In their impressive history of the relationship between politics and banking in the modern western world, Calomiris and Haber (Reference Calomiris and Haber2014) posit as their central explanatory device a ‘Game of Bank Bargains’. Working within the rules set by their particular socio-political institutions, governments interact with bankers, minority shareholders, debtors and depositors. ‘Coalitions among the players form as the game is played, and those coalitions determine the rules governing bank entry (and hence the competitive structure and size of the banking sector), the flow of credit and its terms, the permissible activities of banks, and the allocation of losses when banks fail’ (p. 13). For the British case, drawing upon the work of Broz and Grossman (Reference Broz and Grossman2004), Calomoris and Haber find that over the eighteenth and nineteenth centuries the government and the Bank of England negotiated a series of ‘“loans for rents” contracts’ (p. 91). Specifically the government secured loans by granting and repeatedly extending the Bank of England's monopoly over chartered banking. The Bank passed some of its monopoly profits along to the state in the form of a lower interest rate on its public loans. Cox (Reference Cox2015) offers a similar account.

In this article I examine one very specific interaction between the British government and the Bank: the introduction of two new series of Exchequer bills in 1707 and 1709 respectively. I find the loans-for-rents thesis doesn't fit and offer an alternative explanation for the government's decision during these same years to renew and strengthen the Bank's monopoly. The new Exchequer bill issues were an attempt to address a pressing problem in Britain's monetary system at the time: the scarcity of gold and silver specie. It was this same problem that eventually led the government to extend and even strengthen the Bank's monopoly. In so doing it wasn't authorizing the Bank to prey upon the general public. Rather it hoped to encourage the currency of Exchequer bills and Bank notes. Indeed, during the Exchequer-bill project, government and Bank worked to keep tax collectors and goldsmith bankers from profiting by their privileged access to tax-related specie flows.

The article also offers a short history of the two new Exchequer-bill issues. They were a fascinating monetary experiment: an attempt to get the general public to accept a new paper currency – at times convertible into specie and at other times not – as a major means of payment in the country's system of war finance. Curiously, in his fine study of British Monetary Experiments, 1650–1710, Horsefield (Reference Horsefield1960) chose to ignore this episode, maintaining that its study ‘belongs to fiscal rather than to monetary history’ (p. 124). Ironically it was the fiscal historian Dickson who drew attention to the monetary aspect of the new Exchequer bills. He noted their resemblance to England's treasury orders and France's mint bills (1967, pp. 378–9). Alas Dickson's account is technical and bloodless. I try to convey the moments of keen interest, even high drama, in their story.

Section i introduces the period's principal monetary and fiscal institutions. Sections ii and iii respectively tell as much of the story of the two new issues as the available evidence will permit. I draw principally upon the minutes of the Treasury (NA, T29/14-19 [henceforth Treasury Minutes]) and the Bank's Court of Directors (BEA, G4/6-7 [henceforth Bank Minutes]) and a digital transcription of the Bank's General Ledgers (BEA, ADM7/5-6 [henceforth Bank Ledgers]). The latter volumes in particular – unless otherwise indicated, the source of all figures in this article – help fill large holes in even the most detailed secondary accounts: Clapham (Reference Clapham1958) and Dickson (Reference Dickson1967). Section iv draws out the implications for Calomiris and Haber's account of the politics of banking in early modern England.

I

The War of the Spanish Succession (1701–14) entailed massive amounts of extraordinary government spending: for the core years of 1702–12 an average of £7.8 million per year compared to £3.2 million in 1700 (Jones Reference Jones1988, pp. 70–1). Public revenues struggled to keep up, in two ways. First, never did annual income match annual spending. Average revenue for the period was £5.3 million per year (Jones Reference Jones1988, pp. 70–1). This meant large and ever-growing quantities of public borrowing. Most of it was long-term in nature: at first long-term annuities (Dickson Reference Dickson1967, pp. 60–3) and later lottery loans – in effect perpetual government bonds, most offering a normal rate of interest but a small portion, randomly allocated, paying premium rates (Dickson Reference Dickson1967, pp. 72–3). Second, tax revenues came into the Exchequer months, the dregs of them years, after the spending they were meant to finance had already taken place. This is one reason why revenue officials favoured annuity and lottery-loan acts. They brought in cash almost immediately, money that could be applied right away to meet the Treasury's most pressing needs; the first interest payments weren't due for another year, by which time the relevant tax proceeds should already have begun arriving. To cope with the revenue lag a complicated system of short-term finance was devised (for the details see Dickson Reference Dickson1967, pp. 341–453). When parliament approved a given tax, the Exchequer issued ‘tallies’ in the amount of the anticipated proceeds. Created in denominations ranging from £50 to £10,000 but typically for £500 or £1,000, tallies were a promise to pay the bearer so much of the relevant tax proceeds as they arrived in the Exchequer. Tallies were given out to anyone willing to lend cash today for future repayment. They bore interest – during our period typically at 5 or 6 per cent – payable to bearer, i.e. transferable. Under normal circumstances the Exchequer could find lenders for a third to half of the anticipated tax proceeds. The remaining tallies were assigned to some military paymaster, paying no interest until the Treasury authorized their actual use. Paymasters generally paid for wages and supplies in the first instance with paper: debentures, bills, etc. – instruments that typically bore no interest for at least the first six months. But to maintain good relations with creditors, paymasters needed to furnish actual cash at some point. They regularly solicited the Treasury for the right to convert some of their tallies into cash for this purpose – a gift the Treasury bestowed grudgingly and only upon those more desperate than the rest. Paymasters might offer their tallies, appropriately discounted, directly to creditors in settlement of their bills. More often they had to discount tallies with some third party, or borrow upon their security, paying suppliers with the cash proceeds. All the tallies on a given tax were sequentially numbered and had to be paid off in strict sequence.

