Introduction

Management control systems (MCSs) have been conceptualised in the literature in various ways. While some studies define MCSs in respect to goal congruence and objective accomplishment (Anthony, Reference Anthony1965; Otley & Berry, Reference Otley and Berry1994), other studies define MCSs based on the assumption that superiors are seeking to control subordinates’ behaviour (Euske & Riccaboni, Reference Euske and Riccaboni1999; Horngren, Bhimani, Datar, & Foster, Reference Horngren, Bhimani, Datar and Foster2002; Merchant & Van der Stede, 2007; Malmi & Brown, Reference Malmi and Brown2008). Based on this assumption, this study aims to contribute to the MCS literature in two ways. First, the study uses Snell's (Reference Snell1992) three component model to focus on the use of different types of controls within organisations. Snell's (Reference Snell1992) model focuses on the extent to which organisations are using input, behaviour and output controls. While many studies have developed various control typologies to examine the use of different types of controls within organisations, Snell's (Reference Snell1992) model is chosen as it focuses on both ability and motivation, provides a full range of control, and has been used in the management accounting literature (Snell & Youndt, Reference Snell and Youndt1995; Cardinal, Reference Cardinal2001; Cardinal, Sitkin, & Long, Reference Cardinal, Sitkin and Long2004; Abernethy, Schulz, & Bell, Reference Abernethy, Schulz and Bell2007; Johnson, Reference Johnson2011).

Second, the study aims to provide an improved insight into the use of controls by examining the role of input, behaviour and output controls within different organisational life cycle (OLC) stages. Miller and Friesen (Reference Miller and Friesen1984) classify organisations into five OLC stages (birth, growth, maturity, revival and decline stages) based on the alignment of an organisation's four contingent variables (organisational situation, strategy, structure and decision-making style) simultaneously (Miller & Friesen, Reference Miller and Friesen1984). The approach of examining how multiple contingency factors combine to affect the use of controls is referred to as the configuration form of contingency fit with both Henri (Reference Henri2009) and Gerdin (Reference Gerdin2005) arguing that there is a gap in the literature investigating the simultaneous influence of multiple contingent variables on MCS attributes. It is argued that such an approach more accurately reflects the interaction between an organisation's environment and its MCS (Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005). This approach ‘does not explicitly include contextual variables (such as environment and size) as they are embedded in organizational life cycle stages’ (Moores & Yuen, 2001: 355).

While OLC stages have been widely examined both conceptually and empirically in the organisational behaviour literature, only a limited number of studies have examined the association between MCSs and OLC stages (Moores & Yuen, 2001; Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005; Davila, Reference Davila2005; Kallunki & Silvola, Reference Kallunki and Silvola2008; Silvola, Reference Silvola2008). Of these, Auzair and Langfield-Smith (Reference Auzair and Langfield-Smith2005) only investigated two stages of Miller and Friesen's (Reference Miller and Friesen1984) five-stage OLC model, while Davila (Reference Davila2005) only examined firms in transition from the birth to growth stage. Other studies have examined more than two OLC stages, however these studies have focused on different MCS attributes. For instance, Silvola (Reference Silvola2008) found that the use of budgeting, earnings management and the control of profit centers differed across OLC stages, and Kallunki and Silvola (Reference Kallunki and Silvola2008) indicated that the use of activity-based costing varied across OLC stages. In addition, Moores and Yuen (2001) examined the association between OLC stages and the formality of management accounting systems (MASs), with significant results identified. Rather than focusing on a generic aspect of MASs, namely the formality of MASs, the current study aims to extend this literature by examining the association between OLC stages and three specific formal controls, Snell's (Reference Snell1992) input, behaviour and output controls. Specifically, the study aims to provide a more comprehensive analysis of the association between Snell's (Reference Snell1992) three types of controls and OLC stages by focusing on four stages (birth, growth, maturity and revival stages) of Miller and Friesen's (Reference Miller and Friesen1984) OLC modelFootnote 1. In particular, the study will examine the extent to which organisations use input, behaviour and output controls both within and across OLC stages.

The remainder of this paper is structured as follows. The next section presents a review of the literature on OLC stages and the types of controls, and develops the relevant hypotheses. The Method section discusses the method used to collect data and the measurement of the independent and dependent variables. The results of the data analysis and a discussion of the results are provided in the Results section. The final section provides a discussion of the contributions, practical implications, limitations of the study and insights for future research.

Literature review and research hypotheses

OLC stages

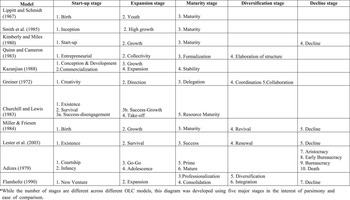

Previous studies have proposed that changes in organisations follow a consistent and predictable pattern which can be characterised by stages of growth (Greiner, Reference Greiner1972; Adizes, Reference Adizes1979; Miller & Friesen, Reference Miller and Friesen1984; Smith, Mitchell, & Summer, Reference Smith, Mitchell and Summer1985; Dodge & Robbins, Reference Dodge and Robbins1992; Quinn & Cameron, 1983). Hanks, Watson, Jansen, and Chandler (Reference Hanks, Watson, Jansen and Chandler1993) suggested that each stage of growth consists of a unique configuration of variables related to organisational context and structure. The concept of an OLC is therefore introduced to reflect the various stages of the development of organisations. Numerous OLC stage models have been developed with the number of stages varying from three to 10 (see Figure 1).

Figure 1 A summary of organisational life cycle (OLC) stage models*

While there are a number of different OLC models developed, Moores and Yuen (2001) argued that an acceptable OLC stage model must meet two criteria. First, a complete biological cycle of organisational development from birth to death should be covered in the model. Second, the model should have been examined empirically. In addition, for the purpose of this study, the model selected should have also provided a well-established measure of the OLC stages developed due to the use of a survey method in the study.

Among the OLC models discussed, models which cover a complete OLC biological series from birth to death are limited to Adizes (Reference Adizes1979), Kimberly and Miles (Reference Kimberly and Miles1980), Miller and Friesen (Reference Miller and Friesen1984), Flamholtz (Reference Flamholtz1990) and Lester, Parnell, and Carraher (Reference Lester, Parnell and Carraher2003). However, Adizes (Reference Adizes1979), Kimberly and Miles (Reference Kimberly and Miles1980) and Flamholtz (Reference Flamholtz1990) did not provide well-established measures of the OLC stages developed, and are therefore considered inappropriate for this study. In addition, while Lester, Parnell, and Carraher (Reference Lester, Parnell and Carraher2003) provided a comprehensive measure of the OLC stages developed, the validity and reliability of this model has not been widely tested. Accordingly, Miller and Friesen's (Reference Miller and Friesen1984) OLC model is considered the most appropriate model and is adopted in this study. The model has been empirically supported and has been widely used in recent management accounting studies (Moores & Yuen, 2001; Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005; Davila, Reference Davila2005; Kober, Reference Kober, Ng and Paul2010; Kallunki & Silvola, Reference Kallunki and Silvola2008; Silvola, Reference Silvola2008).

