Since the 1970s, the idea that corporations should be managed in the long-run interests of their shareholders has dominated the literature on corporate governance.Footnote 1 Scholars who take this position generally agree that Anglo-American law does a better job of promoting shareholders’ welfare than the law in effect in most other countries.Footnote 2 Pointing to the common law's superior flexibility, they argue that the commercial codes put in place in France and elsewhere on the European continent in the nineteenth century locked businesses into a particular set of legal rules. In Britain and the United States, by contrast, the common law could adapt flexibly to the needs of business and the economy. Shareholder-friendly corporate governance rules emerged, they argue, as managers of large firms sought ways of committing credibly not to exploit outside investors.Footnote 3

This article uses data on corporate governance practices in Britain during the late nineteenth and early twentieth centuries to challenge the connection between the greater flexibility of the Anglo-American legal regime and shareholder-friendly governance. Beginning with the 1856 Companies Act, Britain's general incorporation statutes included few provisions regulating corporate governance. Instead, Parliament provided companies with a model set of articles of association that applied only if they did not write their own. Although the model covered most aspects of corporate governance, its provisions were default rules. Companies could reject any or all its parts and write alternative clauses of their own choosing. They could even write substitute clauses that explicitly negated the provisions in the model. So long as the clauses that companies adopted were not illegal, they were enforceable as contracts in court.Footnote 4

To explore the governance choices that incorporators made when they organized their businesses, we collected the articles of three random samples of companies formed in the late nineteenth and early twentieth centuries. We also collected the articles of a sample of companies whose securities traded on the London Stock Exchange (LSE) and other major British exchanges. We find that incorporators revised the model articles in ways that were anything but shareholder friendly. Whether companies were small or large or private or public, they tended to adopt governance structures that shifted power from shareholders to directors to such an extent that shareholders were for all practical purposes disenfranchised. These patterns, moreover, seem to have become more pronounced over time.

Our findings contradict those of scholars who have argued recently for the shareholder-friendly character of British corporate governance in the late nineteenth and early twentieth centuries.Footnote 5 An important reason we obtain different results is that we look at how the governance rules that firms wrote into their articles of association worked in combination, whereas other studies either focus on a narrower set of practices or do not pay adequate attention to the ways in which the various rules interacted. In offering this corrective, however, we are not siding with scholars who have emphasized the nefarious character of British corporate governance during this period.Footnote 6 It is easy to find examples of bad or even fraudulent management in the contemporary financial press, but after searching for news accounts of companies in our traded sample, we were struck by how little controversy the firms provoked. There seems to have been a general understanding that corporations were entrepreneurial vehicles that offered outside investors the chance to earn high rates of return in exchange for their passivity. Shareholders had voice, and they certainly used it when the returns they expected did not materialize. But they did not have much power within these enterprises, and there is little evidence that they pushed for more.

British Company Law and the Model Articles of Association

The contractual flexibility of British general incorporation law was a product of the mid-nineteenth century. Just a few decades earlier, businesses had faced a much more restrictive, even perilous, legal environment. The Bubble Act of 1720 had made it illegal for joint-stock companies to operate without the explicit permission of the government in the form of a charter. Charters were not easy to secure, however, and so despite the law, many multi-owner businesses organized as unincorporated joint-stock companies. These companies were essentially large partnerships structured by contracts that enabled them to concentrate managerial authority and function as if they were legal persons. Beginning in the second decade of the nineteenth century, a series of adverse court decisions made the legality of these businesses increasingly uncertain, and entrepreneurs responded by deluging Parliament with petitions for charters. Although relatively few of these petitions succeeded, Parliament repealed the Bubble Act in 1825, and the number of unincorporated joint-stock companies again began to rise.Footnote 7

The joint-stock company was still an inferior substitute for the corporation, however. Corporate privileges, such as the right to sue and be sued in the company name and especially limited liability, were cumbersome to secure contractually and not reliably enforceable. It was still not clear, moreover, that the form was legal under the common law, and indeed the sitting Lord Chancellor made known his views to the contrary.Footnote 8 In 1834, Parliament made another move toward liberalization by authorizing the Board of Trade to award companies patents that conveyed some corporate privileges, such as the right to sue and be sued as an entity. This effort failed, however, because the board set the bar for granting such requests too high. In 1837, Parliament expanded the board's powers, enabling it to extend to companies any privilege, including limited liability, that “it would be competent” under “the rules of the common law” to include in a charter of incorporation, but the board continued its restrictive policy.Footnote 9

In the face of the conservativism of the Board of Trade, entrepreneurs pushed for legislation that would enable companies to secure charters of incorporation with a simple registration process. Parliament took a first step to meet their demands in 1844 by passing an act granting corporate status to most nonfinancial companies that registered and met a set of minimum requirements.Footnote 10 The act, however, did not grant shareholders limited liability, included quite significant disclosure requirements for the benefit of investors, and also imposed a standard governance structure on registered companies. At the same time, it declared unregistered joint-stock companies to be illegal and prohibited partnerships with more than twenty-five members.Footnote 11 The next year, Parliament enacted the Companies Clauses Consolidation Act, which imposed a strict governance structure on companies chartered by special statute, mainly enterprises in the transportation, banking, and utilities sectors.Footnote 12

Entrepreneurs continued to campaign for limited liability, and Parliament finally complied with the passage of the Joint Stock Companies Act of 1856. This statute also marked a dramatic shift toward laissez-faire, dropping the financial disclosures required by the 1844 act as well as the detailed corporate governance rules it had mandated. Companies henceforth were to be governed by their articles of association. The 1856 act included as an appendix a model set of articles of association with many of the provisions previously imposed by the 1844 law. These articles were now default rules, however, not statutory requirements. They would govern companies that did not submit a set of articles, but incorporators could reject the model as a whole or in part and write their own rules.Footnote 13 This division between the text of the law, which included almost no provisions regulating companies’ internal governance, and an appendix with a default set of governance rules was repeated in the consolidated Companies Act enacted in 1862, and it continues to characterize British company law today.Footnote 14

The 1862 statute consisted of 212 sections spread over more than fifty-five pages, with more than twenty-five additional pages of schedules.Footnote 15 Most of the statute regulated the formation and winding up of companies and the responsibilities of the company and its shareholders toward creditors. Only a few provisions concerned internal governance, and even these mainly took the form of default rules. Thus, section 52 stated, “In default of any Regulations as to voting every Member shall have One Vote.” Section 49 required the company to hold a general meeting at least once a year, but left it to the company's articles to specify what would be done at the meeting. The only governance rule in the statute that applied inflexibly was a provision enabling shareholders to amend their company's articles of association by “special resolution,” that is, by a three-quarters supermajority vote of those in attendance at a general meeting called for that purpose, followed by a majority (confirming) vote at a second general meeting held soon after. Even in this case, however, the number of votes that each member of the company could cast was determined by the company's articles, not by the statute (see sections 50 and 51).

The model articles of association appended to the 1862 statute (labeled Table A) contained ninety-seven provisions that covered such matters as the transfer and transmission of shares, the conduct of general meetings, the powers of directors, procedures for declaring dividends, and requirements for the maintenance of accounts, annual audits, and the provision of financial reports to shareholders. Because the drafters assumed that most companies would be public in the sense of raising capital from a broad group of investors, they included a clause stating that shares would be freely transferable unless the owner was indebted to the company (Article 10). They also attempted to bolster the ability of smallholders to protect their own interests by specifying a voting rule that allocated one vote per share up to the first ten shares, one vote for every five shares up to one hundred, and then one vote for every ten additional shares (Article 44). Perhaps to ensure continuity in the management of the enterprise, the model articles stipulated that board members would hold overlapping terms, with one-third of the directors standing for reelection at every annual meeting (Article 58). Although this staggering of terms may have made it more difficult for shareholders to effect major changes in the composition of the board, Table A constrained the power of directors in important ways. Just one-fifth of the members of a company could force the directors to call an extraordinary general meeting (Article 32). Directors needed the approval of the general meeting to declare a dividend (Article 72) and increase capital (Article 26), with the latter requiring a three-quarters vote. The general meeting controlled directors’ remuneration (Article 54) and could remove any director through the process of special resolution (Article 65). The company's accounts had to be checked annually by auditors chosen by the shareholders (Articles 83 and 84). Shareholders had to be provided with a copy of the balance sheet at least seven days in advance of the annual meeting (Article 82). Moreover, shareholders had routine access to the company's accounts (Article 78).