The following short study of the Bank's balance sheet is essential for understanding the Bank's role in public finance. In keeping with the conventions of double-entry accounting, assets and liabilities were recorded as balances on the debit and credit sides of the relevant accounts respectively. Throughout the article I use net debits (debits less credits) to report account balances, meaning assets and liabilities show as positive and negative quantities respectively. The Bank's principal assets were the long-term loan of £1.2 million it had floated the government upon its creation in 1694 (what the General Ledgers refer to as ‘the fund of the Bank’), tallies and a store of specie (the ‘treasury’ account). Its main liabilities were stock and/or cash calls, bank bills and cash notes (see Figure 1).Footnote 1 Bank bills were one-year certificates of deposit, typically paying interest at 3 per cent per annum. Cash notes could be exchanged for specie upon demand but typically bore no interest. Note the Bank's bill and cash-notes accounts report the quantities in circulation rather than its own holdings. Consequently debit and credit entries represent issues and cancellations respectively.

Figure 1. Running balances (£) on main accounts, 1703–7

The Bank's principal function was to support the government's system of short-term finance. By offering a modest interest rate on bills, it was able to attract and hold a certain quantity of coin. With this specie the Bank could both satisfy the normal run of note holders’ needs for liquidity and keep a reserve large enough to meet even very large surges in liquidity demand. The Bank then issued cash notes to purchase comparable quantities of tallies – most of which were held until they came due at the Exchequer. The model worked well as long as some portion of the notes remained out in circulation. It was relatively risk free in that the Bank typically acquired tallies only when they were a few months away from coming due for payment. Hence even if the public grew unwilling to hold the usual quantity of cash notes, the Bank could replenish its specie reserves in short order by other means. The Bank was a very large player in the tally market. Consider for instance two of the largest and most regular revenue sources – the land tax and malt duties. During our period they were expected to bring in £1.85 m and £650k respectively per annum. Treasury records show average loan receipts on these funds of £1.19 m and £372k per year for the tax years 1703 to 1706 (Great Britain, Public Record Office 1936–52). Over those years the Bank held about £500k and £166k in the two types of tallies respectively (General Ledgers).

The very large monetary flows associated with the nation's system of public finance consistently put the Bank's business model under pressure. Table 1 lists all the Acts for our period by which the government raised revenue for the war. Typically, money surged into the Exchequer right after a major revenue Act passed, as lenders sought early tallies or investors queued to purchase annuities. Treasury records tell us nothing about the specific monetary media in which Exchequer loans or annuity purchases were received or how rapidly the money made its way into the hands of military paymasters and their creditors. But Figures 2 and 3 show that whenever a major revenue Act passed or a related instalment payment came due, large quantities of notes returned upon the Bank, there were relatively large withdrawals from the drawing accounts, and the Bank moved a lot of specie from the vault into cash. This didn't present a major problem as long as specie eventually found its way back to the Bank. And such was the normal pattern; the Bank's specie stores fell when new revenue Acts passed in the winter and built back over the ensuing three quarters. Before 1707, the norm was disrupted only by the Jacobite invasion scare of December 1703 and the very large annuities purchases of 1706.

Figure 2. Cash-note cancellations and drawing-account withdrawals (£), 1703–7

Figure 3. Treasury (vault) daily net withdrawals (£), 1703–7

Table 1. Extraordinary war supply Acts, 1703–11

It was probably concern about its specie stores that moved the Bank in 1707 to undertake a new long-term loan to the government via Exchequer bills rather than in its own cash notes. It was contemplating a loan because this was parliament's asking price for extending the Bank's charter – scheduled to end in 1710. On 6 February 1707 the governor presented the Commons with a ‘proposal for prolongation of the Bank’ (Bank Minutes). It took the form of an offer to lend a further £1.2 m at 5 per cent per annum (Luttrell Reference Luttrell1857, 6:135). That same day the Commons also received a proposal from a consortium of merchants and goldsmiths to lend £1.5 m at 6 per cent by means of Exchequer bills. A week later this group reduced its ask to 5 per cent (Luttrell Reference Luttrell1857, pp. 136, 139). No doubt they were hoping to displace the Bank from its leading role in short-term public finance. The Bank countered with a revised proposal to lend £1.5 m at 4.5 per cent by way of Exchequer bills and to take interest payments for the first three years in the form of further Exchequer bills rather than in specie (Luttrell Reference Luttrell1857, p. 6:139). The Bank's proposal was implemented by a statute passed on 25 March 1707 (5 Ann. c. 13).

The new loan was a strange beast – floated in a currency printed and issued by the Exchequer itself. The Bank's sole role – the only reason parliament agreed to pay it interest – would be to ‘circulate’ the bills. Specifically, the Bank had to provide the equivalent amount of specie upon demand to anyone presenting an Exchequer bill for encashment. The Treasury hoped this promise of redemption, together with its own commitment to accept Exchequer bills for tax payments and loans, would suffice to turn them into money – to get members of the public, military contractors in particular, to accept them as a means of payment. Like Bank notes, Exchequer bills in this first issue were to pay no interest to bearer; their status as money was to derive solely from their convenience in clearing large payment obligations. The authorizing statute gave the Bank an option to make the bills pay interest to bearer, but out of its own pocket – at no additional cost to the Treasury. The Bank made no use of this option at first. So the Bank's only real cost was the potential call from Exchequer-bill holders upon its specie stores. This is why the statute also authorized the Bank to make cash calls upon its shareholders: in case more was needed to support circulation of the bills.