Miller and Friesen's (Reference Miller and Friesen1984) five-stage model describes each stage based on its organisational situation, strategy, structure and decision-making style as follows. Birth-stage firms are small and owner controlled, with a homogeneous environment. In order to avoid confronting competitors directly, birth-stage firms have a narrow product scope, and focus on the pursuit of a niche strategy (Quinn & Cameron, Reference Quinn and Cameron1983; Flamholtz, Reference Flamholtz1990). Organisational structures are simple and centralised with little delegation given to subordinates (Kazanjian, Reference Kazanjian1988; Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003). An intuition-orientated decision-making style prevails and only a limited number of factors and opinions are taken into consideration in making decisions (Kallunki & Silvola, Reference Kallunki and Silvola2008). Different decisions therefore may be in conflict with each other.

In the growth stage, organisational size increases and ownership becomes dispersed (Kimberly & Miles, Reference Kimberly and Miles1980; Churchill & Lewis, Reference Churchill and Lewis1983; Flamholtz, Reference Flamholtz1990). The organisational environment is more dynamic and competitive than in the birth stage. The niche strategy is abandoned as emphasis moves to growth and early diversification. Efforts are also devoted to innovation (Quinn & Cameron, Reference Quinn and Cameron1983) which results in a wider range of products. Organisational structure becomes more complex and less centralised with the adoption of functionally based structures (Greiner, Reference Greiner1972), which facilitates delegation. The movement towards a team-based approach to work design allows more subordinates to be involved in decision making, while the decision-making process itself becomes more analytical and better integrated.

Maturity-stage firms are larger in terms of size, and characterised by a more dispersed ownership than growth-stage firms with a relatively stable organisational environment. An emphasis on a defender strategy shifts organisations’ attention from product innovation and diversification to efficiency and profitability (Adizes, Reference Adizes1979; Quinn & Cameron, Reference Quinn and Cameron1983; Kazanjian, Reference Kazanjian1988) and hence the product scope is narrower than in the growth stage. Organisational structures are centralised with less delegation of power than in the growth stage ( Kimberly & Miles, Reference Kimberly and Miles1980; Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003). The decision-making style is less proactive and less innovative than in any other stage and hence decisions become less responsive and less adaptive to external environmental conditions (Greiner, Reference Greiner1972).

Revival-stage firms are the largest, and ownership becomes even more dispersed than in the maturity stage, thereby minimising the influence of the board, owners and shareholders on business operations and decisions. The organisational environment is much more heterogeneous, dynamic and hostile than in the other stages, and there is a broader range of products than in the maturity stage. Major innovations and extensive diversification play a crucial role in the achievement of a differentiation strategy (Quinn & Cameron, Reference Quinn and Cameron1983; Flamholtz, Reference Flamholtz1990; Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003). Divisional structures are adopted with divisional heads responsible for their own divisions’ performance (Flamholtz, Reference Flamholtz1990). While a high level of risk taking is involved in decision making, the use of an analytical and participative decision-making style (Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003) lessens the boldness involved in the decision-making process.

Finally, in the decline stage ownership is tightly held with the board, owners and shareholders having a significant influence on decision making. Firms strive to survive without a particular organisational strategy. The organisational structure is highly centralised with little communication between managers and subordinates (Adizes, Reference Adizes1979; Kimberly & Miles, Reference Kimberly and Miles1980). Few factors are taken into consideration when making decisions and no real effort is made to ensure the integration of different decisions (Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003).

Types of controls

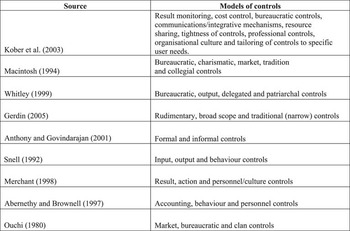

Figure 2 provides a summary of the different models used to describe the types of controls. For instance, Kober, Ng, and Paul (Reference Kober, Ng and Paul2003) developed the most complex model, including nine types of controls. Alternatively, Macintosh (Reference Macintosh1994) categorised controls into five types while Whitley (Reference Whitley1999) suggested a four-category model. Snell (Reference Snell1992) developed a three-component model (input, behaviour and output controls), which is similar to other three-component models developed by Merchant (Reference Merchant1998) (result, action and personnel/culture controls), Abernethy and Brownell (Reference Abernethy and Brownell1997) (accounting, behaviour and personnel controls) and Ouchi (Reference Ouchi1980) (market, bureaucratic and clan controls)Footnote 2. Gerdin (Reference Gerdin2005) developed a different three-component model (rudimentary, broad scope and traditional controls), while Anthony and Govindarajan (Reference Anthony and Govindarajan2001) classified controls into two categories (formal and informal controls).

Figure 2 A summary of control types

This study applies Snell's (Reference Snell1992) three-component model consisting of input, behaviour and output controls for several reasons. First, Walsh and Seward (Reference Walsh and Seward1990) argued that an ideal control model should regulate both ability and motivation. By applying Snell's (Reference Snell1992) three-component model, employees’ working abilities can be enhanced through input controls, while motivation can be enhanced through both behaviour controls (through standard operating procedures) and output controls (through the use of incentives). Second, Cardinal (Reference Cardinal2001) posited that Snell's (Reference Snell1992) three-component model provides a full range of organisational formal controls. The notion of input controls provides a ‘symmetrical counterpart’ to behaviour and output controls, since input controls manage the drivers of performance such as employee knowledge and skills, while behaviour and output controls manage the performance process and results, respectively (Snell, Reference Snell1992). Finally, this model has been empirically used in the management accounting literature (Snell & Youndt, Reference Snell and Youndt1995; Cardinal, Reference Cardinal2001; Cardinal, Sitkin, & Long, Reference Cardinal, Sitkin and Long2004; Abernethy, Schulz, & Bell, Reference Abernethy, Schulz and Bell2007; Johnson, Reference Johnson2011). While Merchant's (Reference Merchant1998) control model is similar to Snell's (Reference Snell1992) and has been widely used in the management accounting literature, it did not provide a comprehensive quantitative approach to measure the extent of use of each type of control and hence was not considered appropriate for a survey.

According to Snell (Reference Snell1992), input controls focus on staff selection and recruitment, and providing adequate training to ensure employees have the necessary knowledge and skills to perform their tasks. Input controls are also used to internalise organisational values by developing employees to become intrinsically committed to their organisation. Recruitment and training programmes are the most common input controls. Behaviour controls are imposed top-down with an emphasis on articulated operating procedures, close supervision, behavioural performance appraisal and feedback. Specifically, articulated operating procedures make employees fully informed as to what they should do, while close supervision enhances the likelihood that operating procedures are carried out as specified. Behavioural performance appraisal and feedback help to monitor and correct deviation from preset standards. Output controls standardise desired organisational outcomes. Employees are held accountable for the results regardless of the means they use to achieve the results. Performance appraisals are based on the results achieved and monetary rewards are directly related to performance outcomes.