Table A seems to have been intended as a model of good governance for companies to emulate. According to Robert Lowe, who introduced the bill in Parliament, its provisions were based on the rules that Parliament had embodied in the Companies Clauses Consolidation Act and also on the drafters’ opinions about articles frequently adopted by joint-stock companies.Footnote 16 To the extent that one can infer intentions from outcomes, it would seem that the drafters aimed to lean against contemporary trends. Mark Freeman, Robin Pearson, and James Taylor have collected the articles of association of companies formed between 1720 and 1844 and found that governance practices were shifting the balance of power toward directors. Based on their calculations, companies that adopted Table A in its entirety would have given shareholders much more authority relative to directors than was common among joint-stock companies at the time.Footnote 17 It seems, moreover, that contemporaries viewed Table A as a good model. As late as 1894, an advice manual aimed at investors commented that Table A “very fairly fixed the balance of power” between shareholders and directors.Footnote 18

The Data Sets

The model articles of association published in Table A were simply default rules. Whatever the drafters intended to signal when they crafted its provisions, incorporators could (and, we will see, often did) reject the model as a whole or in part. Companies were required to submit articles of association with their registration documents, so their choices are a matter of public record. In order to study the extent to which, and how, companies revised Table A, we collected from the U.K. National Archives the articles filed by random samples of companies registered in the years 1892, 1912, and 1927.Footnote 19 We also collected the articles of a sample of commercial and industrial companies reported in Burdett's Stock Exchange Official Intelligence for 1892 that had been formed no earlier than 1888. We compared each company's articles to those in Table A and hand-coded the deviations. Because the coding was so time-consuming, the target size for each sample was only about fifty companies.Footnote 20 The appendix contains a description of our sampling procedures and possible sources of selection bias. We base our discussion on the two 1892 samples (we call them the “registration” and “Burdett's” samples) and use the later samples to highlight long-term trends in the kinds of governance rules that companies adopted.

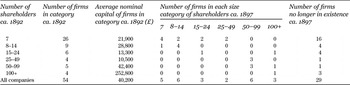

The firms in our 1892 registration sample ranged across a major part of the size distribution of companies. We were not able to find reports on them in Burdett's, suggesting that their securities were not publicly traded, but it is clear from their numbers of shareholders (see Table 1) that a significant proportion sought to raise capital from external sources. The smallest company in the sample had a nominal capital of only £100 and the largest £850,000, near the top of the range of our sample from Burdett's (compare Tables 2 and 3). The median nominal capital of firms in the 1892 registration sample was £10,000, and the average was £40,200 (close to the average of £37,700 for all registrations in 1892).Footnote 21 The law required companies to record at least seven initial shareholders at the time of registration. As Table 1 indicates, nearly half of the companies in the sample (twenty-six of the fifty-four) did exactly that, but nineteen listed fifteen or more shareholders, including five companies (average nominal capital £42,400) with between fifty and one hundred subscribers and four companies (average nominal capital £252,800) with one hundred or more. There is good reason to believe, moreover, that at least some of those reporting only the seven required subscribers aimed to distribute their shares more widely. Although most of the companies in this group did not survive five years, six of the ten that still existed in 1897 had increased their number of shareholders, and two had moved into the range of twenty-five to forty-nine.

Table 1 Distribution of Companies in 1892 Registration Sample, by Nominal Capital and Number of Shareholders in 1892 and 1897

Source: See the Appendix for a description of the 1892 registration sample.

Notes: We counted the number of shareholders reported at the time of registration and also the number reported five years later (or as close to that date as possible). Nominal capital is rounded to the nearest £100.

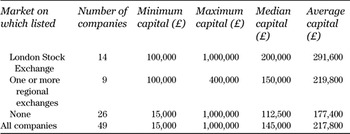

Table 2 Distribution of Nominal Capital of Companies in 1892 Burdett's Sample, by Market on Which Listed

Source: Burdett's Official Intelligence (1892). See the Appendix for a description of the sample.

Note: Nominal capital is rounded to the nearest £100.

Table 3 Distribution of Nominal Capital of Companies in 1892 Registration Sample, by Stance on Table A

Source: See the Appendix for a description of the 1892 registration sample.

Notes: The count of companies rejecting Table A includes two firms whose articles did not specifically reject (or accept) the table but that wrote articles including at least one hundred new clauses. Nominal capital is rounded to the nearest £100.

Table 2 reports the distribution of capitalization of companies in the Burdett's sample, broken down by whether the company's securities were formally listed on the LSE, on another securities market, or on neither. Not surprisingly, companies in the Burdett's sample tended to be much larger (average nominal capital £217,800) than those in the registration sample (£40,200). The companies in the Burdett's sample that were on the LSE official list were larger on average than other companies in the sample, but their size distribution overlapped with those listed on the regional exchanges and with those whose securities were not formally listed.Footnote 22

One might expect large companies, particularly those seeking outside investors, to write articles of association that looked very different from those of small, closely held companies. The literature on corporate governance suggests that companies that planned to raise funds externally would seek to reassure investors that they would be able to monitor and, if necessary, discipline corporate insiders.Footnote 23 By contrast, one might expect the articles of small, closely held firms to be shaped by two very different calculations. On the one hand, members might want to minimize the costs of incorporation by simply adopting Table A as written. On the other hand, they might want to write articles that addressed matters of specific concern to them, such as guaranteeing themselves an ongoing role in making decisions, vetting new members, and passing leadership positions on to their heirs.Footnote 24

Small companies do seem to have been more likely to accept Table A than other firms (see Table 3). Only four companies in the 1892 registration sample (7 percent) accepted the model table in its entirety (though even these companies wrote on average twenty-six additional articles). The median capital of these companies was just £3,000 (less than a third of the sample median), and their average capital was only £5,000 (an eighth of the sample mean). Almost as small were the twelve companies (22 percent) for which there were no articles in the file (median capital £5,000, mean £6,600). As noted above, if a company did not write its own articles the default rules in the model table applied, so it is possible that these companies simply accepted Table A. But it is also possible that the articles were simply lost. We will take both possibilities into account in our quantitative tests.

All of the companies in the 1892 Burdett's sample rejected Table A in its entirety. Twenty-eight of the companies in the registration sample (52 percent) also rejected Table A and wrote their own articles of association from scratch. These companies ranged across the size distribution, but on average they were substantially larger than the rest and included the five biggest companies in the sample. Another ten of the companies in the registration sample (19 percent) accepted some of the articles in Table A but rejected others, writing on average twenty-five new clauses.

In the next section we examine the content of the changes that companies made to Table A when they wrote their articles. What stands out in our findings is the high degree of uniformity in the provisions they wrote and the extent to which the changes were not of the sort generally regarded as shareholder friendly. More specifically, we observe a strong across-the-board tendency to rewrite the corporate governance rules in ways that increased the power of directors relative to shareholders, so that investors in large and small firms alike were for all practical purposes stripped of their power even to monitor what directors were doing with their money. With minor qualifications these changes were as (or more) prevalent in the Burdett's sample as they were in the general sample of 1892 registrants.