That both the Bank and goldsmith consortium offered to lend to in Exchequer bills rather than in their own notes suggests the former currency was expected to minimize strain on scarce specie supplies. They may have thought investors would hold bills more readily than notes because the former could also be used for tax payments and Exchequer loans while the latter could not. In this connection it is remarkable that the Bank's proposal to parliament included an offer to receive interest, for the first three years of the loan, in further issues of Exchequer bills rather than in specie. Indeed, this may well have been the Bank's clinching argument. For it would have relieved the government for another few years of the need to find taxes with which to pay interest – important since the tax fund parliament eventually assigned for this purpose was already spoken for until August 1710. But it would also have deprived the Bank of an important channel by which to replenish its specie stores each year after the high season of Exchequer war loans had passed. Bank directors must have calculated they could withstand this drain: that their dominant position in the banking sector would carry them through. In this expectation the Bank was soon to be proven sadly mistaken.

I close this section with a brief word on the fiscal status of the Bank's cash notes. Economic historians usually assume that by our period they were readily accepted in tax payments and Exchequer loans (e.g. Clapham Reference Clapham1958, pp. 20, 23, 56; Quinn Reference Quinn2000, pp. 18–19; Rowlands Reference Rowlands2012, p. 114; Desan Reference Desan2014, pp. 311–15). Indeed, Quinn believes Bank notes were the ‘dominant form of payment’ in Britain's system of public finance by this time and questions the view of a Treasury historian (Baxter Reference Baxter1985, pp. 124–8) that the Exchequer was still a specie-based operation. But evidence for the standard view is slim. Clapham observes that in a statute of October 1698 (9 Will. III c. 44, §79) the Treasury agreed to accept Bank bills at the Exchequer (1958, p. 56). He neglects to mention, however, that this was only until the end of the next session of parliament (subsequently renewed once more in 10 Will. III c. 11, §13). And of course Bank bills were a very different currency than Bank notes. Rowlands cites a single sentence from a 1702 memorial by John Law. The sentence in question says only that Bank notes were acceptable for paying customs duties. Quinn offers a reference to Davenant. But the passage in question again refers only to customs duties. His econometric evidence for the proposition that Bank bills and notes were accepted in tax payments comes from the period 1695–6 – when the nation's silver money was being recoined and by necessity payments were made almost exclusively in paper. Finally Desan cites a nineteenth-century historian claiming that Bank notes were accepted at the Exchequer ‘[a]t the beginning of the eighteenth century’. But the historian's only evidence for this claim is a parliamentary report on Exchequer practice very late in the century. On the other hand, there is substantial evidence for the proposition that the Exchequer dealt principally in specie, not Bank notes. John Broughton, a frequent commentator upon the Bank during the war, acknowledged the Exchequer might on occasion have accepted Bank notes. But he hinted this was done only ‘collusively’ and from ‘a friendship to the Bank’ (Reference Broughton1705, p. 6). Broughton surmised the government was reluctant to go further because ‘the paper in the Exchequer has too great a dependance [sic] on the money in the Bank or bankers hands and may sink in its value at once if they should either withhold payment or be accidentally disabled only for a small space of time’. Note too that while the statutes authorizing Exchequer bills in 1697 (7 & 8 Will. III c. 31, §70) and again in our period (5 Ann. c. 13, §5, and 7 Ann. c. 7, §42) explicitly conferred legal-tender status upon them for taxes and Exchequer loans, the statute authorizing creation of the Bank of England (5 & 6 Will. & Mar. c. 20) said nothing of the kind about Bank bills or notes. Moreover, Bank minutes are filled with references to tellers working with bags of coin – some of them specific to dealings with the Exchequer (e.g. 10 July 1700, 6 and 14 April 1703, 13 March 1707).

II

If the Bank hoped the new Exchequer bills would mostly remain in circulation and generate little call upon its specie reserves, it was quickly and rudely disappointed. In March 1707 the directors prepared by ordering a 10 per cent cash call upon shareholders, payable just before the new bills began appearing in late April (Bank Minutes, 20 March). Issues rose steadily and by mid August had almost reached the legislative ceiling of £1.5 m (Bank Ledgers). As Figure 4 shows, from the outset over half the issue quickly returned to the Bank for encashment. Hoping perhaps to disrupt the early trend, on 8 May the Bank announced it would give out Exchequer bills to anyone bringing in a corresponding amount of money or Bank notes (Bank Minutes) and placed an ad in the London Gazette declaring that it stood ready to cash Exchequer bills upon demand. A week later the directors ordered a second 10 per cent cash call upon the shareholders, scheduling payment for late July. In the meantime the directors offset the resulting specie outflow by running down the Bank's loan balance and its holdings of Exchequer tallies (see Figure 5). The situation stabilized for a time in June but in July and August a great many more Exchequer bills came in. On 4 September a third 10 per cent call upon the subscribers was ordered, this one payable in October. But still more Exchequer bills came in that month. The directors elected next to issue more Bank bills. Between 6 November 1707 and 15 January 1708, £460k in new issues were ordered atop the £936k already extant (Bank Minutes, 6, 20 November; 4, 11, 31 December 1707; 8, 15 January 1708). There were limits to this strategy, however. The statute authorizing the Bank's creation had placed a ceiling of £1.2 million on the quantity of bills that could be outstanding at any one time – a constraint that had been reached by mid December. The Bank used the session's new land-tax act, passed on 18 December 1707, to pay a lot of bills into the Exchequer. But an equal value had returned within three weeks, almost halving the Bank's specie reserves in the process.

