1. INTRODUCTION

The difference between the EU15 and US unemployment rates in recent decades is well known. European unemployment was low during the 1960s but started to increase in the 1970s, and rose above the US rate in the early 1980s, where it has remained ever since. This phenomenon is often referred to as the EU–US unemployment puzzle. The earlier literature, starting with Nickell (Reference Nickell1997), often emphasized the role of changes in labor-market institutions (LMIs) to explain this gap. In particular, this literature showed that greater institutional rigidities are a central cause of Europe’s bleak unemployment performance. Aging may also affect unemployment. In the overlapping-generations (OLG) approach, life expectancy typically stimulates savings [e.g., Attanasio et al. (Reference Attanasio, Kitao and Violante2007)]. In closed economies, higher savings automatically generate investment, which reduces unemployment. This is the main finding of de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013). As a result, a fast-aging area such as Europe should experience a low unemployment rate, all else equal, a finding at odds with the puzzle mentioned above. However, in an open-economy framework, capital mobility may blur this savings-investment link [see for instance, Flodén (Reference Flodén2003), Domeij and Flodén (Reference Domeij and Flodén2006), and Börsch-Supan et al. (Reference Börsch-Supan, Ludwig and Winter2006)] and, hence, that between aging and unemployment when countries are characterized by differential aging. In this paper, we investigate how each of LMIs, aging, and capital flows contribute to the EU–US unemployment gap.

We first construct a two-period two-region general-equilibrium model with OLG dynamics. To generate unemployment, we follow the search and matching literature [Pissarides (Reference Pissarides2000)] and allow capital to move – or not – between regions. We use this model to demonstrate analytically the implications of LMIs (here unemployment- and pension-replacement rates), fertility and aging on savings, (un)employment and capital flows. We then set up a quantitative model with a larger number of generations and endogenous labor supply. We calibrate this model using EU15 and US data and also feed in the historical and projected changes in (i) LMIs and (ii) demography. We quantitatively assess its ability to explain the observed changes in the individual (EU15 vs. US) unemployment rates between 1960 and 2010, as well as the unemployment-rate gap.Footnote 1

Our main findings can be summarized as follows. First, institutional features alone, i.e., the asymmetric strengthening of LMIs with an EU15 bias, reproduces changes in the individual unemployment rates between 1960 and 2010, and that in the gap, reasonably well. The average error (between the observed and simulated data) for the individual unemployment rates is 0.9 percentage points (pp) and that for the gap is 1.1 pp. Adding demographic changes in closed economies, i.e., asymmetric aging with a EU15 bias, worsens the fit: the relatively higher savings in the EU reduce the real interest rate, which stimulates job creation and lowers unemployment. However, introducing open economies allows capital to flow from Europe to the US and this lowers EU unemployment that is, in some sense, exported. This final model (with institutions, demography, and capital flows) performs the best, with the average error for the individual unemployment rates becoming 0.8 pp and that for the gap 0.9 pp Second, although the model performs well in terms of unemployment, it does exaggerate the extent of capital flows. We therefore introduce restrictions on capital mobility to exactly match the historical change in EU–US net foreign assets (NFAs). The unemployment fit remains almost as good as in the frictionless model. We also discuss extensions with possible implications for savings and capital flows, such as capital taxes, an imperfect annuity market, and the introduction of a third region. Third, we extend the horizon to understand the effects of major institutional and demographic changes between 2010 and 2050: the stabilization of the size of LMIs in the two regions and the substantial start of the aging process in the US.