The association between the types of controls and OLC stages

Previous studies show that since organisational features vary across OLC stages different controls are required to fit the different organisational contexts (Miller & Friesen, Reference Miller and Friesen1984; Kazanjian, Reference Kazanjian1988; Brignall, Reference Brignall1997; Moores & Yuen, 2001; Kallunki & Silvola, Reference Kallunki and Silvola2008). This study aims to extend the findings of Moores and Yuen (2001) who found that the formality of MASs varied across OLC stages. Organisations are expected to implement MASs along a control continuum with one end of the continuum more formal whereas the other end of the continuum more informal (Moores & Yuen, 2001; Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005). While Moores and Yuen (2001) focused on the overall extent to which formal controls are used within organisations, the current study is more specific focusing on three specific types of formal controls, that is input, behaviour and output controls. Accordingly, the following sections will develop hypotheses concerning the use of different types of controls in each OLC stage, and the use of each type of control across different OLC stages. Hypotheses will not be developed for the decline stage as previous studies (Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005; Kallunki & Silvola, Reference Kallunki and Silvola2008; Silvola, Reference Silvola2008) have found that it is difficult to obtain data from decline-stage organisations.

The use of different types of controls in each OLC stage

Birth stage

Given that birth-stage organisations are small and young with a limited number of employees (Miller & Friesen, Reference Miller and Friesen1984), top management does almost everything and directly supervises subordinates, thereby fostering the use of behaviour controls. In addition, as organisations attempt to develop a viable product for the first time, employees are less experienced than those in later OLC stages (Miller & Friesen, Reference Miller and Friesen1984). Challagalla and Shervani (Reference Challagalla and Shervani1997) suggested that behaviour controls, in a form of specifying job activities, can improve job performance for less experienced employees. Similarly, Bailyn (Reference Bailyn1985) argued that less autonomy and more behaviour controls play an important role in reducing employees’ job dissatisfaction in early OLC stages.

Due to the absence of a well-established reputation birth stage organisations must work hard to secure revenues by providing value to customers and satisfying them. Output controls are therefore perceived to be critical to ensure the achievement of desired outcomes. However, birth stage organisations are usually very unstable and thus it becomes difficult to pre-set desired outcomes against which performance can be measured (Abernethy, Schulz, & Bell, Reference Abernethy, Schulz and Bell2007). In a similar vein, Liao (Reference Liao2006) reported that in the birth stage the level of creativity tends to be high and the goals tend to be ambiguous. As a result, the availability of output measures is relatively low and output controls are considered to be inappropriate (Ouchi, Reference Ouchi1977; Jaeger & Baliga, Reference Jaeger and Baliga1985; Snell, Reference Snell1992; Snell & Youndt, Reference Snell and Youndt1995). Furthermore, since decision making and ownership are in the hands of top management, if output controls prevailed subordinates would have no significant influence on the results for which they would be held accountable. Accordingly, output controls are considered inappropriate in the birth stage (Merchant & Van der Stede, Reference Merchant and Van der Stede2003).

In regard to input controls, birth-stage organisations do not have established staffing policies and procedures, and staff experts are rarely used (Miller & Friesen, Reference Miller and Friesen1984). In addition, there would be relatively few staff meetings and little emphasis placed on training and recruitment programmes. Abernethy, Schulz and Bell (Reference Abernethy, Schulz and Bell2007) argued that the use of input controls is costly, and it is therefore less likely that input controls will be implemented to a great extent in birth stage organisations that have tight budgets. Wiesner, McDonald and Banham (Reference Wiesner, McDonald and Banham2007) also found that management practices such as staff recruitment and selection and staff training programmes are used to a low extent in small-sized firms.

Hypothesis 1: Business units in the birth stage of their OLC are expected to use behaviour controls to a greater extent than input and output controls.

Growth stage

In growth-stage organisations, a function-based structure is adopted with employees deployed in teams (Miller & Friesen, Reference Miller and Friesen1984). Teams are given a certain level of autonomy and independence to deal with an increasingly heterogeneous and dynamic environment (Ciavarella, Reference Ciavarella2001). With the high level of delegation of authority, output controls are expected to play an essential role in achieving desired organisational outcomes. However, Merchant and Van der Stede (Reference Merchant and Van der Stede2003) suggested that for output controls to work well, organisations must know what results are desired in the areas they intend to control, and how to measure the results effectively. Given the uncertain and dynamic environment in the growth stage, it is too difficult to predict future events and therefore less likely that appropriate performance criteria can be set to evaluate employee performance. Hence, output controls are less likely to be used to a great extent under these circumstances.

Cardinal (Reference Cardinal2001) argued that behaviour controls overemphasise the formality of processes and make employees less capable of dealing with the significant environmental uncertainty experienced in the growth stage. However, given that top management increasingly delegates authority to subordinates in the growth stage, and it is difficult to employ output controls due to the problems involved with setting appropriate performance criteria, Simons (Reference Simons1995) suggested that behaviour controls become critical to ensure that employees act in the best interests of their organisation. This argument is also supported by Moores and Yuen (2001).

Finally, organisations in the growth stage seek innovation and early diversification of their products, placing greater emphasis on the degree and variety of employees’ knowledge, skills and attitude towards their jobs (Sandelin, Reference Sandelin2008). Therefore, input controls such as recruitment and training programmes, become critical in this stage. This is consistent with Jensen's (Reference Jensen1998) argument that organisations with a dynamic environment are more likely to rely on employees’ capabilities.

Hypothesis 2: Business units in the growth stage of their OLC are expected to use behaviour and input controls to a greater extent than output controls.

Maturity stage

In the maturity stage, the organisational environment is relatively stable and there are many rules and regulations in place (Smith, Mitchell, & Summer, Reference Smith, Mitchell and Summer1985). The availability of desired performance criteria is fairly high and task programmability is nearly perfect. Bonner (Reference Bonner2005) suggested that the exclusiveness of behaviour controls in this OLC stage could lead to an over-focus on internal processes and an under-focus on external influences. Output controls can overcome this disadvantage by paying attention to the external financial market and environment. Accordingly, the use of both behaviour and output controls simultaneously is considered more appropriate than the use of either behaviour or output controls.

Instead of exploring new markets and developing new products, organisations in the maturity stage strive to maintain their market share for existing products. In this context, job descriptions and procedures become more formal and specified (Miller & Friesen, Reference Miller and Friesen1984) and there is less focus on professional and technical skills. In addition, innovation and learning are no longer the focus of organisations with employees concentrating on performing daily routine tasks. In these circumstances, employee selection, and training and development are not as crucial and hence input controls are expected to be used to a lesser extent.

Hypothesis 3: Business units in the maturity stage of their OLC are expected to use behaviour and output controls to a greater extent than input controls.

Revival stage

Due to the high level of risk taking and innovation, revival stage organisations are more likely to exhibit a high level of role ambiguity and uncertainty. According to Perrow (Reference Perrow1986) and Galbraith (Reference Galbraith1977), role ambiguity and uncertainty are best managed by the use of input controls. Similarly, Abernethy and Brownell (Reference Abernethy and Brownell1997) found that when task uncertainty is high input controls will have the greatest positive impact on organisational performance. Furthermore, firms in this stage are more likely to commit to learning due to the pursuit of substantial innovation, and will therefore prioritise the selection, training and development of employees (Abernethy, Schulz, & Bell, Reference Abernethy, Schulz and Bell2007). In addition, Cardinal (Reference Cardinal2001) found that input controls play a significant role in radical innovations, one of the major features of revival-stage organisations. This is consistent with the models of Snell (Reference Snell1992), Eisenhardt and Bourgeois (Reference Farr-Wharton and Brunetto1988), Ouchi (Reference Ouchi1977, Reference Ouchi1978) and Thompson (Reference Thompson1967), which suggest that when task programmability is imperfect and standards of desirable performance are ambiguous, input controls are the best option.