Figure 4. Exchequer bill holdings (£), 1707–11

Figure 5. Running balances (£) on main accounts, 1706–9

The onset of a major political crisis pushed the Bank very near the financial edge. News first arrived in London on 26 February 1708 of an intended Jacobite landing in Scotland (for a running account see Luttrell Reference Luttrell1857, pp. 279–83). That same day, for the first time ever, the directors ordered the issue of Exchequer bills that would pay interest to bearer – in this case at the rate of about 3 per cent per annum (Bank Minutes, 26 February 1708, 4 March 1708). The Bank converted £180k of its non-interest-bearing Exchequer bills for this purpose. It also entered almost a further £200k of non-interest-bearing Exchequer bills into the cash on 10 March. Perhaps this was because the directors anticipated the public would rather hold a public currency than its own liabilities. Indeed, Bank bills and notes began returning quite rapidly on 12 through 14 March. Apparently not everyone was prepared to take Exchequer bills in exchange, for the Bank was also forced to withdraw large quantities of specie from the vault on these days. On the 13th the directors halted all discounting of commercial bills (i.e. new private lending). Two days later, with the treasury balance now below £100k, they resolved to double the interest rate on all existing Bank bills to 6 per cent until 24 June and to issue new bills at this rate to anyone wanting to exchange them for Exchequer bills, Bank notes or ready money. The directors also arranged for a 20 per cent call upon the stock – due on 20 April but with a 2 per cent premium for payment before 20 March (Bank Minutes, 13 and 15 March 1708). We know that around this time several prominent aristocrats came to the Bank's aid (Boyer Reference Boyer1708, p. 355) and that the Treasury ordered government receivers to return their tax proceeds to London by way of the Bank (Bank Minutes, 18 March 1708). On 18 March the Commons also agreed to a clause preventing any other corporations but the Bank from issuing cash notes payable in less than six months (Great Britain, Parliament, House of Commons 1803, p. 616). Whether for these reasons or because the invaders were soon contained, by the end of March the Bank's situation had stabilized. In April discounting of commercial bills resumed in stages (Bank Minutes, 8 and 16 April 1708) and specie holdings slowly recovered. But the invasion scare seems to have left the public more wary of Exchequer bills. By the end of April the Bank was holding £1.2 m – some 80 per cent.

The remaining year of the first issue held no new surprises. But neither did it bring any marked improvement. Over the next few months the Bank was able to push £500k in Exchequer bills back into circulation, reduce the number of Bank bills outstanding, repay £100k of the recent cash calls in a large fall dividend, and build back its specie stores to £400k. But from September onward the Bank's treasury balance steadily declined, falling back to just £200k by the new year. And after October 1708 (other than for a short period in late December) the Bank's holdings of Exchequer bills settled above £1 m.

So on balance the first new Exchequer bill issue had not been a good business move for the Bank. On the liabilities side it had led to a contraction of cash notes in favour of Bank bills and cash calls – thereby increasing the Bank's obligations to pay out interest and, ceteris paribus, diminishing the effective rate of return for shareholders. On the assets side the Bank had in effect swapped Exchequer bills for a large part of its holding of tallies: a losing proposition given that the two assets paid rates of return of 4.5 per cent and (mostly) 6 per cent per annum. In the process its specie stores had come under considerable, indeed unprecedented pressure.

III

The Bank's participation in the 1707 issue had been an opening gambit in the negotiation to get its charter extended by parliament. Early in 1708 Treasury Secretary Lowndes argued in the Commons ‘that circulating exchequer bills by the bank last sessions was next to a renewal of the bank; and if they would now advance 800,000l. at 5l. per cent, he thought they could not doe better than prolong their time’ (Luttrell Reference Luttrell1857, p.259). The House did not follow up on his suggestion that year. But early in 1709 the Treasury proposed very specific terms for renewing the Bank's charter. The Bank would add another £400k to its initial long-term public loan of £1.2 m, at no additional interest charge. The first issue of Exchequer bills would be converted to a regular loan at 6 per cent per annum. And the Bank would circulate £2.5 m in new Exchequer bills ‘on ye present foot they [the old bills] now are’ (Bank Minutes, 28 January 1709).

The Treasury's proposals tell us a little about how it regarded the first issue. The second proposition cut in two directions. It was most likely an acknowledgement that the 1707 issue hadn't proved as financially rewarding as the Bank had expected. For the Bank was now holding most of it – constraining its ability to invest in tallies, which carried a better rate of return. A loan at 6 per cent would help address that problem. And if the Bank agreed to the loan, this would also help it circulate a new issue of Exchequer bills. Specifically it would guarantee the Bank a new, steady (quarterly) influx of specie from the Exchequer in the form of interest payments on the loan. This is probably why the Treasury proposed the new issue of Exchequer bills be on the same plan as before, even though that first issue hadn't gone very well – because the Bank would now have greater liquidity resources with which to support it.

While the Bank's directors were prepared to accept the first two propositions, they declined the third (Bank Minutes, 28 January 1709). In their counter-offer three days later they were prepared to support a second issue only if the Bank could take subscriptions for doubling their stock and the interest rate on the bills was raised to 6 per cent per annum – half (specifically 2 pence per day per £100 or about 3.04 per cent) to those holding the bills and the other half to the Bank (Bank Minutes, 31 January 1709). The directors left no written explanation. But they probably reasoned paying interest to holders would help Exchequer bills function more like money, circulating among the public rather than returning rapidly upon the Bank for specie. And if even the new bills didn't circulate well, the Bank would have two forms of insurance: (a) a larger initial stock of specie and a larger pool of shareholders from which to draw more if needed (the most important effects of the stock doubling); and (b) an interest rate of at least 6 per cent on its investment (something closer to what it could have earned simply by discounting tallies). It wouldn't hurt either that with twice the stock it would be much harder for government to terminate the Bank's charter (the statutes granting or extending charters always required full repayment of the Bank's outstanding government debt before its corporate status could be revoked). The Treasury quickly agreed to the Bank's proposed amendments. The directors decided on a 20 per cent down payment from the new subscribers (Bank Minutes, 4 February 1709). A subscription book was opened 22 February and commitments for the whole of the appointed sum were taken in before 1 p.m. that day (Boyer Reference Boyer1709, p. 295).