This paper relates to the debate over the role of institutions in the historical rise in the EU15–US unemployment gap. There is much empirical controversy regarding this question. On the one hand, Nickell et al. (Reference Nickell, Nunziata and Ochel2005) emphasize the role of changes in LMIs to explain this gap, and also show that interactions between the average values of institutions and shocks do not improve our understanding of this gap. On the other hand, Blanchard and Wolfers (Reference Blanchard and Wolfers2000) argue that institutional changes are not central for the explanation of the stylized facts (European countries already enjoyed well-developed welfare systems before the rise in the gap), but it is rather the interaction between common shocks and different institutional levels. We contribute to this discussion. We first show that asymmetric LMI changes only, that is without aging and capital mobility, can reproduce a large part of the historical rise in the EU15–US unemployment gap. This is in line with Nickell et al. (Reference Nickell, Nunziata and Ochel2005). Second, we show that this result no longer holds when we add asymmetric aging to asymmetric institutional changes (keeping capital mobility unchanged). Third, we are able to restore and even improve upon the initial result when we allow for international capital mobility. This paper also relates to work that considers the general-equilibrium OLG approach to be the appropriate way of quantifying the international implications of demographic changes and, in particular, differential aging [for example, Fehr et al. (Reference Fehr, Jokisch and Kotlikoff2003), Börsch-Supan et al. (Reference Börsch-Supan, Ludwig and Winter2006), Attanasio et al. (Reference Attanasio, Kitao and Violante2007), and Krueger and Ludwig (Reference Krueger and Ludwig2007)]. One of the main findings in this literature is that capital mobility (largely induced by demographic differences) affects factor prices, macroeconomic variables, and the distribution of wealth. In the receiving country, capital inflows boost labor income (which enhances the welfare of young workers) and reduce capital returns (which harms the elderly). Labor markets are, however, assumed to be competitive, so that there is no effect on unemployment. To our knowledge, there are only two papers using general equilibrium models with OLG dynamics and labor-market frictions to consider demographic changes. Jaag et al. (Reference Jaag, Keuschnigg and Keuschnigg2010) analyze the effects of a pension reform in Austria and de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013) look at the effects of aging on unemployment. However, both use closed-economy models. This paper is closely related to de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013). The main difference is that we have two open economies with international capital mobility instead of one closed economy. This has important consequences. In de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013), aging stimulates savings and therefore capital accumulation. Real interest rates fall, which encourages job creation and reduces unemployment. In our work, the link between savings and capital accumulation is broken, and therefore so is that between aging and unemployment.

The remainder of this paper is organized as follows. Section 2 presents empirical evidence on asymmetric institutions and aging between the EU15 and the US, bilateral capital flows and the gap in the unemployment rate. In Section 3, we develop a simple, analytically tractable multi-country OLG model to highlight the qualitative effects of LMIs and demographic differences on capital flows and unemployment. We use these analytical results in the subsequent analysis to better understand the quantitative results. Section 4 describes the quantitative model and Section 5 sets out the calibration. In Section 6, we present the key simulation results, underlining the roles of institutions, demography, and capital flows in explaining the EU and US unemployment rates. Section 7 extends the horizon beyond 2010 and Section 8 concludes.

2. FACTS

The difference in EU15 and US unemployment performance over recent decades is well known. European unemployment was low during the 1960s but started to increase in the 1970s. It rose above the US level in the early 1980s and has remained higher ever since (see panel a in Figure 1).Footnote 2 The EU15–US unemployment gap mostly widened from 1960 onwards, rising from around −4% in 1960 to almost 5% in 1995 (panel b), but then declining to 1% in 2010.

Figure 1. EU15–US labor markets, demography, and net foreign asset position. Panel a, “Unemployment rate”: Unemployment rate of 25–54 year olds. 5-year smoothed average (e.g., 2005 = the 2003 to 2007 average). The data are from the OECD. Panel b, “UR gap”: Unemployment-rate gap. Calculated as the difference between the EU15 and US unemployment rates. A negative (resp. positive) number means that the EU15 unemployment rate is lower (higher) than that in the US. “NFA gap”: Net Foreign Assets gap. Calculated as the difference between US-owned assets (excluding financial derivatives) in the EU15 and EU15-owned assets (excluding financial derivatives) in the US, divided by US GDP. A positive sign (resp. negative) means that the US is a net creditor (debtor). The data are from the Bureau of Economic Activity. The figures are normalized to zero in 1960. No data are available before 1960. Panel c: Relative retirement- and unemployment-replacement rates. Calculated as the difference between EU15 and US replacement rates. A positive number indicates that EU institutions are more generous than their US counterparts. Panel d: The dependency ratio is the percentage of people aged 65+ years over people aged 25–64 years. The working-age population ratio is the percentage of people aged 25–64 years over people aged 25+ years. The data are from the United Nations.