In addition, the use of behaviour controls can contribute to the reduction of ambiguity and uncertainty, as the formalisation of rules and procedures and frequent observation provides employees with information about what they should do and how tasks should be completed. For example, Merchant (Reference Merchant1984, Reference Merchant1981) found that as organisational structure becomes more complex, organisations are more likely to decentralise and implement more administratively oriented controls with a high level of behaviour formalisation. Furthermore, Farr-Wharton and Brunetto (Reference Eisenhardt and Bourgeois2007) argued that organisational documents and manuals, which contribute to improving the communication between different levels within organisations, can assist employees in better accepting organisational changes.

Although the launch of a unique product requires strong basic research and development and the success of such products cannot be evaluated in the short run, revival-stage firms are still expected to use output controls to a great extent. This is because having gone through the maturity stage, such firms have well-established knowledge regarding desired results and have already developed the ability to measure results effectively. More importantly, after experiencing temporary decline at the end of the maturity stage, revival-stage firms are forced to focus on product diversification and innovation as a means of survival (Miller & Friesen, Reference Miller and Friesen1984). In such a situation any unsuccessful launches of products could accelerate the arrival of the decline stage, and hence, output controls become vital to ensure the achievement of desired organisational outcomes.

Hypothesis 4: Business units in the revival stage of their OLC are expected to use input, behaviour and output controls to a similar extent.

The use of each type of control across OLC stages

Input controls

In the birth stage, given that the product market is uniform and narrow there is little need for staff experts, with the founders taking responsibility for almost every aspect of their organisation, including the manufacturing of products (Kallunki & Silvola, Reference Kallunki and Silvola2008). Hence, the use of input controls, focusing on staff recruitment and training, and developing employees’ knowledge and skills, is not expected to be as prevalent in the birth stage.

As organisations move to the growth stage, function-oriented departments are established and employees are required to perform a wider range of tasks (Lester, Parnell, & Carraher, Reference Lester, Parnell and Carraher2003; Bartol et al., 2008). Firms aim to broaden product lines with the pursuit of diversification and growth (Miller & Friesen, Reference Miller and Friesen1984). Such aims can be facilitated by the hiring of more professional and experienced employees who are capable of providing a more complete array of products in an existing market, or tailoring new products to a new market (Johnson, Reference Johnson2011). As a result, the use of input controls becomes more important in the growth stage than in the birth stage, in an attempt to improve employees’ knowledge, skills and attitudes towards their jobs (Sandelin, Reference Sandelin2008).

Compared to growth-stage organisations, maturity-stage organisations are embedded in a much more stable organisational environment. The availability of standardised work procedures and specific job descriptions, and the decreased emphasis on product innovation lowers the demand placed on employees’ professional and technical skills. Accordingly, input controls are expected to be used to a lesser extent in the maturity stage than in the growth stage.

Firms shift their emphasis to major innovation and diversification when they reach the revival stage. In order to create an innovative organisational environment, employees are given more autonomy and freedom in their work, and consequently higher demands are placed on employees’ competencies. In addition, Galbraith (Reference Galbraith1977) reported that uncertainty is best managed via the use of input controls. Due to the highly competitive and uncertain environment in this stage, employees are required to have superior knowledge, skills and experience to deal effectively with all potential threats and opportunities in a timely manner. Given that recruitment policies can enhance the likelihood of a workforce capable of producing the creativity warranted in this stage, and training and development programmes can enhance the competency of staff, input controls are expected to be used to a greater extent in the revival stage than in the maturity stage.

Hypothesis 5: Business units are expected to use input controls to a greater extent in the growth and revival stages than in the birth and maturity stages.

Behaviour controls

In the birth stage, products are homogeneous and simple, and the number of employees is limited. Therefore, managers are able to closely observe employees’ ongoing behaviour (Snell & Youndt, Reference Snell and Youndt1995). However, both Miller and Friesen (Reference Miller and Friesen1984) and Simons (Reference Simons1995) argued that given the structure of birth-stage firms is very simple, few formal policies and procedures are in place. Accordingly, in line with Snell's (Reference Snell1992) assertion that behaviour controls mainly consist of articulated operating procedures and policies, and close supervision, behaviour controls are therefore only expected to be used to a moderate extent in the birth stage.

As organisations expand, management is less able to observe operations directly, and is therefore required to introduce formal rules and procedures to monitor employees’ performance. For instance, Simons (Reference Simons1995) argued that with the increased delegation of decision-making power to subordinates, it becomes very important to clarify strategic boundaries and specify business activities in order to reduce the likelihood of bad investments in the growth stage. Similarly, Merchant and Van de Stede (Reference Merchant and Van der Stede2003) suggested that by specifying and clarifying the nature of tasks for employees and through direct supervision, behaviour controls can alleviate employees’ feelings of a lack of direction in such a highly uncertain and competitive organisational environment. Consequently, behaviour controls are expected to be used to a greater extent in the growth stage than in the birth stage.

As organisations continue to develop and reach the maturity stage, formal rules and procedures are in place. Management in this stage have sufficient knowledge in regard to the process by which inputs are converted into outputs, with Snell (Reference Snell1992) and Jaeger and Baliga (Reference Jaeger and Baliga1985) maintaining that behaviour controls prevail when the availability of the knowledge relating to transformation processes from input to output is relatively high. Furthermore, behaviour controls, such as specifying when and how tasks are to be completed, frequently monitoring progress, and making ongoing adjustments, can help to document best practices (Merchant & Van de Stede, Reference Merchant and Van der Stede2003), thereby contributing to the improvement in the level of productivity and efficiency in the maturity stage. Hence, behaviour controls are expected to be just as relevant in the maturity stage as in the growth stage.

When organisations enter the revival stage, divisional structures are adopted to deal with the increased market heterogeneity, with divisional managers overseeing and held responsible for the performance of their own divisions (Miller & Friesen, Reference Miller and Friesen1984). Behaviour controls, particularly in the form of procedures and policies, thereby provide an efficient way to facilitate organisational coordination among different divisions (Merchant & Van de Stede, Reference Merchant and Van der Stede2003). In addition, although revival-stage firms emphasise innovation and creativity, the complexity of markets, as well as the uncertainty and competitiveness of the organisational environment, make it imperative for top management to monitor their employees’ behaviour and performance to ensure firms develop in an orderly manner (Miller & Friesen, Reference Miller and Friesen1984). Hence, behaviour controls are expected to be just as relevant in the revival stage as in the maturity stage.

Hypothesis 6: Business units are expected to use behaviour controls to a greater extent in the growth, maturity and revival stages than in the birth stage.