How Companies in the 1892 Registration and Burdett's Samples Modified Table A

Most empirical studies of corporate governance have followed one of two approaches: they have focused on a few key aspects of companies’ governance structures, such as voting rules or the procedures by which shareholders might call extraordinary general meetings; or they have constructed additive indexes that aim to summarize a more comprehensive set of governance rules.Footnote 25 Neither of these approaches captures the multifarious ways in which various provisions in a company's articles might interact with one another, and so they both can produce misleading results. For example, scholars have classified companies by their voting rules—whether they awarded each shareholder one vote per share or imposed graduated scales that limited the number of votes large shareholders could cast—but the impact of this choice could vary significantly depending on the issues on which shareholders could vote and the circumstances under which the formal voting rule came into play.

As already noted, the 1862 model articles specified a graduated scheme that limited the number of votes large shareholders could cast. Very few of the companies in the 1892 registration sample (only nine of the forty-two for which we have articles, or 21 percent) retained this or a similar schedule, with the rest moving to a one-share-one-vote rule (see Table 4).Footnote 26 The percentages in the Burdett's sample were almost the same, with only 19 percent of the companies sticking with a graduated scheme. Scholars have disagreed about the impact of this shift on corporate governance, but they have not sufficiently appreciated the extent to which voting rules must be considered in the context of other governance procedures.Footnote 27 For example, the practice in British companies was to decide all motions in the first instance by a show of hands and only bring the voting rule into play if some threshold number of shareholders called for a poll.Footnote 28 This procedure might seem to be an egalitarian one: in a show of hands each shareholder had one vote. But, again, how it worked depended on other rules, such as the size of the quorum required to hold a general meeting, the procedure to be followed if shareholders demanded a poll, and the ability of shareholders to vote by proxy.

Table 4 Percentage of Companies Revising Table A in Specified Ways

Source: See the Appendix for a description of the samples.

Notes: Percentages for the registration sample pertain only to the forty-two companies with articles in the file. For the variables relating to financial accounts, the number of observations for the registration sample is only forty-one because we are missing the relevant page of articles for one of our companies. There are forty-nine companies in the Burdett's sample, but the observation for the first variable is missing for one company.

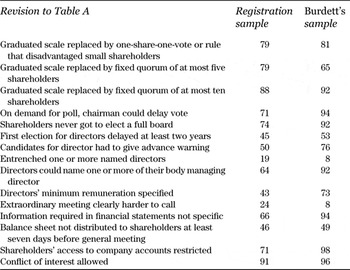

Table A specified a quorum that rose with the number of shareholders. If the number of shareholders was ten or fewer, the quorum was five; it then increased in steps with the number of shareholders to a maximum of twenty (Article 37). Only four companies in the registration sample and one in the Burdett's sample adopted the default rule. In the registration sample, 79 percent of the companies specified a quorum that was as low as, or lower than, the default minimum of five members for companies with up to ten shareholders, and 88 percent specified a quorum of ten members or fewer. In the Burdett's sample, 65 percent of the companies had a quorum of five or fewer, and 92 percent, ten or fewer.Footnote 29 Such low quorums meant that it was possible for directors to run a general meeting and decide all business among themselves with few if any other shareholders present.

The rules governing the taking of polls also affected how voting worked. All companies in our samples included in their articles a provision enabling some minimum number of shareholders (often a number equal to or lower than the number required for a quorum) to demand a poll—that is, a formal ballot that followed the company's voting rule. According to Table A, if a poll was demanded, “it shall be taken in such manner as the chairman directs, and the result of such poll shall be deemed to be the resolution of the company in general meeting” (Article 43). A possible interpretation of this default rule was that the poll would be taken right away, but most companies specifically rejected that view.Footnote 30 Fully 71 percent of the companies in the registration sample and 94 percent of the Burdett's companies wrote substitute articles that allowed the chairman to adjourn the meeting and postpone the poll until some date in the future.Footnote 31 Such a rule allowed directors to behave strategically and schedule the poll for a time that enabled them to round up additional votes. Usually, however, directors controlled enough proxy votes to get their way without delaying the vote. Table A specified that shareholders could vote either in person or by proxy (Article 48), and all of the sample companies adopted this provision or a close substitute. Contemporary newspaper accounts suggest that directors typically controlled enough proxies to dominate in a poll and that they called for polls when necessary to push through their agenda.Footnote 32

The main item on which shareholders voted at general meetings, besides the annual dividend, was the election of directors. Table A let a company's founders (the subscribers to the original memorandum of association) choose the initial directors (Article 52); then, these would step down at the first general meeting, and shareholders would have an opportunity to elect a new board. In every subsequent year, one-third of the directors had to stand for reelection if they wished to remain on the board (Article 58). Today staggered boards are thought to reduce shareholders’ power, but it appears that policymakers at the time considered them useful to preserve managerial continuity. In any event, only one firm in our 1892 samples sought to do away with the practice by requiring all the directors to stand for reelection at each annual meeting. Most of the other companies (74 percent of those in the registration sample and 92 percent of those from Burdett's) moved instead in the opposite direction and started the fractional rotation at the first election, so shareholders never got a chance to choose the full board. Many companies (45 percent of the registration sample and 53 percent of the Burdett's) also delayed the timing of the first election at least two years (and often longer).Footnote 33 In addition, 50 percent of the companies in the registration sample and 76 percent of the Burdett's companies added a provision that was not in Table A requiring anyone seeking the office of director, except a retiring director or someone chosen by the existing board, to provide advance notice of his intention to run. Presumably the directors wanted to be sure that they would have time to line up the votes to block anyone whom they did not favor from securing a seat on the board.

Many companies included provisions in their articles that insulated at least some of their directors from the need for shareholders’ approval. Eight companies in the registration sample (19 percent) and four in the Burdett's sample (8 percent) went so far as to entrench specific directors for a lengthy number of years or even for life. A much more common technique was to add a provision to the articles that enabled members of the board to designate one or more of themselves “managing directors.” There was no provision for a managing director in the 1862 Table A, but 64 percent of the firms in the registration sample and 92 percent in Burdett's added a clause that empowered directors to give themselves this title, either for a fixed term or “without limitation.” In most cases, the clause also explicitly exempted managing directors from having to stand for reelection while they held the office.Footnote 34 Thus, by designating themselves managers, directors could perpetuate their power indefinitely. Moreover, they could also control their own remuneration. Table A left the determination of directors’ pay to the general meeting, though 43 percent of the companies in the registration sample and 73 percent from Burdett's limited shareholders’ discretion by specifying at least a minimum annual payment. The remuneration of the managing directors, however, was set by the board and could take the form of a salary, a commission, and/or a proportion of the profits. In other words, directors could name themselves managing directors and take a share of their company's earnings off the top, before the calculation of dividends.

At least in theory, directors could be removed by the shareholders. The overwhelming majority of the companies (76 percent in both samples) followed Table A in giving shareholders the authority to depose directors by a three-quarters vote (Article 65) or occasionally less.Footnote 35 Most also made it easy to call extraordinary general meetings for this or any other purpose, either by adopting Table A's provision that directors had to call such a meeting upon the request of one-fifth of the shareholders (Article 32) or by substituting another provision that was equivalently accommodating. There was a lot of variation in such clauses, but only a few companies (24 percent of the registration sample and 8 percent of Burdett's) made calling an extraordinary general meeting clearly more difficult than the Table A rule.Footnote 36

In combination with the election procedures we have already described, the three-quarters supermajority requirement meant it was difficult to dislodge directors in practice. Nonetheless, companies typically modified Table A in ways that both increased directors’ power and limited shareholders’ ability to monitor how that power was used. For example, the most important item on the agenda at the annual shareholders’ meeting, besides voting for at least some directors, was the declaration of dividends. The standard procedure was for directors to propose the amount of the dividend and shareholders simply to approve their recommendation.Footnote 37 The articles of almost all companies specified that shareholders could not raise dividends above the level recommended by the directors. Dividends could only be paid out of profits, and directors had the power to determine what those profits were and also to set aside whatever they thought the enterprise needed as a reserve. As already noted, moreover, directors determined the amount of revenues that would be taken off the top in the form of salaries and commissions to managing directors (and other officers).