A number of other aspects of the economy have also evolved in an asymmetric fashion in recent decades. First, LMIs, depicted in panel c of Figure 1 and measured by unemployment and retirement replacement rates, have always been stronger in the EU15 than in the US. Moreover, this gap grew between 1960 and 2005. According to OECD data including recent reforms, the retirement replacement rates are currently falling. Second, while the old-age dependency ratio in the US was almost constant between 1960 and 2010, it increased from 15% to 25% in Europe, as shown in panel d of Figure 1. Similarly, the working-age ratio fell by 7 pp in the EU15 over the same period, but by only 2 pp in the US. Third, the capital flows from the EU15 to the US (panel b) from 1960 onwards reveal a deterioration in the US NFA position with Europe.

There are, therefore, some striking similarities between the movements in relative LMI and the unemployment-rate gap, with a steady rise starting in 1960 followed more recently by a small drop. At the same time, we also observe a parallel between relative aging and the direction of net capital flows. Last, the unemployment-rate gap and capital flows might themselves be related [see, for instance, Head and Smits (Reference Head and Smits2004)]. To examine all of these possible links, we first develop a simple analytically tractable OLG model. We then adopt a numerical general-equilibrium model to quantify the international implications of LMIs and demographic changes on capital flows and labor-market outcomes in both a historical and forward-looking perspective.

An alternative way of looking at the different relationships between aging, LMIs, capital flows, and unemployment over the 1960–2010 period is via econometrics. One advantage of the econometric approach is that it can statistically assess whether the storyline suggested above is valid. The difficulty here would certainly be to appropriately and convincingly identify the many different causal relationships. By way of contrast, a dynamic general-equilibrium model provides a framework in which the different interactions are generated endogenously and dynamically. Moreover, our model with search and matching frictions also has the advantage of providing a theoretical foundation for the functioning of labor markets. Last, the OLG framework calibrated on official LMIs and demographic data can incorporate various types of institutions (benefits for the unemployed, retired, and early retired) and detailed demographic information reproducing, for example, a time-varying age pyramid over a given time period.

3. A STYLIZED MODEL

Section 2 underlined that between 1960 and 2010, (i) LMIs, measured by unemployment and pension replacement rates, were more developed in the EU15 than in the US and (ii) the aging process accelerated more in the EU15 than in the US. At the same time, capital migrated from Europe to the United States, and the EU–US unemployment gap rose (at least until 1995).

This section aims to provide qualitative insights into the combined effects of these asymmetric developments in LMIs and population aging. To do so, we construct a stylized two-period, two-country OLG model that can be solved analytically. Population aging is introduced via changes in the survival probability or fertility rate, and LMIs are measured by the generosity of public unemployment and pension benefits. The setup is a search and matching model with exogenous job destruction with or without capital mobility. We first focus on a closed-economy model, i.e., no capital mobility, and then consider the consequences of perfect capital mobility in a two-country model.

3.1. Closed Economies

Demography and labor flows

Each generation lives for up to two periods. The size of the new generation increases at a rate of f; the size of the old generation is a fraction θ of that of the corresponding young generation, where 0 < θ < 1 is the survival probability. The size of the total population scaled by the size of the new generation is thus

$$\begin{equation*}

\frac{N_t}{N^y_t} = 1+\theta \phi ,

\end{equation*}$$

$$\begin{equation*}

\frac{N_t}{N^y_t} = 1+\theta \phi ,

\end{equation*}$$

where

$\phi \equiv \frac{1}{1+f}\le 1.$

A larger survival probability or lower fertility rate both imply a higher old-age dependency ratio. Young households supply one unit of labor and use their labor income to pay taxes, consume, and save. In period two, the surviving households retire and consume their savings and pension benefits.