Output controls

Merchant and Van der Stede (Reference Merchant and Van der Stede2003) argued that in order to make output controls work effectively, subordinates should have a certain level of control over their tasks. Given that in the birth stage ownership is tightly concentrated in the hands of a few individuals, with little authority delegated to subordinates (Miller & Friesen, Reference Miller and Friesen1984), output controls are not expected to be used to a great extent in this stage. Furthermore, with the limited number of employees and the simple organisational structure in the birth stage, management have sufficient knowledge in regard to all aspects of their business’ day-to-day operations, and therefore are expected to place less demand on output controls.

The organisational environment in the growth stage becomes more heterogeneous and competitive, with efforts devoted to broadening product lines by diversification and innovation (Miller & Friesen, Reference Miller and Friesen1984). Hence, in comparison to the birth stage which focuses on routine administration, management in the growth stage must pay more attention to monitoring and evaluating the financial performance of various divisions. In addition, as organisations expand and grow, management is less likely to involve themselves in all business activities, and hence there will be a greater reliance on the use of output controls to monitor the achievement of desired organisational goals (Simons, Reference Simons1995). As a result, output controls are expected to be used to a greater extent in the growth stage than in the birth stage.

Compared to growth-stage organisations, maturity-stage organisations have a relatively stable environment, and specific operational procedures and policies are in place (Miller & Friesen, Reference Miller and Friesen1984). With employees performing routine and repetitive tasks in this stage, output controls play a significant role in enhancing employees’ work commitment and motivation, especially when performance is linked with employee rewards (House, Reference House1996; Phoenix, Reference Phoenix2006). Such employee compensation schemes can subsequently lead to improved productivity and efficiency, two main strategies pursued in the maturity stage. In addition, output controls are appropriate due to the high level of stability in the maturity stage which allows organisations to clearly set desired performance criteria (Jaeger & Baliga, Reference Jaeger and Baliga1985; Snell, Reference Snell1992), and subsequently facilitates the use of output controls (Ouchi, Reference Ouchi1979). Hence, in the maturity stage output controls are expected to be as relevant as in the growth stage.

Revival-stage organisations enter a highly heterogeneous, competitive and dynamic environment. The use of output controls, which do not require a great level of scrutiny from management (Christ, Sedatole, Towry, & Thomas, Reference Christ, Sedatole, Towry and Thomas2008), allows management to reserve their attention for important strategic issues. Merchant and Van der Stede (Reference Merchant and Van der Stede2003) proposed that output controls are particularly desirable where creativity plays a crucial role. The autonomy embedded in output controls provides employees with more freedom and flexibility in their work (Christ et al., Reference Christ, Sedatole, Towry and Thomas2008), and therefore facilitates the implementation of the innovation strategy employed in the revival stage. Furthermore, given business units reaching this stage have already established knowledge relating to desired results and appropriate output measures, such controls are considered appropriate in the revival stage. Hence, output controls are expected to be as relevant in the revival stage as in the maturity stage.

Hypothesis 7: Business units are expected to use output controls to a greater extent in the growth, maturity and revival stages than in the birth stage.

Method

A survey questionnaire was mailed to 1,000 General Managers from a random sample of Australian manufacturing organisations chosen from the Kompass Australia Database (2010). In order to increase the response rate, Dillman's (Reference Dillman2007) ‘Tailored Design MethodFootnote 3’ was followed for the design and distribution of the questionnaire. Australian manufacturing organisations were chosen because they play a significant role in the Australian economy. Specifically, the Australian manufacturing industry made the second highest contribution to Australian gross domestic Product and accounted for almost 10% of total employment in Australia (Manufacturing Industry Brief 2008–2009). Surveys were distributed to General Managers, who were asked to complete the questionnaire for a business unit within their organisation. General Managers were selected for two reasons. First, they were considered to be the most appropriate respondents to identify OLC stages in their chosen business unit. Second, given that General Managers are the designers of controls in organisations, it is believed that they can provide the most reliable information in regard to the controls used in their business units. The business unit was chosen as the unit of analysis since different business units in an organisation may fall into different life cycle stages, making it difficult to complete the survey at the corporate level.

Three hundred and forty three responses were received for a response rate of 34.3%. These comprised 214 (21.4%) from the initial distribution of the questionnaires and 129 (12.9%) from the follow-up mail-out. This response rate was considered to be good given that recent management accounting studies associated with OLC stages have indicated response rates in the range of 10–25% [Moores & Yuen, 2001 (14.5%); Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005 (15.5%); Kallunki & Silvola, Reference Kallunki and Silvola2008 (21%)]. Eighty-six per cent of respondents were General Managers, with the remainder having similar titles, while the respondents had worked in their positions for 9.9 years on average. A test for non-response bias was conducted by comparing the responses of early and late respondents for each of the independent and the dependent variables. There were no significant differences between early respondents and late respondents for any of the variables. Hence, there were no problems regarding non-response bias for the data obtained.

Compared to Moores and Yuen (2001), this study provides more powerful data in two ways. First, the study incorporated 277 usable responses for data analysis as opposed to 49 usable responses in Moores and Yuen (2001). According to Singleton and Straits's (Reference Singleton and Straits2005: 141) argument that ‘the larger the sample, the greater the precision of the sample estimate’, the current study's results are more precise. Second, the target population in the study is spread across all states in the Australian manufacturing industry, with employee number ranging from one to 2,200. In contrast, Moores and Yuen (2001) targeted specific types of Australian manufacturers, clothing and footwear manufacturers, who were located mainly in Victoria, New South Wales and Queensland, and who had <1,000 employees. Accordingly, the sample applied in the current study exhibits a higher level of generalisability.

Variable measurement

OLC stages

A number of studies have utilized the self-categorisation approach which relies on respondents’ perception of their business unit's OLC stage (Kazanjian & Drazin, Reference Kazanjian and Drazin1990; Auzair & Langfield-Smith, Reference Auzair and Langfield-Smith2005; Kallunki & Silvola, Reference Kallunki and Silvola2008). This approach only provides respondents with the names of the OLC stages and asks them to tick a box that describes their stage of development. Consequently, the failure to convey what defines a particular stage may lead to misunderstanding of their actual OLC stage and inconsistency between respondents who have different perceptions about the OLC stages. Accordingly, a more comprehensive cluster analysis approach, classifying organisations into their OLC stages based on a number of organisational characteristics, was considered to be more appropriate. According to Ketchen and Shook (Reference Ketchen and Shook1996), cluster analysis is a statistical technique that groups observations into clusters so that observations in the same cluster are homogeneous and there is heterogeneity across clusters. This approach minimises the statistical variance among organisations within the same cluster and maximises the variances between clusters. Cluster analysis permits the inclusion of multiple variables as sources of the configuration definition without over-specifying the model.

The study applied an adapted version of Miller and Friesen's (Reference Miller and Friesen1984) 54-item instrument to measure OLC stages. Without compromising the accuracy and completeness of the measurement, the 54 items were reduced to 38 items by eliminating items which were ambiguous, duplicated and/or considered irrelevant to the context of the current study. The instrument consists of four variables (strategy, organisational situation, structure and decision-making style), with respondents required to indicate the extent to which each item was reflected in their business unit, using a 5-point scale with anchors of ‘Not at all’ and ‘To a great extent’. The four variables represent formative indicators of OLC stages with changes in each of these variables causing changes in the determination of the OLC stages.