There must have been something about Exchequer bills in particular that made Treasury officials ask the Bank to circulate another £2.5 m of them. For at the new rate of 6 per cent per annum the Treasury would be paying no less interest than on a standard long-term loan. The most likely reason is that Exchequer bills served as a vital means of payment in Britain's system of public finance. The anonymous author of A Defence of the Bank, usually assumed to be director Nathaniel Tench, claimed that almost 80 per cent of the ‘moneys lent to the government are paid into the Exchequer out of the cash of the Bank’ (1707, p. 43). Figures 2 and 3 above suggest he wasn't exaggerating. And Figure 6, compared with Figure 3, indicates a clear benefit to the Bank from the introduction of Exchequer bills; the pressure of Exchequer loans upon its clearing operations could now be met with Exchequer bills instead of specie. This was exactly the reasoning employed by governor Sir Francis Eyles in trying to persuade shareholders to support the second Exchequer bill issue: ‘it was evident to them all that the want of species in the kingdome required some remedy for the circulation of the great yearly paymts. to her majty. for carrying on the war and that perhaps no other remedy was to be found at this time but by Excheqr. bills’ (cited in Dickson Reference Dickson1967, p. 374). Presumably the Treasury had similarly noticed that Exchequer bills helped relieve the bottleneck associated with specie-only payments and receipts at the Exchequer.

Figure 6. Treasury (vault) and Exchequer bill daily net withdrawals (£), 1707–11

One important matter remained to be negotiated: the specific currency in which interest would be paid. In early March, the Bank was told ‘no ways or methods could yet be found out by the publick’ to pay interest from the outset in specie (Bank Minutes, 3 March 1709). The Treasury proposed that for the first few years interest be paid instead by further issues of Exchequer bills. Since a return flow of specie from Exchequer to Bank was vital for the success of the new issue, it isn't surprising that the directors countered with several new demands. The most significant was that the Bank not be required to cash Exchequer bills until they had been received at least once at the Exchequer in payment of taxes. Certainly this would directly reduce the strain upon the Bank's specie reserve. But the directors were probably also thinking tactically. For the proposed change would prevent military paymasters from simply taking newly issued Exchequer bills straight to the Bank for encashment. Instead they would have to persuade suppliers to hold the bills as short-term investments or use them in turn as a means of payment. This was the very goal for which Bank and Treasury alike had been aiming in any case. Perhaps this is why the Lord Treasurer (Sidney Godolphin) accepted the Bank's proposal the very next day (Bank Minutes, 4 March 1709). It was probably around this same time that one further design feature was added: a stipulation that the bills be cashable by all of the crown's revenue officers. Specifically, in the words of the statute (7 Ann. c. 7) the latter were ‘directed and required’ to pay the bills upon demand ‘out of any current coined money’ that they had received from taxpayers but not yet transmitted to the Exchequer. Note that unlike for the Bank, this condition applied immediately, whether or not the bills in question had already been received at the Exchequer in payment of taxes, and that revenue officers were not entitled to receive interest on any bills in their possession. The new measure would have had three beneficial effects. It would help increase circulation, since Exchequer bills could be exchanged for specie everywhere in the land rather than only at the Bank's office in London. It would make it harder for tax receivers to withhold specie receipts for their own private gain (a practice explored later in the section). Finally and most importantly it gave those holding Exchequer bills an alternative, indeed readier, way of satisfying any desire for specie.

At first all went well with the second issue. The authorizing statute received royal assent on 21 April 1709. By early June the Bank had taken in all of the old Exchequer bills and exchanged them for a new annuity (see Figure 7). The new bills began issuing out of the Exchequer in mid May. Late that month the Navy's cashier requested the Bank's assistance because he could not get his creditors to accept Exchequer bills. The Bank agreed to lend him £50k, taking as security an equal amount of ‘non-specie’ bills – i.e. those not yet received at the Exchequer in payment of taxes and so ineligible to be converted into specie upon demand (Bank Minutes, 26 May). But that was the last mention in the Bank's minutes of difficulties in getting the bills accepted. Total issues rose steadily, reaching £2.5 m on 1 October. As late as September the Bank was holding only £600k – at a time when almost £2 m had been issued. And during this early period the Bank's specie holdings climbed a little and then held steady. This was no doubt owing in part to the steady influx of new capital from the remaining four stock-doubling instalment payments – which came due in May, June, August and October (plus a special payment in July to cover the £15 by which the stock's market price exceeded the par value of £100 per share). The Bank Ledgers show the instalments were paid almost in full and very near their respective deadlines (see Figure 7).

Figure 7. Running balances (£) on main accounts, 1709–11

These early successes were due in part to measures the Bank took to encourage circulation of the new Exchequer bills. It urged the Treasury to instruct customs and excise receivers, when collecting on inland bills of exchange (a kind of cheque) that had been submitted in payment of taxes, to accept any Exchequer bills proffered for this purpose (Treasury Minutes, 9 May). On 14 May, and again on the 21st, the London newspaper Post Man featured a lengthy article introducing the new bills to the public – stressing that they would be received (and immediately credited with any interest owing) in payment of taxes and Exchequer loans and could be presented for encashment to tax receivers anywhere in Britain. When one paymaster asked the Bank to discount £50k worth of tallies, the Bank's directors agreed only on condition he take half of the loan in Exchequer bills (Bank Minutes, 30 May). Shortly thereafter the directors ordered that tallies on the land tax be discounted with Exchequer bills (Bank Minutes, 14 July, 4 August). Anyone wanting to discount foreign or inland bills of exchange was offered a lower interest rate (3 per cent instead of the usual 5 or 6) if they agreed to take Exchequer bills (Bank Minutes, 14 July). The final instalment of a new £400k loan to the government was paid with Exchequer bills (Bank Minutes, 28 July). And judging from the Bank's own holdings a much higher proportion of the 1709 than of the 1707 bills were issued in low denominations – which would have encouraged smaller investors to hold more.Footnote 2

Problems with the second issue first surfaced in October 1709. The likely occasion was the Bank's decision in late September to circulate a further £400k in Exchequer bills. Though the General Court (the Bank's label for shareholder meetings) unanimously supported the proposal (Luttrell Reference Luttrell1857, p. 492), the public was much less enthusiastic. Between early September and mid October another £400k in Exchequer bills returned upon the Bank and its specie stores fell by £160k or 44 per cent. In the first half of October, £200k of its own notes also came back for encashment. So it is not surprising that in late October the directors considered ‘what might most conveniently be further done for the circulation of Excheqr bills’ (Bank Minutes, 27 October).