$\phi \equiv \frac{1}{1+f}\le 1.$

A larger survival probability or lower fertility rate both imply a higher old-age dependency ratio. Young households supply one unit of labor and use their labor income to pay taxes, consume, and save. In period two, the surviving households retire and consume their savings and pension benefits.

Frictions on the labor market generate imperfections and unemployment. Employment is determined by a standard matching function. In this two-period setup where only the young generation participates in the labor market, employment is equal to the number of matches:

$$\begin{equation}

n_t = \bar{m}\,v_t^\nu ,\hspace{14.22636pt}\mbox{where}\;\bar{m}> 0,\;0\le \nu \le 1.

\end{equation}$$

$$\begin{equation}

n_t = \bar{m}\,v_t^\nu ,\hspace{14.22636pt}\mbox{where}\;\bar{m}> 0,\;0\le \nu \le 1.

\end{equation}$$

Here, n

t

is the employment rate,

$\bar{m}$

is a matching-efficiency parameter, vt

is the number of vacancies per worker at the beginning of period t, and ν is the elasticity of matches with respect to vacancies.

$\bar{m}$

is a matching-efficiency parameter, vt

is the number of vacancies per worker at the beginning of period t, and ν is the elasticity of matches with respect to vacancies.

Households

We assume the following lifetime expected-utility function:

$$\begin{equation}

\ln c^y_t + \beta \theta \ln c^o_{t+1},\hspace{14.22636pt}\mbox{where}\;0<\beta <1.

\end{equation}$$

$$\begin{equation}

\ln c^y_t + \beta \theta \ln c^o_{t+1},\hspace{14.22636pt}\mbox{where}\;0<\beta <1.

\end{equation}$$

Here, cy t and co t + 1 stand for the consumption of the young and the old, respectively. The utility of future consumption is weighted by the subjective discount factor β.Footnote 3 The employed member of a young household earns a wage of w t , and pays taxes at the rates of τ r t to finance retirement benefits and τ u t to finance (untaxed) unemployment benefits of bu t . In the second period, all surviving households retire and receive (untaxed) pension benefits br t + 1. If we further assume that households have access to perfect annuity markets, optimal consumption results from the maximization of expected lifetime utility (2) subject to the employment constraint (1) and the following intertemporal budget constraint:

$$\begin{equation}

c^y_t+\theta \,\frac{c^o_{t+1}}{1+r_{t+1}} = \left(1-\tau ^r_t-\tau ^u_t\right) w_t n_t+ b^u_t(1-n_t)+\theta \,\frac{b^r_{t+1}}{1+r_{t+1}},

\end{equation}$$

$$\begin{equation}

c^y_t+\theta \,\frac{c^o_{t+1}}{1+r_{t+1}} = \left(1-\tau ^r_t-\tau ^u_t\right) w_t n_t+ b^u_t(1-n_t)+\theta \,\frac{b^r_{t+1}}{1+r_{t+1}},

\end{equation}$$

where r t + 1 is the real interest rate. The first-order condition, the Euler equation, is

$$\begin{equation}

c^o_{t+1} = \beta (1+r_{t+1})\;c^y_t.

\end{equation}$$

$$\begin{equation}

c^o_{t+1} = \beta (1+r_{t+1})\;c^y_t.

\end{equation}$$

Combining the Euler equation and the budget constraint yields the following savings equation:

$$\begin{eqnarray}

s_t = \frac{\beta \,\theta }{1+\beta \,\theta }\left\lbrace \left(1-\tau ^r_t-\tau ^u_t\right)\,w_t\,n_t + b^u_t\,(1-n_t)-\,\frac{b^r_{t+1}}{\beta \,\left(1+r_{t+1}\right)}\right\rbrace ,

\end{eqnarray}$$

$$\begin{eqnarray}

s_t = \frac{\beta \,\theta }{1+\beta \,\theta }\left\lbrace \left(1-\tau ^r_t-\tau ^u_t\right)\,w_t\,n_t + b^u_t\,(1-n_t)-\,\frac{b^r_{t+1}}{\beta \,\left(1+r_{t+1}\right)}\right\rbrace ,

\end{eqnarray}$$

where s t stands for the savings per worker.

