Cabrera-Suarez and Martin-Santana2013; Sanchez-Marin & Baixauli-Soler, Reference Sanchez-Marin and Baixauli-Soler2015). Through their diverse experience, professionalism, and relationships, non-family managers provide a family firm with resources that strengthen the firm’s capabilities (e.g., Dyer, Reference Dyer1989; Davidsson & Honig, Reference Davidsson and Honig2003; Vallejo-Martos & Puentes-Poyatos, Reference Vallejo-Martos and Puentes-Poyatos2014), which confirms that non-family managers are also important contributors to the success of family firms (Klein & Bell, Reference Klein and Bell2007; Vallejo-Martos & Puentes-Poyatos, Reference Vallejo-Martos and Puentes-Poyatos2014). Further, as Ng and Roberts (Reference Ng and Roberts2007) reported, non-family managers implement corrective actions to mitigate tensions among family members. We expected family involvement in management to negatively moderate the relationship between family social capital and innovation; however, our results do not confirm this relationship. It is possible that a greater representation of family members in the TMT enhances formal knowledge sharing and the cultivation of this knowledge in building and sustaining innovation. Family managers could also orient the firm management to a long-term future, and innovation use could be related to long-term decisions. As Dyer (Reference Dyer2006) reported, family managers could bring common goals, high trust, and shared values, in addition to unified governance, to the firm.

The second contribution of this study is in line with other studies that represent family firms as a heterogeneous group (not all family firms have the same behaviours and achieve the same results), not only because of the important role played by non-family managers, as suggested by Cruz and Nordqvist (Reference Cruz and Nordqvist2012), De Massis et al. (Reference De Massis, Kotlar, Campopiano and Cassia2015), Dyer (Reference Dyer2006), and Zahra, Neubaum, and Larrañeta (Reference Zahra, Neubaum and Larrañeta2007), but also because the results demonstrate the coexistence of family social capital and non-family social capital in family firms, both of which influence family firm innovation. With regard to the latter point, prior studies analysed the social capital construct at different levels (e.g., Leana & Van Buren, Reference Leana and Van Buren1999), while suggesting that social capital is homogeneous and independent of other social groups within an organisation. Therefore, family groups have received extensive attention in the strategy, entrepreneurship, and family business research (Melin & Nordqvist, Reference Melin and Nordqvist2007; Nordqvist et al., Reference Nordqvist, Sharma and Chirico2014). In this study, we follow the calls made by some prior researchers (e.g., McCollom, Reference McCollom1992; Ram, Reference Ram2001; Sharma, Reference Sharma2008; Stewart & Hitt, Reference Stewart and Hitt2012) to consider the non-family group as an additional level of analysis when investigating the social capital of family firms. Moreover, in line with other researchers (Habbershon, Williams, & McMillan, Reference Habbershon, Williams and MacMillan2003; Hoffman, Hoelscher, & Sorenson, Reference Hoffman, Hoelscher and Sorenson2006; Arregle et al., Reference Arregle, Hitt, Sirmon and Very2007; Pearson, Carr, & Shaw, Reference Pearson, Carr and Shaw2008), we identified social capital theory to be particularly relevant to the study of family firms.

The third contribution is that our theory and findings complement recent studies emphasising that family firms surpass non-family firms when non-family managers are present (e.g., Savolainen & Kansikas, Reference Savolainen and Kansikas2013). Our study suggests that it is important to examine the different types of relationships (structural dimension) and potential family ties among the actors (relational dimension), rather than simply examining the strength of the relationships (cognitive dimension). Structural and relational dimensions are complementary; the structural dimension refers to the structure of networks (determining with whom each individual maintains contacts), while the relational dimension focusses on the quality (closeness) of these networks (Moran, Reference Moran2005). Finally, given that the family firm is an organisational archetype characterised by a dominant social group (similar to many other organisations) (Foreman & Whetten, Reference Foreman and Whetten2002), many of the relationship characteristics that occur in a family firm context could be generalised to other organisations. Thus, our study has the potential to help scholars and practitioners to understand social capital and innovation more clearly in the context of other organisational forms that are characterised by strong social structures.

Implications for management practice

Our model has important implications for family firm managers because it can help them to understand the antecedents of firm innovation. For example, trust among all family firm members is crucial for innovation. In addition, the adoption of a set of best practices for managing employees is believed to have a positive effect on innovation (e.g., Wright & Snell, Reference Wright and Snell1998). First, our research represents an unconventional approach to the importance of family and non-family social capital as potential sources of competitive advantage for family firms. This is especially relevant to most family firms that lack a successor and are embarking on the process of hiring non-family executives (e.g., non-family CEOs), who will strive to achieve innovation through their knowledge and social networks beyond the family. Thus, more effective integration of non-family members into the business is important in order to encourage innovation. Therefore, the drivers and elements of non-family social capital must be well managed and understood. Second, managers should encourage knowledge acquisition and collaboration by carefully managing internal relationships (Wright & Snell, Reference Wright and Snell1998; Craig & Moores, Reference Craig and Moores2010). Sundaramurthy (Reference Sundaramurthy2008: 89) asserts that non-family members serve as a critical ‘trust catalyst’, building bridges between family members. For example, in line with Nonino (Reference Nonino2013), informal meetings and discussions in which family and non-family members have the opportunity to participate could act as valuable sources of innovation and could help in creating consensus about the goals of the firm. Finally, family firms should consider hiring non-family managers, at least for positions that are critical to the innovation process. Adding non-family managers to the management team seems to widen the set of alternative assumptions or opinions that are considered. Non-family members could make vital contributions because they could expand the knowledge base of the family business by introducing additional skills, assisting with conflict resolution, and promoting professionalism.