Shareholders had very little ability to check or even to monitor those decisions. Although the articles of all of the companies in our samples required directors to lay some type of audited financial statement before the shareholders at each annual meeting, most companies (66 percent of the registration sample and 94 percent of Burdett's) watered down Table A's specific requirements that the statement “shall show, arranged under the most convenient heads, the amount of gross income, distinguishing the several sources from which it has been derived, and the amount of gross expenditure, distinguishing the expense of the establishment, salaries and other like matters” (Article 80) and that the statement must be “made up to a date not more than three months before” (Article 79). A significant number of companies (46 percent of the registration sample and 49 percent of Burdett's) also scrubbed the obligation to send shareholders copies of the balance sheet at least seven days in advance of the annual meeting (Article 82).Footnote 38 Most companies, moreover, rejected Table A's requirement that directors keep the account books at a registered office of the company, where they “shall be open to the inspection of the members during the hours of business” (Article 78). In 71 percent of companies in the registration sample and fully 98 percent in Burdett's, directors were given the power to determine whether and to what extent shareholders could examine the company's accounts.Footnote 39 Of course, there may have been good reasons for companies to limit shareholders’ access to the books. Incorporators certainly worried that by buying a share in their company a competitor could gain access to information about the business that might give it some advantage. But the same concerns cannot explain the dilution of the annual reports.

In addition to shifting the balance of power in favor of directors, most companies modified their articles of association in ways that made it possible for directors to engage in self-dealing. Table A included a strict rule precluding directors from being on both sides of a contract with the company (Article 57), but almost all of the companies (91 percent of the registration sample and 96 percent of Burdett's) adopted a laxer standard and allowed directors to contract with the company.Footnote 40 In most (though not all) cases, the articles specified that directors had to disclose any conflict of interest to the board and refrain from voting on matters in which they were interested. Today, the corporate governance literature generally frowns on provisions allowing directors to be on both sides of contracts unless the conflicts are formally disclosed to, and approved by, the body of shareholders rather than the directors.Footnote 41 It is possible, however, that some relationships that look like conflicts of interest might actually benefit shareholders. A manufacturing company, for example, might want to put a prominent wholesaler on its board as a way of inducing the wholesaler to make selling its goods a priority and of ensuring that the company benefited from the wholesaler's knowledge of the market. Similarly, a railroad might want to have someone involved with steel-making on the board, as such a director would have technical and market expertise the railroad would otherwise have to pay for. In each case, the hypothetical director could use his position for self-dealing, but in each case, the firm could profit from the relationship implied by this director's involvement.

This same ambiguity affects all of the provisions we have discussed in this section. Modifications to Table A that shifted power from shareholders to directors may have facilitated the extraction of private benefits of control. But it is also possible that they placed managerial control squarely in the hands of those with the expertise and entrepreneurial vision needed to make the enterprise a success. The provisions that incorporators wrote into their articles of association were a matter of public record. If investors believed that particular provisions enabled directors to expropriate returns, we would expect them to have shied away from companies that had them. For the same reason, we would expect companies seeking to raise funds from outside investors to eschew them. In the next section we test this expectation formally.

Were Large Companies and Listed Companies Different?

Whether companies that aimed to raise funds from the wider public adopted articles that reassured potential investors was largely their own decision. Parliament, as we have seen, explicitly left this choice to incorporators, and neither the LSE nor the regional exchanges imposed much in the way of corporate governance rules.Footnote 42 When a company applied to be quoted on the LSE, the exchange's listing committee reviewed its articles of association. If the company was not approved for listing, its securities could still be traded on the exchange under a provision called “special settlement,” and many were.Footnote 43 Even so, the committee's criteria for approving a company's articles seem to have been quite minimal. Firms had to eschew purchasing their own shares with company funds, place limits on directors’ ability to borrow on behalf of the company without the approval of the general meeting, regulate the amount that directors could call in on shares not fully paid up, and prevent directors from restricting the transferability of shares that were fully paid in. The listing committee does not seem to have insisted on any provisions relating to voting rules or how often (or even whether) directors had to stand for election by shareholders.Footnote 44 Not until 1902 did the committee follow Table A's Article 82 and require companies to send out balance sheets annually to shareholders, and not until 1909 did it require companies to provide an earnings statement to the yearly meeting (Article 79). Nor did it require companies to adhere to Table A's rule about conflicts of interest (Article 57). Indeed, according to Brian Cheffins, before 1902 the committee did not even insist that directors disclose conflicts of interest to the other members of the board or refrain from voting on contracts in which they had a personal interest.Footnote 45 In this laissez-faire environment there was little more than self-interest to induce incorporators to adopt shareholder-friendly rules. Hence we would only expect to see them write articles that enabled shareholders to check and monitor directors if they thought that would enable them to raise larger amounts of capital at lower cost.

To explore the extent to which the capital markets disciplined incorporators in this way, we coded the clauses discussed in the previous section as dummy variables that took a value of 1 if a company modified Table A in ways that increased directors’ power relative to shareholders. We then analyzed the variation in the articles written by companies in our two 1892 samples to test whether large firms, or firms whose securities traded publicly, were less likely to modify Table A in ways that shifted power from shareholders to directors. Trading information comes from the reports in Burdett's for 1892. Size is nominal capital reported by the company at the time of filing.

Nominal capital is not, of course, the same thing as paid-in capital, for which we unfortunately do not have systematic information for the 1892 registrants. In the first place, a company might not succeed in selling all of the shares it had originally intended. Second, subscribers typically paid for only part of the par value of their shares at the time of purchase, contributing the rest in installments when called to do so by the directors. Nonetheless, we think nominal capital is a useful metric. By the late nineteenth century, its magnitude was a good indication of the incorporators’ ambitions at the time they drafted their articles of association and thus a good way to gauge the extent to which they planned to raise capital from the public.Footnote 46 Excessive optimism was costly because a company had to pay fees at the time of registration that were scaled by the magnitude of its nominal capital.Footnote 47 Moreover, because shareholders were liable for the full value of the shares, regardless of the amount they actually paid in, nominal value captures the magnitude of the obligation they assumed when they invested in the company.