Two counter-measures were implemented. First, the Bank's directors resolved ‘that specie Exchequer bills be issued out’ (Bank Minutes, 27 October). The phrase is ambiguous. But an order the next day to the Bank official overseeing interaction with the Exchequer suggests the most likely meaning: that any bills henceforth given out from the Exchequer to military paymasters would be classified as specie bills. This meant they would be eligible for immediate encashment at the Bank upon demand rather than as usual having to wait until they had been received back at the Exchequer in payment of taxes or upon loan. Second, the Treasury tried to police tax receivers more closely (Treasury Minutes, 1 November). Receivers were returning revenues to London by way of inland bills made payable to their agents there. The latter worked with London goldsmiths, ‘for private lucre’ the Treasury complained, to hold back specie and submit payment as much as possible in Exchequer bills instead. So the Treasury ordered its receivers to return tax proceeds instead via inland bills made payable to the Bank. Receivers were also ordered to send in their accounts fortnightly, as a way of checking their tendency to retain cash locally (where it could be loaned out via local bankers for private gain) rather than remit it promptly to London. Some receivers simply refused; late in the year the Treasury called in leading tax officials to complain ‘about receivers that do not transact by [i.e. via] the Bank’ or who were sending only trivial amounts of cash their way (Treasury Minutes, 30 December). Others complied only nominally. Later that month the Bank had to ask the Treasury to instruct receivers to stipulate that their inland bills should be ordered payable ‘in money’ (Treasury Minutes, 23 November). Presumably their London agents were offering payment in Exchequer bills instead and ready money continued to accumulate with goldsmiths rather than the Bank. Indeed, one land-tax receiver complained of exactly this.Footnote 3

These changes were not sufficient to address the Bank's problems. Its holdings of Exchequer bills continued climbing in the first half of November, reaching almost £1.2 m. The directors responded by trying to force more into circulation, ordering their cashiers to discount notes and inland bills only in this currency (Bank Minutes, 8 November). With specie stores still declining in November and standing by month's end at only £160k, they contemplated a much more aggressive measure: a cash call upon the shareholders for 25 per cent of the value of their stockholdings (Bank Minutes, 28 November 1709). With specie reserves falling off even more quickly in December (reaching £82k on the last day of the year), the directors acted on this idea. They got the General Court to agree to a 15 per cent call, payable in money or Exchequer bills and due on 25 February (Bank Minutes, 13 and 15 December; London Gazette, 15–17 December). The directors had resolved in advance that if shareholders approved the call, the Bank would start giving out specie, rather than non-specie, Exchequer bills. If the General Court declined, the Bank would stop discounting notes and inland bills with non-specie Exchequer bills, i.e. would try to reduce the number of such bills in circulation. Around this same time the directors also proposed that they, rather than the usual contractor (Sir Henry Furnese), remit the next £300k for the army in Flanders (Treasury Minutes, 12 December). They explained this would be ‘an ease to the Bank’. Their meaning is made clear in a subsequent communication from Furnese to the Lord Treasurer (NA, T1/117/23). Typically, the Treasury offered immediate payment to remitters for cash that would be delivered on the continent at a later date. In this case the Bank would take payment in Exchequer bills and arrange for a short-term credit from its European agents – who would pay out the equivalent amount on the continent in the currencies accepted there. This would keep a large quantity of Exchequer bills off the open market in the interim. By the time the Bank's short-term loans came due, Furnese noted, it would have acquired fresh supplies of specie.

Furnese was referring in part to the stock call already announced but also to an imminent public lottery loan. Both helped to repair the Bank's situation for a few months. The lottery loan was authorized by a statute that received royal assent on 18 January 1710 (8 Ann. c. 4). It was designed to raise £1.5 m up front (via tickets of £10 each) in exchange for a commitment from the crown to pay annuities of £135k for the next 32 years. The Treasury appointed the Bank to receive the loan payments and transmit them to the Exchequer (Bank Minutes, 16 January 1710). Though the payment deadline was 10 September, over half came in shortly after the subscription books were opened on 20 January – owing to the prompt payment discount of 8 per cent per annum (Bank Ledgers; Luttrell Reference Luttrell1857, p. 537; Boyer Reference Boyer1710, p. 335). The Bank did not record the currencies in which this cash was received or paid over to the Exchequer. But it used the occasion to build its specie store by about £200k. Between this and the cash call the Bank was able in March to absorb £400k in Exchequer bills without any adverse effect on the treasury account (Bank Ledgers).