Limitations and directions for future research

In all empirical studies, the limitations must be identified and considered when interpreting the results and drawing conclusions. Because of the cross-sectional nature of this study, the findings cannot be generalised across the family business population. Further, it would be beneficial to test and examine the reported effects over time. Thus, future research should adopt a longitudinal design to allow for stronger causal interpretations. Another limitation of this study is that our measures constrain our results. There are many potential ways to measure family involvement in management. The measures selected in this study are consistent with, but not necessarily identical to, those used in prior studies (e.g., Chrisman, Chua, & Litz, Reference Chrisman, Chua and Litz2004; Klein, Astrachan, & Smyrnios, Reference Klein, Astrachan and Smyrnios2005). Additional items could be added and tested to improve these measures in future research. Finally, the research sample consists of Spanish non-listed family firms, which could limit the generalisation of the results. For example, in Spain, great importance is placed on family relationships, and family unity and harmony are more highly valued than they are in other countries such as the United States (Poza, Reference Poza1995). Thus, it would be interesting for future research to compare the findings of this study with the findings obtained in other more individualistic settings in which the individual’s importance and personal achievements are placed above the group’s interests.

Despite these limitations, this study has added to the empirical body of research on family business, social capital, and innovation, and marks an important step towards gaining insights into the ways in which family involvement in management influences the relationship between internal social capital and innovation in family firms.

Acknowledgements

We are indebted to the associate editor – Peter Galvin- and the two anonymous reviewers for their insightful and developmental feedback. We highly appreciate the financial support received from the Family Business Centre of the University of the Basque Country UPV/EHU for financial support (DFB/BFA and European Social fund). This research has received financial support from the UPV/EHU (Project UPV/EHU 14/52).

APPENDIX I: Variables and Items

ORIGINAL IN SPANISH

Measures: Family social capital – Likert (1-5) (α=0.78)

Please indicate your agreement with the following statements concerning the relationships between family members working in the family firm. For your rating, take into account that ‘1’ is to express that you completely disagree and ‘5’ that you completely agree.

STRUCTURAL DIMENSION (α=0.80)

-

– Item 1: In general, family members who work in the company and /or are members of the board of directors also maintain relationships outside the company (dinners, clubs, …)

-

– Item 2: In general, family members who work in the company and/or are members of the board of directors maintain close social relationships outside the company; that is, they collaborate with one another to solve company problems together.

RELATIONAL DIMENSION (α=0.84)

-

– Item 3: In general, family members who work in the company and/or are members of the board of directors maintain close social relationships because they share information and rely on each other to conduct business.

-

– Item 4: In general, family members who work in the company and/or are members of the board of directors keep their promises and are loyal to the company.

COGNITIVE DIMENSION (α=0.74)

-

– Item 5: In general, family members who work in the company and/or are members of the board of directors share the same ambitions, vision, and values.

-

– Item 6: In general, family members who work in the company and/or are members of the board of directors pursue the same objectives and mission.

Measures: Non-Family social capital – Likert (1-5) (α=0.80)

Please indicate your agreement with the following statements concerning the relationships between non-family members working in the family firm. For your rating, take into account that ‘1’ is to express that you completely disagree and ‘5’ that you completely agree.

STRUCTURAL DIMENSION (α=0.71)

-

– Item 7: In general, non-family members who work in the company maintain relationships outside company (dinners, clubs, …)

-

– Item 8: In general, non-family members who work in the company maintain close social relationships outside the company; that is, they collaborate with one another to solve company problems together.

RELATIONAL DIMENSION (α=0.80)

-

– Item 9: In general, non-family members who work in the company maintain close social relationships because they share information and rely on each other to conduct business.

-

– Item 10: In general, non-family members who work in the company keep their promises and are loyal to the company.

COGNITIVE DIMENSION (α=0.85)

-

– Item 11: In general, non-family members who work in the company share the same ambitions, vision, and values.

-

– Item 12: In general, non-family members who work in the company pursue the same objectives and mission.

Measures of Family Firm Innovation – Likert (1-5) (α=0.73)

Please indicate your agreement with the following three statements with respect to the family firm innovation. For your rating, take into account that ‘1’ is to express that you completely disagree and ‘5’ that you completely agree.

-

– Item 13: The rate of introduction of new products or services in the organisation has grown rapidly in the last five years.

-

– Item 14: The rate of introduction of new production methods or services rendered in the organisation has grown rapidly in the last five years.

-

– Item 15: In comparison to its competitors, the organisation has become much more innovative in the last five years.