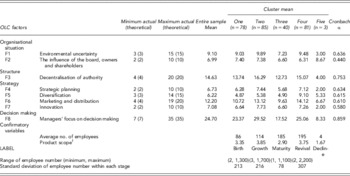

In order to classify organisations into OLC stages, this study follows the procedures applied in Moores and Yuen (2001), whereby factor analysis (principal component with varimax rotation) was conducted to reduce the 38 items to a manageable set of data. Factor analysis resulted in eight factors, two relating to organisational situation, one relating to structure, four relating to strategy and one relating to decision-making style. The specific items loading on each factor are shown in Appendix A, with each factor subsequently scored as the sum of the items loading clearly on each other.

The factor scores were subsequently used in cluster analysis with organisations forced into five clusters so as to be consistent with Miller and Friesen's (Reference Miller and Friesen1984) five-stage life cycle model. Cluster analysis was performed using the hierarchical agglomerative technique with Ward's minimum variance method for distance measure between two sub-groups. Table 1 reveals that as a result of the clustering procedures, 78 organisations were categorised into Cluster one, 85 in Cluster two, 40 in Cluster three, 81 in Cluster four and three in Cluster five. Table 1 also provides the mean scores for each factor across the clusters, and demonstrates the validity of the constructs with each of the Cronbach α values at an acceptable level of 0.4 or higher (Sproles & Kendall, Reference Sproles and Kendall1986; Mital, Desai, Subramanian, & Mital, Reference Mital, Desai, Subramanian and Mital2008).

Table 1 Descriptive statistics: mean values for each OLC factor across clusters

Notes. The product scope was measured with scores ranging from 0 to 5.

OLC = organisational life cycle.

The comparison of the characteristics across the five clusters facilitates the determination of an appropriate label (birth, growth, maturity, revival and decline) for each cluster, in accordance with the characteristics of the OLC stages proposed by Miller and Friesen (Reference Miller and Friesen1984).

Business units in Cluster five exhibited the highest centralised-structure with little delegation of authority. Ownership is tightly held and the Board of Directors and shareholders exercise the greatest degree of power. Such a management style suggests that there is poor communication between top managers and subordinates which stifles the ability of business units to react promptly to the challenges confronting them. Little effort is devoted to strategic planning, diversification, marketing and distribution and the emphasis on innovation is also very low. No particular strategy is pursued, representing a muddle through management style. Multiplexity and integration of decisions are not taken into account when making decisions, with a minimal amount of analysis involved. The pattern revealed in this cluster is consistent with the characteristics of the decline stage described in Miller and Friesen (Reference Miller and Friesen1984).

Business units in Clusters two and four have approximately similar scores for most of the OLC factors. All the scores from these two clusters are generally higher than scores from the other three clusters. In regard to organisational situation, business units in these two clusters have a relatively high level of dynamism, hostility and heterogeneity. Significant effort is devoted to facilitating the communication between top managers and subordinates to ensure more effective coordination. For strategy, the high scores indicate a greater emphasis on strategic planning, diversification (particularly for Cluster four), marketing and distribution, and innovation. High scores were also shown for the ‘Environmental uncertainty’ factor for both clusters. The decision-making style appears to be more analytical and multiplex with better integration compared to the other three clusters (particularly for Cluster two). The characteristics discussed above signify that business units in Clusters two and four correspond to either the growth or revival stages.

A further comparison of these two clusters reveals that Cluster four has a significantly higher score for the ‘Diversification’ factor than Cluster two. Since the emphasis of growth-stage organisations is early diversification, while the emphasis of revival-stage organisations is extensive diversification (Miller & Friesen, Reference Miller and Friesen1984), it is expected that business units in the revival stage will exhibit a higher score for the ‘Diversification’ factor. Furthermore, Cluster four exhibited a significantly lower score than Cluster two for the ‘The influence of the board, owners and shareholders’ factor. Miller and Friesen (Reference Miller and Friesen1984) proposed that ownership becomes even more dispersed in the revival stage than the growth stage. Hence, it is expected that the influence of the board, owners and shareholders would be lower in revival-stage business units. As a result, it is more likely that business units in Cluster two are in the growth stage, while those in Cluster four are in the revival stage.

Business units in Cluster three appear to be conservative with less emphasis on diversification. The business environment is quite stable, perhaps as a result of the low levels of innovation and diversification. A low score for the ‘Influence of the board, owners and shareholders’ factor indicates that ownership is widely dispersed. Structure remains fairly centralised without a great deal of delegation of decision making. This structure style is justified by the simplicity and stability of operations which make it easier for only a few key managers to dominate. Decisions become less adaptive and responsive due to the less innovative and proactive decision-making style, as indicated by the low scores for the ‘Managers’ focus on decision making’ factor. These characteristics closely resemble the characteristics of the maturity stage described by Miller and Friesen (Reference Miller and Friesen1984).

Business units in Cluster one exhibited the lowest scores for the ‘Diversification’ factor, indicating the pursuit of a niche strategy. Ownership is tightly concentrated in the hands of a few individuals with a high score reported for the ‘Influence of the board, owners and shareholders’ factor. The centralised ownership also results in simple and centralised structures. Top managers make their decisions largely based on their intuition without extensive analyses involved in the decision-making process. The pattern revealed in this cluster describes the characteristics expected in the birth stage as described by Miller and Friesen (Reference Miller and Friesen1984).

Having compared the characteristics of business units in the five clusters with those of the birth, growth, maturity, revival and decline stages proposed by Miller and Friesen (Reference Miller and Friesen1984), the relevant OLC labels have been assigned to each cluster. Specifically, the five clusters are labeled Birth (Cluster one), Growth (Cluster two), Maturity (Cluster three), Revival (Cluster four) and Decline (Cluster five).

To confirm the cluster labeling, additional information regarding the average number of employees and product scope for business units within each of the five clusters was collected, with the mean values reported in Table 1. Table 1 reveals that the average number of employees increases across the birth, growth, maturity and revival stages but decreases in the decline stage, which is in line with Miller and Friesen's (Reference Miller and Friesen1984) descriptions of OLC stage characteristics. In addition, the broader product scope in the growth and revival stages compared with the birth and maturity stages, and the narrower product scope in the decline stage are also in line with Miller and Friesen's (Reference Miller and Friesen1984) descriptions. Therefore, the classification of OLC stages from cluster labeling was considered to be appropriateFootnote 4.

Types of controls

This study incorporates reflective indicators of the three types of controls, using an adapted version of Snell's (Reference Snell1992) instrument. Minor adjustments to the wording were made so as to fit the context of this study, and respondents were asked to indicate the extent to which each item was reflected in their business unit using a 5-point scale with anchors of ‘Not at all’ and ‘To a great extent’.