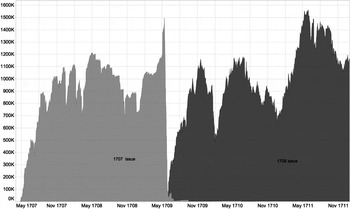

Unfortunately the relief was only temporary. In early April the Treasury summoned Bank officials to complain that ‘the discount on Exchequer bills not only continues but grows’ and demanded action (Treasury Minutes, 5 April 1710). No copy survives of the Bank's response, presented on 27 April. But we can guess at its contents from the Treasury's response two days later. Godolphin declared that ‘the most effectual method to prevent’ discounts was to order all tax receivers to ‘transact their affaires wth the Bank’ (Treasury Minutes, 29 April). In other words, tax receivers would again be ordered to return their money to London via the Bank rather than goldsmith bankers. Godolphin made two related orders that same day. First, receivers general in every county were to publish reminders about a provision in the original statute: that tax receivers were obliged to cash Exchequer bills upon demand out of any tax proceeds in their hands and to keep registers, open to the general public, of the money received from collectors. Second, receivers were now to send in accounts of the serial numbers and dates of the Exchequer bills they had cashed for members of the public or received from collectors. This would make it harder for receivers’ London agents, when withholding specie and offering payment instead in Exchequer bills, to maintain they were just passing along bills redeemed by the receivers locally. The Treasury introduced another change at this time, one that must have reflected its own analysis (since it came before the Bank's memorandum). Whenever paymasters came to the Exchequer to collect funds earmarked for them, they were to be paid not in ready money but in specie Exchequer bills. The new measures didn't reduce the discount rate on Exchequer bills (see Figure 8).Footnote 4 But at least things grew no worse. The problem wasn't mentioned again in Treasury or Bank minutes for some time.

Figure 8. Discount rates on Exchequer bills, 1710–11

But the Bank's situation had reached near crisis proportions by the fall. In July the discount rate began rising again and by late October stood above 3 per cent. The immediate cause seems clear: the financial uncertainty generated by a change in government. The discount rate began climbing as soon as it became known that Godolphin might be dismissed from his post, jumped a little when Robert Harley replaced him on 10 August, and really took off after 21 September, when Queen Anne dissolved parliament and replaced many of the leading Whig ministers with Tories. Investors were uncertain whether the new House of Commons, likely to be dominated by anti-war Tories, could be counted upon to approve the taxes needed to support public credit (Hill Reference Hill1971). The rising discount rate on Exchequer bills had an adverse effect upon the Bank's store of specie. The transmission mechanism can't be identified directly from the Ledgers, especially since notes and bills outstanding held fairly stable and the Bank's holdings of Exchequer bills declined. But the mostly likely cause was a decline in new specie inflows from the Exchequer – perhaps as Exchequer bills became a less acceptable means of payment generally and state creditors sought payment instead in coin. Certainly the Bank itself now began pressing the Treasury for its loans to be repaid ‘in money’ (Bank Minutes, 22, 24 and 31 August; 14 and 27 September; Treasury Minutes, 13 September). The Treasury also agreed to coin £100k in gold bullion, previously set aside for the army, to repay a recent Bank loan (Bank Minutes, 22 August). The directors pursued additional measures. Treasury requests for new loans, usually answered in Exchequer bills, were resisted. Ready money was raised by borrowing short term, via bills of exchange, from agents on the continent. Tellers were instructed to discount foreign bills of exchange only in non-specie Exchequer bills (Bank Minutes, 4 October). The fall dividend was to be paid in the same currency. Non-specie bills could be converted into Bank bills bearing interest at 6 per cent (Bank Minutes, 9 October). Finally, there was a 10 per cent call upon the stock, payable in ready money. The call was due on 20 December but with an early payment premium at 9 per cent per annum (Bank Minutes, 9 October); it produced £320k in new cash (over two-thirds by mid November) and spared the Bank the need to pay a further £175k in dividends (Bank Ledgers). These measures turned the tide for the Bank. Specie reserves fell to their nadir on 18 October and thereafter climbed steadily, reaching almost £200k by year's end.

But the high discount rate on non-specie Exchequer bills persisted. For the Treasury this meant significant losses and potential for a sudden crisis of confidence. Harley was therefore eager to find a solution. In early November he wrote a confidant that he was ‘upon a proposition which will immediately restore all our credit and make all Exchequer bills equal to money’ (Great Britain, Royal Commission on Historical Manuscripts 1897, p. 623). The basic idea must have been to offer the Bank inducements to stand ready to convert all non-specie to specie Exchequer bills. For Treasury Secretary Lowndes sent the Bank a draft one-year agreement to this effect in mid November, authorizing the Bank to issue a further £1 million in stock (Bank Minutes, 14 November). A week or so later the Bank submitted a counter-proposal (Treasury Minutes, 22 November). The details haven't survived. We know for sure only that the directors wanted the figure bumped to £1.5 m and a commitment by the Treasury to reduce its loan requests. Harley was clearly frustrated. Though the Treasury had offered ‘a great sum of money’ to reduce the discount, the Bank was unwilling to cooperate; ‘her majesty thinks it preposterous to press them’ any further (Treasury Minutes, 23 November). The directors denied they were unwilling to help (Treasury Minutes, 28 November), but no agreement was reached at this time.

The Treasury persisted in asking for more loans from the Bank. On one day alone in late November paymasters were authorized to seek another £110k (Treasury Minutes, 27 November). The directors approved part of the request but warned this would raise the discount on Exchequer bills (Bank Minutes, 30 November). The Treasury insisted (Bank Minutes, 7 December) and the Bank obliged a week later (Bank Minutes, 14 December). The paymasters converted these and other Exchequer-bill loans into specie at the prevailing market discount (see for instance NA, T1/126/42). When the Treasury later authorized one paymaster to seek a fresh Bank loan (Treasury Minutes, 26 December), the directors objected much more stridently (Bank Minutes, 29 December). They noted the Treasury now had about £600k in short-term Bank loans outstanding. They were all for two-month terms and to be repaid in ready money. To raise the necessary cash the Treasury would have to sell non-specie Exchequer bills. This ‘occasions great loss to the publick without any advantage to the Bank’ and might make it impossible to eliminate the discount. The directors invited the Treasury, instead of taking out new loans, to find some way of repaying existing ones.