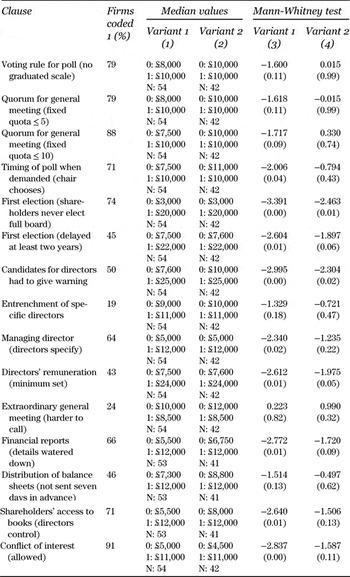

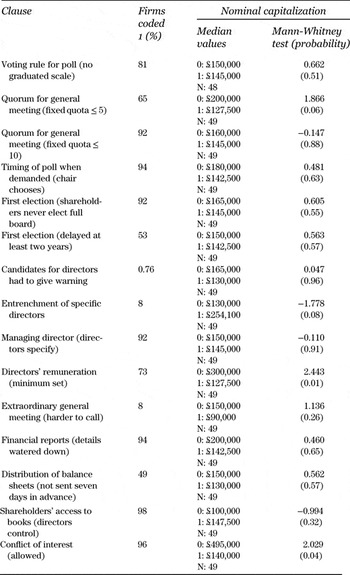

Table 5 reports the number and percentage of companies that modified various provisions of Table A so as to shift power toward directors. For each of the specified clauses there are two variants: one includes all the companies in the sample, and the other excludes the twelve whose files did not include articles of association. As already indicated, there is good reason to believe that most, if not all, of the companies without articles chose to be governed by Table A and hence that Variant 1 does a better job of capturing incorporators’ decisions. But it is also possible that the articles were simply missing. For the two variants of each clause, Table 5 displays the median nominal capital of companies coded 1 and 0 and the results of a Mann-Whitney test for whether companies coded 1 were significantly different from those coded 0. If companies coded 1 are larger than those coded 0, the test statistic will have a negative sign. The numbers in parentheses below the test statistic are the p-values for a two-tailed test of significance.Footnote 48

Table 5 Extent of Revisions to Table A that Shifted Power to Directors, by Nominal Capitalization of Company (1892 Registration Sample)

Source: See the Appendix for a description of the 1892 registration sample.

Notes: We coded the clauses listed in the first column as dummy variables that took a value of 1 if the company modified Table A in the way indicated. The percentage of firms coded 1 is relative to the N for Variant 2. For each clause we test two variants of the dummy variable. Variant 1 includes all of the fifty-four limited-liability firms in the sample. Variant 2 excludes the twelve companies whose files did not include articles of association. For the variables relating to financial accounts, the number of observations is smaller because we are missing the relevant page of the articles for one of our companies. In the columns marked (1) and (2), the figures 0:£X and 1:£X are the median values of nominal capital, rounded to the nearest £100, for companies coded 0 and 1, respectively, on the variable. N is the number of observations for the cell. Columns (3) and (4) report the Mann-Whitney test statistics and, in parentheses, the p-values for a two-tailed test. The value of the test statistic is negative if firms coded 0 on the variable have smaller capitalization values than firms coded 1.

For Variant 1, the differences between companies coded 1 and 0 are mostly statistically significant. This result is entirely expected, given that we know small firms were disproportionately likely to be missing articles of association. What is surprising, however, is that the signs are opposite from what one would expect if shareholder-friendly rules mattered for companies’ ability to raise capital.Footnote 49 The results for Variant 2 are similar in that the signs on the Mann-Whitney tests indicate large firms more commonly shifted power away from shareholders.Footnote 50 Many of the coefficients are not statistically significant, suggesting that the choices made by large firms were not appreciably different from those of small firms and that neither adopted shareholder-friendly rules. However, large firms were significantly more likely than small firms to delay the first election of directors, to allow shareholders to elect only a proportion of the board at that first election, and to require outsiders seeking a seat on the board to announce their candidacy in advance. Large firms were also more likely to water down the financial statements provided annually to shareholders and to prescribe at least some minimum compensation for the directors rather than leave it entirely to the shareholders.Footnote 51

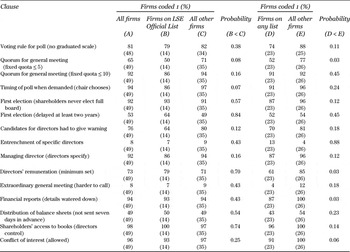

We have already seen that the companies in the Burdett's sample were generally more likely to shift power from shareholders to directors than the companies in the 1892 registration sample (Table 4). The enterprises in the Burdett's sample ranged considerably in size, from £15,000 in nominal capital at the small end of the spectrum to £1,000,000 at the other extreme (Table 2), but size seems not to have had much effect on the kinds of articles that the companies wrote. As Table 6 indicates, the Mann-Whitney test statistics are more likely to be positive for the Burdett's sample than for the 1892 registration sample, but they are rarely statistically significant. Moreover, most cases where the tests are significant are not economically meaningful. Fewer large firms set quorums for general meetings of less than five members, but almost all of them specified less than ten—still a very small number for a big, publicly traded company. Similarly, large firms were statistically less likely to reject Table A's strict conflict-of-interest provision, but only two of the companies in the Burdett's sample actually accepted it. Large firms were somewhat more likely than small ones to leave directors’ remuneration to the shareholders, but fully three-quarters of the companies in the Burdett's sample embedded a compensation rule in their articles. Almost all had a provision allowing the board to pay managing directors salaries, commissions, and/or a share of profits off the top.

Table 6 Extent of Revisions to Table A that Shifted Power to Directors, by Nominal Capitalization of Company (1892 Burdett's Sample)

Source: See the Appendix for a description of the 1892 Burdett's sample.

Notes: We coded the clauses listed in the first column as dummy variables that took a value of 1 if the company modified Table A in the way indicated. There are forty-nine companies in the Burdett's sample, but the observation for the first variable is missing for one company. In the column headed “Median values,” the figures 0:£X and 1:£X are the median values of nominal capital, rounded to the nearest £100, for companies coded 0 and 1, respectively, on the variable. N is the number of observations for the cell. The next column reports the Mann-Whitney test statistic and, in parentheses, the p-values for a two-tailed test. The value of the test statistic is negative if firms coded 0 on the variable have smaller capitalization values than firms coded 1.

Only fourteen of the forty-nine companies in the Burdett's sample had a security officially listed on the LSE, and only twenty-three had a security listed on any British exchange. Table 7 reports the proportion of companies in these categories that altered Table A's clauses to shift power to directors and compares these proportions with those of all other companies in the sample. As a general rule, companies with at least one listed security were less likely to adopt these changes, but the differences do not offer much comfort to those who believe that companies seeking to raise capital on the country's most liquid markets would adopt more shareholder-friendly governance rules. Firms with a security on the LSE official list were significantly less likely to allow their chairman to delay the taking of a poll, but 86 percent of firms in this category still adopted this revision. Firms with securities listed on an exchange were significantly less likely to water down their financial reports, to reject Table A's strict rule on conflicts of interest, and to specify a minimum compensation for directors, but most of them nonetheless adopted these changes (the proportions of companies adopting each of these modifications were 87 percent, 91 percent, and 61 percent respectively). No other difference is statistically significant.Footnote 52

Table 7 Extent of Revisions to Table A that Shifted Power to Directors, by Whether Company Was Listed on an Exchange (1892 Burdett's Sample)

Source: See the Appendix for a description of the 1892 Burdett's sample.

Notes: We coded the clauses listed in the first column as dummy variables that took a value of 1 if the company modified Table A in the way indicated. The other columns report the proportion of companies for which the specified article was coded 1 for all companies (A), for companies that had at least one security on the LSE Official List (B) versus all other companies (C), and for companies with at least one security listed on any British exchange (D) versus all other companies (E). The numbers in parentheses are the number of companies in each cell. For each comparison, B versus C and D versus E, we provide the p-values for a one-tailed test of the hypothesis that firms with listed securities were less likely to modify Table A in a way that shifted power toward directors.

In sum, neither large firms, firms covered in Burdett's, firms with securities listed on an exchange, nor even firms with a security on the LSE official list bucked the trend to write articles that gave directors largely unchecked powers. If incorporators were worried that embedding such rules into their articles would raise their cost of capital, one might expect them to break ranks and compete for funds by offering more shareholder-friendly governance. But we do not observe anything of the kind.