For input controls, a seven-item measure was used to assess the extent of emphasis placed on the recruitment and orientation of new staff, establishing staffing procedures and adhering to these procedures, and employee training and staff development. The extent of input controls used was measured as the average score of these seven items, with higher (lower) scores representing a higher (lower) extent of use of input controls. For behaviour controls, a six-item measure was applied to assess the extent to which employees were held accountable for their actions, employees’ actions were monitored to ensure compliance with staffing policies and procedures, standards and procedures were imposed top-down, and employee performance was evaluated based on their on-going behaviour. One item (see Behaviour control item 6 in Appendix A) was deleted from the calculation of the average score due to a low score in the reliability test. Hence, the extent of behaviour controls used was measured as the average score of the remaining five items, with higher (lower) scores representing a higher (lower) extent of use of behaviour controls. For output controls, a six-item measure was used to assess the extent to which clear and planned performance targets were set for employees, pre-established targets were used as a benchmark for employee evaluation, performance evaluation was based on results achieved regardless of what employees were like personally, and employee rewards were linked to results. The extent of output controls used was measured as the average score of these six items, with higher (lower) scores representing a higher (lower) extent of use of output controls.

Results

The extent of use of controls in each OLC stage

Table 2 panel A provides the results of the pairwise comparisons of the extent of use of different types of controls in the birth, growth, maturity and revival stages. In the birth stage, input and behaviour controls were used to a significantly greater extent than output controls at the 5% significance level. This result partially supports Hypothesis 1, with behaviour controls used to a greater extent than output controls. However, the finding that input controls were used to a significantly greater extent than output controls and to a similar extent as behaviour controls was not expected. This finding, while surprising, may reflect the learning-oriented nature of birth stage organisations (Miller & Friesen, Reference Miller and Friesen1984). For instance, Abernethy, Schulz and Bell (Reference Abernethy, Schulz and Bell2007) found that employing individuals with appropriate skills and attitudes, or training existing employees to improve their skills and attitudes can help with the implementation of an organisational learning orientation.

Table 2 Results of pairwise comparison comparing the extent of use of each type of control in each OLC stage and across OLC stages

Notes. aSome respondents failed to provide answers concerning the use of controls and hence were excluded from this analysis.

OLC = organisational life cycle.

*Significant at the 10% level.

**Significant at the 5% level.

In the growth stage, behaviour controls were found to be used to a significantly greater extent than output controls at the 5% significance level. Input controls were also found to be used to a greater extent than output controls, although only at the 10% significance level. Therefore, support is provided for Hypothesis 2, which stated that business units in the growth stage are expected to use behaviour and input controls to a greater extent than output controls. The extensive use of behaviour controls is justified as they mitigate the level of uncertainty and increase the level of predictability by routinising the product transformation process (Snell & Youndt, Reference Snell and Youndt1995), while the extensive use of input controls may be attributable to the increasing reliance on employees’ knowledge and skills in performing their jobs in the growth stage.

In the maturity stage, behaviour and output controls were hypothesised to be used to a greater extent than input controls. However, no significant differences were found in the extent of use of the three types of controls, indicating that input controls were used to a greater extent than was anticipated. Hypothesis 3 is therefore not supported. A possible explanation may be that training, career planning, and development programmes have been developed in an attempt to retain well-performing employees, given today's high labour cost and low levels of employee loyalty (Samson & Daft, Reference Samson and Daft2005; Beatson, Lings, & Gudergan, Reference Beatson, Lings and Gudergan2008). The retention of competent employees can subsequently facilitate the achievement of efficiency and productivity, which are major strategies pursued by maturity stage firms as suggested by Miller and Friesen (Reference Miller and Friesen1984).

In the revival stage, all three types of controls were found to be used to a similar extent, and hence Hypothesis 4 is supported. The importance of the use of all three types of controls in the revival stage could be explained by the argument that to respond to the dynamic and challenging environment experienced in the revival stage, the use of input controls assists organisations in carefully selecting, training and developing current and future employees, while the freedom and autonomy associated with output controls foster employees’ creativity and innovation. In addition, with increased freedom and delegated decision-making rights, the use of behaviour controls helps to limit individuals’ undesirable behaviour and enhance the likelihood of achieving organisational goals.

The extent of use of controls across OLC stages

Pairwise comparisons were also performed to examine the extent of use of each type of control across OLC stages, with the results shown in Table 2 Panel B. Consistent with Hypothesis 5 input controls were used to a significantly greater extent in the growth and revival stages than the birth and maturity stages. Similarly, both behaviour and output controls were used to a significantly greater extent in the growth and revival stages than the birth and maturity stages. Hence, Hypotheses 6 and 7 are not fully supported, given that maturity-stage business units used behaviour and output controls to a lesser extent than was expected. The unexpected findings that all three types of controls are used to a low extent in the maturity stage could be explained by the argument that well-established maturity stage organisations, which are embedded in a relatively stable environment, tend to place more emphasis on informal controls. Hence, formal controls such as budgeting and performance measures may be supplemented with informal controls such as internal informal meetings and communications, thereby allowing a more flexible management style (Moores & Yuen, 2001).

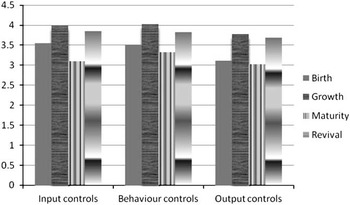

Figure 3 provides a summary of the extent of use of each of the three types of controls across OLC stages illustrating that all three types of controls were used to a significantly greater extent in the growth and revival stages than the birth and maturity stages.

Figure 3 The pattern of use of controls across organisational life cycle (OLC) stages

Table 3 provides a summary of the seven hypotheses developed and the results obtained.

Table 3 Summary of the results for each hypothesis tested

Conclusion and discussion

This study contributes to the MCS literature by examining the association between the use of Snell's (Reference Snell1992) three types of controls and OLC stages. In particular, using Miller and Friesen's (Reference Miller and Friesen1984) life cycle model, this study investigated how the use of input, behaviour and output controls differed in each OLC stage and across OLC stages in Australian manufacturing organisations. Gordon and Miller (1976) first claimed that contextual factors should be considered in combination with Moores and Yuen (2001) examining the association between organisational variables (strategy, structure, leadership and decision-making styles), whose combined fit was represented by OLC stages, with MAS formality. By adopting Miller and Friesen's (Reference Miller and Friesen1984) model the current study contributes to the literature employing this configuration form of contingency fit. Furthermore, the study extends the OLC findings of Moores and Yuen (2001) by focusing on the use of these three specific types of formal controls.

The results show that output controls were used to a lesser extent than input and behaviour controls in the birth and growth stages, and used to a similar extent as input and behaviour controls in the maturity and revival stages. In addition, the results reveal that the extent of use of each type of control varies across OLC stages, exhibiting a similar pattern, with all three types of controls used to a greater extent in the growth and revival stages compared to the birth and maturity stages.

The finding that all three types of controls were used to a greater extent in the growth stage than in the birth stage concurs with Davila's (Reference Davila2005) findings that the use of personnel, action and results controls increase over time from the birth to growth stage. The results are however inconsistent with Auzair and Langfield-Smith's (Reference Auzair and Langfield-Smith2005) finding that maturity-stage organisations focus on bureaucratic MCSs more than growth-stage firms. This conflict may be attributable to the different setting in which the two studies were conducted, with Auzair and Langfield-Smith's (Reference Auzair and Langfield-Smith2005) study conducted in the service sector and the current study conducted in the manufacturing industry. Accordingly, it is suggested that future studies could explore the hypothesised associations further within the service sector.