This memorandum somehow broke the logjam. For the Treasury offered to repay half the loans with early tallies on the new land tax (very liquid securities) and invited the Bank to help reduce the discount on Exchequer bills. The directors accepted the offer and professed themselves very willing to consider any proposal for circulating non-specie Exchequer bills (Treasury Minutes, 4 January 1711).

Negotiations began straightaway. Lowndes sent the Bank a memorandum (Treasury Minutes, 8 January). The directors responded by offering to ‘undertake the circulation of all ye [Exchequer] bills as specie bills’ on condition the Treasury supply them with an additional £45k per annum (Treasury Minutes, 10 January) – no doubt in specie. The discount rate fell by half on 13 January when the Commons accepted this arrangement (Luttrell Reference Luttrell1857, p. 677). The authorizing statute (9 Ann. c. 7), passed on 17 March, guaranteed the Bank £45k per year in exchange for its commitment to cash all Exchequer bills, authorized it to contract annually with private investors for the requisite specie backing, and raised the statutory limit on Bank bills by whatever amount was called in upon the circulation contracts. The first annual circulation contract was opened on 23 March (Bank Minutes, 22 March). Well over half the down payment was taken in before month's end (Bank Ledgers). As Figure 8 shows, the remaining small discount on non-specie Exchequer bills completely disappeared that week. The Bank's specie reserves began climbing; by autumn they had reached nearly £800k – a level not seen since 1705.

IV

In one respect the two new Exchequer-bill issues worked as planned. Figures 3 and 6 indicate that in the Bank's operations Exchequer bills took on the role previously filled by specie in accommodating Exchequer loan and annuity payments. The significance of the achievement becomes more apparent when set beside the French case. Mint bills were originally issued as receipts for bullion brought to French mints for coining. But in 1701 the crown started to issue them outright to pay for military supplies – sheer credit creation. The bills were to bear interest at 4 per cent annum and be repaid in a few years. The government at first refused to accept them for tax payments. Later it agreed to take them as long as 75 per cent of the total payment was in specie. In part for this reason, by 1709 Mint bills carried a discount of 55 per cent (Bonney Reference Bonney2001). By comparison, British Exchequer bills were a raging success. By law they were acceptable in tax payments and war loans; Figure 6 shows this was also Exchequer practice. Only so can we understand why the Treasury agreed to pay the Bank an additional £45k per year to take on the circulation contract. This put the total interest rate on 1709-issue Exchequer bills at 8 per cent per annum. The Treasury must therefore have valued them as a means of payment, since a simple loan could have been secured at just 6 per cent.

But in another respect the experiment failed miserably. As a Bank spokesperson wrote at the time, ‘one chief end of making … [Exchequer bills], viz. of creating a new species of mony’, had not been realized (Scheme 1711). Rather than enhancing the total supply of credit, he continued, the new bills had simply diminished in equal measure the Bank's capacity to discount tallies and bills of exchange (an interpretation supported by Figure 5).Footnote 5 With the first issue most bills were quickly presented for conversion into specie and ended up stored in large bundles in the Bank's vault. A significantly larger proportion of the second issue remained in circulation, perhaps because they bore interest. But after a while the inconvertible variety went to a significant discount. The problem was repaired only after the Bank amassed a specie backing large enough to convince the public that Exchequer bills could always be changed for specie upon demand. Exchequer bills never became a perfect substitute for gold and silver coin. So Chartalists are simply wrong when they assert (see for instance Wray Reference Wray and Wray2004, pp. 242–6) that for anything to become money governments need only declare it will be accepted in payment of taxes.

The very failure of Exchequer bills to become a ‘new species of mony’ tells us something important about the architecture of Britain's monetary system at the time. Behind the scenes there was an intense struggle for access to gold and silver coin. Specie drained from the Bank's vaults because Exchequer bills afforded tax receivers and their goldsmith bankers new opportunities to amass large quantities of coin for their own purposes. The Bank valued tallies in part as claims upon Exchequer specie. As the discount-rate crisis deepened, it pressed for Treasury loans to be repaid in specie. It mattered greatly in which currency the interest on public loans was paid. Becoming a state lender was attractive in part because interest payments ensured regular influxes of specie. It was a considerable privilege to be invited to manage the subscription for a public loan, especially for an institution like the Bank that held large quantities of Exchequer bills; managers could take subscriptions in specie and settle with the Exchequer in bills. In the very terms of the circulation subscription we find an indication of specie's relative importance. If the scheme worked as designed it would afford subscribers a return of 21 per cent per annum.Footnote 6 As recent events have illustrated, the security being offered Exchequer-bill holders was illusory; in the event of an actual crisis, it would have been impossible for all of them to flee to the safety of specie. But the circulation subscribers would have faced ruin ahead of all the rest. At some level Bank and Treasury must have known this; for not otherwise would the one have demanded, and the other agreed to give, such a high price for this insurance.

Judging from the case of Exchequer bills, the relationship between Bank and Treasury was far different than Calomiris and Haber surmise. Their ‘loans-for-rents’ interpretation implicitly assumes the Bank had an extensive private business from which it could generate monopoly profits. But very little of the Bank's business was private. Only its loans and bill-discounting operations might fit this category. Yet almost all its loans were to military paymasters. And the Bank bragged that it discounted bills upon better terms than had goldsmith bankers before them (see for instance Tench Reference Tench1707, pp. 17–18). Yes, the Bank offered the two Exchequer-bill loans to secure an extension of its charter. But its profit came almost exclusively from these and other public loans. The government strengthened its monopoly to assist the Bank not in extracting rents (of which the state would have been the principal payer) but in supporting the currency of Exchequer bills and Bank notes. Much like with its orders to tax receivers, the Treasury was trying to encourage contemporaries to settle their payments through the Bank. This would help the Bank retain specie more easily and use that scarce resource to better effect in supporting public credit. Private borrowers may have suffered from the diversion of credit supplies toward the state, but not otherwise.