Contemporary Views of Companies’ Governance Practices

Contemporary financial writers warned shareholders that poor corporate governance practices could cost them money. The Investor's and Shareholder's Guide, for example, admonished investors to read a company's articles of association carefully because “in them often lurk most mischievous provisions.”Footnote 53 Those who did not heed this advice might later discover that the articles had “been so devised as to deprive them of their just rights” by “unrestrictedly vesting in the directors all the powers of the company.” They might also learn that the articles conferred upon the directors “the right to excessive remuneration,” or that the directors retained their positions “for a long term of years, or even ‘irremovably,’ at high salaries.” Moreover, even when directors were technically removable, shareholders might find that the privilege of voting by proxy gave members of the board a powerful “weapon” they could use “to shield mal-administration, to balk inquiry, to thwart reform.”Footnote 54

Periodicals such as the Economist and the Financial Times underscored the urgency of these warnings.Footnote 55 Readers would have come across report after report of directors using their control of the voting process to outmaneuver discontented investors. For instance, the chairman of the South American and Mexican Company blocked shareholders’ efforts to prevent a vote on a controversial proposal by declaring their motion to adjourn defeated “on a show of hands, without the slightest pretence of a count.” He then “with lightning speed put the substantive motion” to a vote, “declaring it carried by the same instantaneous method,” and adjourned the meeting before the opposition had time to demand a poll.Footnote 56 When shareholders of the Lancashire and Yorkshire Water Gas Company rejected by a show of hands the directors’ annual report and called for a committee of investigation, the directors demanded a poll and controlled enough proxies to defeat the resolution.Footnote 57 Essentially the same thing happened at the annual meeting of the Maxim-Nordenfelt Guns and Ammunition Company.Footnote 58 At the meeting of the Industrial and General Trust Company, the chairman kept a slate of unpopular directors in power by accepting calls for polls whenever one of them was defeated in a show of hands.Footnote 59

Readers would also have encountered numerous accounts of directors taking advantage of weak governance rules to enrich themselves at shareholders’ expense. The Economist republished an item from a Johannesburg newspaper reporting that several “life governors” of De Beers had obtained more than £66,000 from the company in exchange for a set of worthless securities, which they then lumped with other items on the company's balance sheet to obscure the transaction.Footnote 60 Directors of companies ranging from the famous to the obscure—from the Nobel Dynamite Trust to the United Horse Shoe and Nail Company to the Voigt Brewery—stood accused of pocketing excessive salaries and fees and profiting from contracts in which they had a conflict of interest.Footnote 61 As a shareholder in the Shenango Railway and Mercer Coal Company complained bitterly, “Everybody concerned gets something except the shareholders. And so it will go on, I doubt not, until the shareholders make themselves masters of their own business, and insist upon a radical reform.”Footnote 62

A search for news stories about the companies in our Burdett's sample suggests, however, that these lurid accounts were by no means representative of the experience of shareholders more generally. Plenty of articles in the Economist and the Financial Times covered the companies’ foundings as well as their subsequent general meetings and important transactions. Most were straightforward accounts that contained little in the way of drama, and shareholders displayed scarcely any interest in corporate governance, let alone in making themselves “masters.”Footnote 63 To the contrary, they seem to have willingly granted directors control in exchange for the promise of returns greater than could be obtained elsewhere. Although the terms of this bargain were rarely spelled out explicitly, their traces can be seen in the efforts made by directors to keep dividends high and steady.Footnote 64 They can also be seen in the rituals associated with the annual general meeting, in particular the practice of accompanying motions to accept the annual report with resolutions of thanks to the directors for their hard work on behalf of the company.Footnote 65 In good years these votes might be accompanied by approving speeches and applause. At the 1891 annual meeting of Mason and Mason, for example, shareholders learned they would receive a dividend of 18 percent, and the presentation of the annual report was punctuated by rounds of applause, cries of “Hear, hear,” and even laughter.Footnote 66

Shareholders had voice, and when earnings were unexpectedly low, they might complain vociferously about the misguided business strategies or poor management practices they thought were responsible.Footnote 67 But they could also be patient when circumstances warranted. In some cases, companies developing innovative new technologies were not expected to earn profits for some time, and shareholders showed a willingness to wait and even, as in the case of the Linotype Company, to increase the company's capital. Linotype's chairman concluded his speech in support of a new issue of preference shares with this assertion: “I do not think anyone ought ever to go into a company of this character which is introducing an invention altogether new who expect returns immediately and of a considerable amount. But those who wait, I think, would get large returns.” He then moved the resolution “amidst applause.”Footnote 68

Shareholders could also be supportive when they thought a fall in earnings was the result of general macroeconomic conditions or a consequence of necessary write-offs of capital or of costly new investments.Footnote 69 In 1895, annual dividends fell from 14 to 9 percent at Charles Baker and Company, as a result of poor business conditions and the closing of a store, but shareholders applauded a resolution thanking the board and singled out the managing directors in particular “for the very satisfactory balance-sheet which had been produced that day.”Footnote 70 Earnings bounced back by the next year, and shareholders continued to applaud the company's management.Footnote 71 Comebacks were particularly appreciated. Shareholders of the National Explosives Company had attributed their low earnings to the poor management practices of the directors.Footnote 72 After a reorganization in 1893, the company gradually returned to profitability, and five years later a large shareholder took the floor to declare his “pleasure in seconding the resolution” to approve the directors’ report. His assertion that the company had a “brilliant” future was greeted with applause, and the resolution passed unanimously, as did a motion to reelect the two retiring directors.Footnote 73

When earnings were low, directors sometimes explicitly acknowledged that they had not lived up to their implicit bargain with shareholders by making appropriately sacrificial gestures. For example, shareholders were furious when the directors of Joseph Robinson and Company, sank money into an alabaster mine that did not initially pay off. After one investor proposed a resolution of censure, the directors promised not to take their fees until the company was able to declare a dividend of at least 5 percent, and the controversy seems to have faded when the mine began to produce.Footnote 74 Similarly, directors of the Fowler-Waring Cables Company, attempted to head off shareholders’ ire when the company did not earn enough in its first year of operation to pay dividends; they announced that “as we have not made any profits we have taken no fees ourselves.” The news was greeted with cries of “Hear, hear,” and although shareholders expressed their unhappiness by questioning the amount paid to auditors, the meeting concluded with a unanimous vote of thanks to the board. The next year, the company was still not profitable, and the directors again refused their fees.Footnote 75

Trends in Law and Practice in the Early Twentieth Century

When shareholders complained about their companies, they typically focused their anger on particular people and actions, not on the governance structures that facilitated bad behavior. Criticisms of the concentration of power in directors’ hands were rare, and indeed there seems to have been little interest in reforming corporate governance rules. A Parliamentary committee, formed in the wake of a series of business scandals in the early 1890s, solicited comments from businesspeople about how better to prevent “fraud in relation to the formation and management of Companies.”Footnote 76 The responses focused much more on the problem of fraudulent promotions than on internal governance. Although the committee recommended that Table A be amended to “conform more closely to modern practice and business requirements,” it did not specify how the articles should be revised, and neither the Board of Trade nor Parliament took any action.Footnote 77 Parliament did, however, take action on the committee's recommendations to prevent fraudulent promotions. The resulting Companies Act of 1900 required companies issuing shares to the public to publish detailed information about their sources of capital and the allocation of shares and debentures, restricted their ability to sell shares for anything but cash, and required them to register mortgages and other charges on assets for the protection of creditors. It also made directors and officers criminally liable for any false statements on these documents. However, aside from regulating procedures for calling extraordinary meetings and requiring auditors to examine balance sheets and report annually to shareholders at the general meeting, the 1900 statute contained no provisions relating to corporations’ internal affairs.Footnote 78