The findings are consistent with those of Moores and Yuen (2001), who found that organisations’ reliance on MAS formality increases from the birth to growth stage, decreases in the maturity stage and increases again in the revival stage. Moores and Yuen (2001: 358) claimed that the level of formality is influenced by the decision-making style with growth and revival stage organisations adopting integrative and flexible based decision-making styles, respectively. As a means of coping with the greater uncertainty in these environments, the level of MAS formality is anticipated to be higher. Our study makes an additional contribution by focusing on three specific formal controls (i.e., input, behaviour and output controls) rather than the overall extent to which formal controls are used within organisations.

Due to the difference in the emphasis placed on each type of control across OLC stages, the findings highlight the importance of being aware which OLC stage a business unit is in. In particular, awareness of a business unit's characteristics and the extent to which those characteristics reflect a different OLC stage could alert practitioners to adjust their emphasis on each type of control accordingly. This is important, for if organisation fails to adopt appropriate controls during the transition it will result in ‘organisational transitional pains’ (Flamholtz, Reference Flamholtz1995: 47).

While the study did not intend to provide an insight into the success of specific controls in different OLC stages, the observance of current practices does however provide knowledge about the suitability of specific types of controls for business units in different stages of the OLC. For instance, the findings indicate that in business units which are in the birth and growth stages, more emphasis was placed on input controls such as staff selection, training and development, and behaviour controls such as specifying and monitoring operating procedures. Less emphasis was placed on output measures suggesting that such measures are not as appropriate. Alternatively, business units which are in the maturity and revival stages were found to place a similar emphasis on all three types of controls. Therefore they should consider concentrating on staff recruitment and skill development, monitoring the behaviour of employees, and also focusing on result-oriented performance measures.

While this study makes a significant contribution to the literature examining the association between MCSs and OLC stages, it is subject to some limitations. For instance, while cluster analysis is considered to be superior to the self-categorisation approach it has been criticised due to the reliance on research judgement in respect to the factor analysis and subsequent labelling of clusters. In addition, this study is potentially subject to common method bias given that the self-report data obtained on all variables were from the same individuals, General Managers. Future studies could collect data from different sources such as lower-level managers so as to minimise the effect of common method bias. Future studies could also explore if similar findings are reported in alternative industries. Furthermore, instead of applying Snell's (Reference Snell1992) three-component control model, which does not include any informal controls, a future study could examine the association between controls and OLC stages in respect to both formal and informal controls. Finally, given that the present study only examines the use of different types of controls in each OLC stage, future studies could investigate how different types of controls are used (i.e., diagnostically or interactively) from a life cycle perspective.

Appendix A

The instrument of OLC stages

Please indicate the extent to which the following statements reflect the work environment in your business unit (1 = not at all, 5 = to a great extent).

Situation

F1: Environmental uncertainty

1.1 Dynamism (evidenced by the unpredictability of changes in customer tastes, production technologies).

1.2 Hostility (evidenced by the intensity of competition and other external influences).

1.3 Heterogeneity (evidenced by the differences in competitive tactics, customer tastes, product lines, channels of distribution).

F2: The influence of board, owners and shareholders

2.1 The decisions and operations are influenced by the boards of directors.

2.2 The decisions and operations are influenced by owners/shareholders.

Structure

F3: Decentralisation of authority

3.1 Participative Management.

3.2 Effective internal communication systems.

3.3 Delegation of decision making.

3.4 Proactive decision making.

Strategy

F4: Strategic planning

4.1 Action planning (includes formal strategic and project planning and review procedures, the use of capital budgeting techniques, and market forecasting).

4.2 Scanning (involves identification of threats and opportunities in the external environment of your business unit)

F5: Diversification

5.1 Use acquisition to diversify into unrelated lines.

5.2 Diversifies into unrelated lines by establishing our own departments or subsidiaries.

5.3 Engages in vertical integration.

F6: Marketing and distribution

6.1 Has major, frequent product innovations.

6.2 Dominates distribution channels.

6.3 Extensive advertising and promotional expenditure.

6.4 Provides different product lines for different markets.

F7: Innovation

7.1 Has small, incremental product innovations.

7.2 Selective in respect to the introduction of new products.

Decision-making style

F8: Managers’ focus on decision making

8.1 Centralisation of strategy formulation.

8.2 Extensive analysis of major decisions.

8.3 Multiplexity of decisions (consideration of a broad range of factors in making strategic decisions).

8.4 Integration of decisions (actions in one area of the firm are complementary or supportive of those in other areas (i.e., divisions, functions).

8.5 Futurity of decisions (our business unit incorporates a long-term planning horizon relative to our industry).

8.6 Consciousness of strategies (concerns the degree of your conscious commitment as a business unit manager to an explicit corporate strategy).

8.7 Adaptiveness of decisions (concerns the responsiveness and appropriateness of decisions to market requirements and external environmental conditions).

Notes

Eleven items did not load onto any of the eight factors and are listed below:

1. Follows the lead of competitors.

2. Adopts a niche strategy.

3. Engages in price cutting.

4. Charges a premium for high-quality products.

5. The decisions and operations of our business unit are influenced by customers.

6. The decisions and operations of our business unit are influenced by managers.

7. Sophisticated Management Information Systems.

8. Technocratisation (a higher proportion of highly trained staff specialists and professionally qualified people (accountants, engineers, scientists) as a percentage of the number of employees).

9. Resource shortages (human, physical and financial shortages).

10. Risk taking.

11. Industry expertise of top managers (they are in a position to make decisions because of their excellent knowledge of internal operations and the outside environment).

Types of controls

Please indicate the extent to which the following statements reflect the work environment in your business unit (1 = not at all, 5 = to a great extent).

Input controls

1. Employees must undergo a series of evaluations before they are hired.

2. Employees receive substantial training before they assume new responsibilities.

3. New employees undergo orientation regarding organisational activities.

4. Our business unit has gone to great lengths to establish staffing policies and procedures.

5. Employees are expected to adhere to established staffing policies and procedures.

6. Employees are given ample opportunity to broaden their range of talents.

7. Our business unit provides on-going training and skill development to employees.

Behaviour controls

1. Employee performance is evaluated based on their on-going behaviour.

2. Employees are held accountable for their actions, regardless of results.

3. Employees are monitored to ensure that they are complying with staffing policies and procedures.

4. Supervisors regularly monitor the actions undertaken by employees.

5. Employees are accountable for areas of responsibilities that are defined by top managers.

6. Subordinates assume responsibility for setting their own performance goals (R).

Output controls

1. Performance evaluations place emphasis on results.

2. There are clear and planned performance targets set for employees.

3. Pre-established targets are used as a benchmark for evaluations.

4. Regardless of what employees are like personally, their performance is judged by results achieved.

5. The rewards employees receive are linked to results.

6. Employees who do not reach objectives receive a low performance rating.