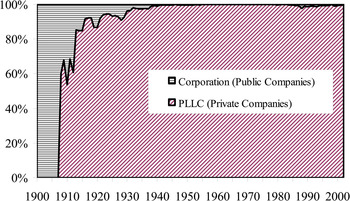

Because the law raised the cost of organizing all types of corporations, whether or not they issued securities to the public, it led to a sharp drop in the number of new companies (from 5,082 in 1897 to 4,849 in 1900 to 3,343 in 1901 to 3,725 in 1904) and a flood of complaints.Footnote 79 Parliament responded in 1905 by appointing the Warmington Committee to recommend further changes in the law.Footnote 80 The result was a new statute in 1907 that gave incorporators the choice of organizing their companies as either public or private enterprises. In essence, the law offered businesspeople a tradeoff: if they organized their corporations as public companies they had to conform to the requirements of the 1900 Act, but they could escape the act's strictures (except for the obligation to submit an audited balance sheet each year to the general meeting) by organizing instead as private companies. To signal this choice they had to include in their articles of association clauses that (1) prohibited their company from making public offerings of shares or debentures, (2) limited the number of shareholders in the company to fifty (not including employees), and (3) restricted the transferability of shares in some way.Footnote 81 Businesspeople overwhelmingly voted with their feet for the new form. Fully 16,172 existing companies converted to private companies in 1908, 19,329 in 1909, and an average of 15,100 a year from 1910 to 1919 and 12,000 a year from 1920 to 1929.Footnote 82 As Figure 1 shows, incorporators of new firms disproportionately chose to organize as private companies such that by the early 1920s, more than 90 percent of all new companies were private.Footnote 83 Enterprises that opted to be private could still raise capital externally, but they had to place their securities through intermediaries. Many incorporators signaled their intention to raise funds in this way by including a provision in their articles of association enabling them to “pay a commission to any person for subscribing or agreeing to subscribe . . . for any shares in the Company or procuring or agreeing to procure subscriptions.”Footnote 84

Figure 1. Ratio of new private companies to all new limited companies in Britain, 1900–2000. (Sources: U.K. Board of Trade, General Annual Report [London, 1900–1921] and Report [London, 1922–2000]).

At the same time that Parliament offered companies the choice of being private or public, it provided them with a new default set of articles of association. The 1862 Companies Act had given the Board of Trade the authority to revise the model table as needed, with the revisions acquiring the force of law upon publication in the London Gazette.Footnote 85 Decades elapsed, however, and the board took no action until finally, in 1906, the Warmington Committee undertook a revision. The committee considered, and rejected, two alternatives to updating Table A. One was to give up altogether on the idea of a set of model articles of association and simply leave it to each company to draft its own rules. The committee recognized, however, there were “a considerable number of small companies . . . which adopt Table A with a few small variations, simply in order to save expense in printing” and thought it important to keep the setup costs low for these entities. The committee also considered whether to seek an act of Parliament to impose uniform regulations on all companies, but decided that such legislation would “be wholly inconsistent with the use now made of the freedom which companies enjoy” to draft their own articles and that there were important reasons to allow companies of different sizes and types to draft articles suited to their specific business needs.Footnote 86

Instead, the committee commissioned barristers R. J. Parker and A. C. Clauson to draw up a new model table. It then circulated the draft for comments and discussed it at a subcommittee meeting that included Sirs Francis Beaufort Palmer and Francis Gore-Browne, both prominent barristers who had published handbooks for incorporators.Footnote 87 After a few small and mostly technical changes to the draft, the Warmington Committee appended the new Table A to its report of June 18, 1906.Footnote 88 The Board of Trade published it in the London Gazette on July 31, 1906, as required by law, and the revised version came into force on October 1, 1906.Footnote 89 With the exception of a last article concerning notifications by post, the new Table A was appended verbatim to the Companies Act in 1908.Footnote 90

Some of the changes the committee made to Table A were responses to shifts in business practice. For example, the model included several new clauses in recognition of the increasingly common practice of issuing multiple classes of shares with different income and/or voting rights (Articles 3 and 4). Other revisions aimed to ensure that the articles of a company accepting the model table would automatically comply with the LSE's listing requirements. Consequently, there was now a clause in Table A forbidding directors to use a company's funds to purchase its own shares (Article 8) as well as one limiting the extent to which directors could borrow on behalf of the company without the approval of the general meeting (Article 73).

What is most striking about the revised Table A, however, is the extent to which it embraced the provisions enhancing directors’ power that so many companies in our 1892 samples had written into their articles. For example, the 1862 model table had specified a quorum for general meetings that increased with the number of shareholders, starting with a minimum of five. Most of the 1892 firms had lowered this requirement, and the 1908 model table followed suit, reducing the quorum to just three members personally present (Article 51). Similarly, in the event that the chairman or the requisite number of shareholders demanded a poll, the 1862 model table did not specify when the vote would be taken, but the implication was that it would be held immediately. Most of our 1892 firms wrote articles allowing the chairman to delay the vote, and the 1908 model table copied this change (Article 59). The new Table A also followed practice by shifting the default voting rule to one vote per share (Article 60). As noted above, there was no provision in the 1862 model for a managing director. The 1908 table not only added such a clause but also explicitly exempted managing directors from having to stand for reelection during their terms of service, which were set by the directors themselves (Article 72). The 1908 table revised the default rules to enable directors to restrict shareholders’ access to the company's books (Article 105). It also watered down the financial information that directors were required to provide shareholders at the annual meeting, no longer specifying the content of the financial statement and balance sheet, and allowed these documents to be made up as much as six months in advance of the meeting, rather than the three months mandated by the 1862 version (Articles 106 and 107).

In a few cases, however, the drafters of the new model articles sought to improve corporate governance practices by maintaining some of the 1862 rules that large numbers of companies had discarded. Thus, the drafters did not alter Table A's strict conflict-of-interest rule (Article 77), nor did they revise the expectation that shareholders should have the opportunity to elect a full board of directors at the first annual meeting of the company (Article 78). The drafters also occasionally qualified some of their changes so as to moderate the resulting shift in power toward directors. Most notably, the 1908 model included a sentence, not found in any of our 1892 articles, enabling the company in a general meeting to terminate the appointment of a managing director (Article 72).

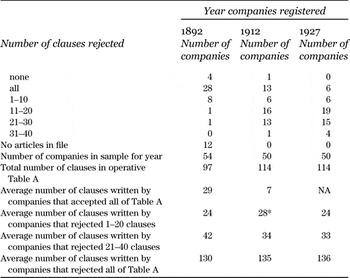

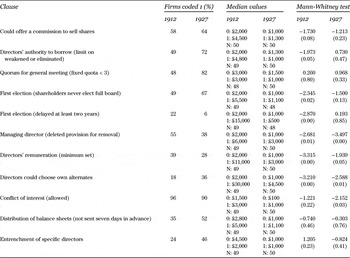

As we have seen, one of the motives of the Warmington Committee in seeking to bring Table A more in line with current practice was to keep the costs of organizing small companies low by giving incorporators a model set of articles they could adopt off the shelf. In this goal the board seems to have been only partially successful (see Table 8). Although the companies in our 1912 and 1927 samples were smaller on average than those in the 1892 registration sample, none simply adopted Table A as written. At the same time, many fewer companies—only 26 percent in 1912 and 12 percent in 1927, compared with 53 percent of the 1892 registration sample—rejected Table A in its entirety. Most companies seem to have chosen an intermediate path, rejecting some clauses, substituting alternatives in their stead, and adding extra clauses of their own devising. In 1912, companies that rejected at least one but not all clauses in Table A on average rejected nineteen clauses and wrote thirty substitute or new provisions. The equivalent companies in 1927 on average rejected nineteen clauses and wrote twenty-eight provisions of their own.

Table 8 Summary of Modifications Made to Table A by Companies in Registration Samples

Source: See the Appendix for descriptions of the samples.

Notes: The list of 1892 companies rejecting Table A includes two firms whose articles did not specifically reject (or accept) the entire table but wrote at least one hundred clauses.

* based on only forty-nine companies because we are missing the last page(s) of the articles for one company and so can see only sixteen of its clauses.

Many of the changes that companies made to the model table continued the shift in the balance of power toward directors that we observed in 1892 (see Table 9). Of course, incorporators no longer had to revise Table A in order to institute a low quorum, though 48 percent of the 1912 companies and 82 percent of the 1927 companies set the quorum even below Table A's minimal level of three shareholders personally present. Table A now diluted the financial information that directors were required to provide annually to the general meeting, but 35 percent of the 1912 companies and 52 percent of those in 1927 still rejected the provision that balance sheets be distributed at least seven days in advance. Almost all companies rejected Table A's prohibition of conflicts of interest (96 percent in 1912 and 90 percent in 1927). Moreover, incorporators continued to go beyond Table A in protecting directors from having to face reelection by shareholders. Many companies (49 percent in 1912 and 67 percent in 1927) denied shareholders the opportunity ever to elect a full board of directors, though it was now less common for firms to delay the first election for two or more years (only 22 percent of the companies did this in 1922 and 6 percent in 1927). Table A permitted directors to exempt one or more of their number from the regular election rotation by naming them managing directors, but 55 percent of the 1912 companies and 38 percent of the 1927 companies went further and deleted Table A's provision giving the general meeting the authority to terminate the appointment of managing directors. Now, moreover, companies began to add a new clause to their articles, not in Table A, allowing directors to choose their own alternates when they were out of the country or could not otherwise attend board meetings for an extended period of time (18 percent of companies included this provision in 1912 and 36 percent in 1927). More strikingly, the number of cases of outright entrenchment of directors increased sharply. By 1927 the proportion of companies naming one or more directors for life had increased to 46 percent.Footnote 91

Table 9 Extent of Revisions to Table A that Shifted Power to Directors, by Nominal Capitalization of Company (1912 and 1927 Registration Samples)

Source: See the Appendix for a description of the 1912 and 1927 registration samples.

Notes: We coded the clauses listed in the first column as dummy variables that took a value of 1 if the company modified Table A in the way indicated. There are fifty companies in the 1912 sample, but for one firm there was no quorum rule in the articles and we are missing the last page of the articles for another company and so can see only sixteen of its clauses. There are also fifty companies in the 1927 sample, but two companies failed to include provisions for the timing of the first election and the start of the rotation, though they opted out of the relevant Table A provisions. In the column headed “Median values,” the figures 0:£X and 1:£X are the median values of nominal capital, rounded to the nearest £100, for companies coded 0 and 1, respectively, on the variable. N is the number of observations for the cell. The next two columns report Mann-Whitney test statistics and, in parentheses, the p-values for a two-tailed test. The value of the test statistic is negative if firms coded 0 on the variable have smaller capitalization values than firms coded 1.

As was the case for the 1892 sample, larger firms were not more likely than small to adopt shareholder-friendly corporate governance rules in either 1912 or 1927. To the contrary, in Table 9 the signs on the Mann-Whitney test are mainly negative (and statistically significant), indicating that it was large firms that most often wrote rules shifting power to directors. In the few cases where the signs were positive, the tests were not significant. Nor is there any evidence that companies that chose to be public aimed to reassure investors by giving shareholders more power to check or monitor investors. Only eight of the companies in the 1912 registration sample and only three in the 1927 registration sample chose to be public companies, so it is difficult to generalize.Footnote 92 Public companies were less likely to entrench directors for life than private companies, but in most other respects they were as likely or more likely to revise Table A in ways that enhanced directors’ power relative to shareholders.Footnote 93

Conclusion

British company law granted incorporators a great deal of freedom to write governance rules for the enterprises they founded. Although Parliament provided companies with a model set of articles of association that they could adopt off the shelf, its provisions were merely default rules that prevailed only if a firm did not write its own articles. Most companies in fact rejected the model articles, either as a whole or in part. To study the kinds of governance rules that incorporators chose to write instead, we collected the articles of three samples of companies drawn from the Board of Trade's registration lists and a fourth sample (from Burdett's) of registered companies whose securities traded on the exchanges. We analyzed the alternative provisions that the companies drafted—how they deviated from those of the model articles and how they interacted with each other to shape the way corporate governance worked on the ground. We found that the vast majority of companies wrote articles whose provisions collectively shifted power from shareholders to directors. Shareholders in companies formed under British general incorporation law—whether large or small, public or private—had little ability even to monitor, let alone influence, what directors were doing with their investments.

A few contemporary observers expressed concern about the extent of directors’ control, but shareholders themselves seem largely to have been unfazed. For the most part, complaints about bad corporate behavior focused on the misleading or sometimes fraudulent statements of promoters of new issues, not on the governance practices of existing companies. Parliament responded to this pattern of grievances by enacting reforms in 1900 that tightened oversight of public offerings, but it took no action to mandate better rules. To the contrary, when in 1906 a Parliamentary committee finally rewrote the model articles of association embedded in the 1862 statute, it largely ratified contemporary practices that shifted power toward directors. Now that the model table more closely reflected what companies were actually doing, fewer companies rejected it in its entirety, but they continued to rewrite key sections in ways that further enhanced directors’ autonomy.

Companies could, of course, have bucked this trend and revised Table A in ways that increased shareholders’ ability to monitor and check directors. One might expect them to have done so if they could thereby have lowered their cost of capital, but we found no evidence of such a strategy either among our sample firms or in the financial press. To the contrary, the idea that companies should be run in the interests of their shareholders seems not yet to have been in people's minds. If one reads history forward rather than backward, if one tries to understand what people at the time thought they were doing rather than interpreting their behavior in twenty-first-century terms, then it seems that shareholders in the late nineteenth and early twentieth century did not expect to exercise much more than voice. When they bought shares in a corporation, they were gaining the chance to earn returns that were much higher than those available from government bonds and the like.Footnote 94 Returns were potentially higher because the investments were riskier. But they were also higher because of the knowledge and skills of the entrepreneurs running the companies, and shareholders seem to have been content to leave those men in charge. Of course, entrepreneurs sometimes failed to live up to the terms of this implicit bargain. When shareholders suspected that low dividends were a result of bad faith, they could become very vocal in their discontent and move beyond voice to action, organizing to overthrow management or take the perpetrators to court. These kinds of incidents take up many pages in the financial press of the period. But they seem to have been exceptional. If one starts, as we do, with a sample of companies and then searches for reports on them in the press, what stands out is the absence of conflict. The bargain seems to have been upheld to the satisfaction of the parties involved.

Nonetheless, there remains the counterfactual question of whether investment would have been higher if governance rules had been friendlier to shareholders. A number of years ago William Kennedy opened up a new front in the scholarly war over the sources of British economic decline by arguing that poor corporate governance practices encouraged investors to put their money overseas rather than in the new technology sectors of the domestic economy.Footnote 95 Michael Edelstein quickly challenged this view by demonstrating the responsiveness of capital flows to relative rates of return.Footnote 96 More recently, Benjamin Chabot and Christopher Kurz have shown that foreign and domestic returns were uncorrelated and investors seeking diversified portfolios behaved rationally when they moved substantial amounts of capital overseas.Footnote 97 An important limitation of this work, however, is that it is based on data collected from the public securities markets. As we have shown, the overwhelming majority of new companies seeking external capital in the early twentieth century chose to raise funds by private placement rather than on an exchange. Therefore, if scholars are truly to answer the counterfactual question, they must find ways of studying these private investment channels and assessing their magnitude.