Government

The government balances its budget in every period and finances both the pay-as-you-go pension system and unemployment benefits via payroll taxes, which implies

$$\begin{equation}

b^u_t\,(1-n_t) = \tau ^u_{t}\,n_{t}\;w_{t},\\

\end{equation}$$

$$\begin{equation}

b^u_t\,(1-n_t) = \tau ^u_{t}\,n_{t}\;w_{t},\\

\end{equation}$$

$$\begin{equation}

b^r_{t+1} = \frac{\tau ^r_{t+1}}{\theta \phi }\,n_{t+1}\;w_{t+1}.

\end{equation}$$

$$\begin{equation}

b^r_{t+1} = \frac{\tau ^r_{t+1}}{\theta \phi }\,n_{t+1}\;w_{t+1}.

\end{equation}$$

We assume a constant τ r t = τ r as well as a constant net unemployment benefit rate of ρ u , i.e., bu t = ρ u (1 − τ r t − τ u t ) wt . The values of τ r and ρ u measure the generosity of public pension and unemployment benefits.

Firms

Firms have a Cobb–Douglas production technology with 0 < α < 1. They rent capital k

t

and labor n

t

from the households and face a cost for each posted vacancy. In line with the existing literature, we assume that the cost per vacancy is proportional to total factor productivity [see for instance, Pissarides (Reference Pissarides2000), Chap. 3]. As our focus is on demographics rather than technological progress, we will assume that total factor productivity is constant. The cost per vacancy is thus constant too and will be denoted by

$\mathsf{a} >0$

.

$\mathsf{a} >0$

.

Capital fully depreciates in one period. The optimal capital k t and (per worker) number of vacancies vt are the outcome of the following profit-maximization program:

$$\begin{equation*}

\max _{k_t,\,n_t,\,v_t}\Pi _t\;=\;k_t^\alpha \,n_t^{1-\alpha } -\left(1+r_t\right)\,k_t-w_t\,n_t-\mathsf{a}\,v_t,

\end{equation*}$$

$$\begin{equation*}

\max _{k_t,\,n_t,\,v_t}\Pi _t\;=\;k_t^\alpha \,n_t^{1-\alpha } -\left(1+r_t\right)\,k_t-w_t\,n_t-\mathsf{a}\,v_t,

\end{equation*}$$

subject to n t = q t vt , where q t is the probability of filling a vacancy. The first-order conditions are the following:

$$\begin{equation}

\alpha \;\widetilde{k}_t^{\alpha -1} = 1+r_t,\\

\end{equation}$$

$$\begin{equation}

\alpha \;\widetilde{k}_t^{\alpha -1} = 1+r_t,\\

\end{equation}$$

$$\begin{equation}

\frac{\mathsf{a}}{q_t} = (1-\alpha )\;\widetilde{k}_t^\alpha -w_t,

\end{equation}$$

$$\begin{equation}

\frac{\mathsf{a}}{q_t} = (1-\alpha )\;\widetilde{k}_t^\alpha -w_t,

\end{equation}$$

where

$\widetilde{k}_t={k_t}/{n_t}$

is the capital stock per employed worker and

$\widetilde{k}_t={k_t}/{n_t}$

is the capital stock per employed worker and

$$\begin{equation}

q_t=\frac{n_t}{v_t}={\bar{m}}^{1/\nu }\,{n_t}^{(\nu -1)/\nu }

\end{equation}$$

$$\begin{equation}

q_t=\frac{n_t}{v_t}={\bar{m}}^{1/\nu }\,{n_t}^{(\nu -1)/\nu }

\end{equation}$$

is obtained from the employment constraint (1).

Wages and employment

Wages are renegotiated in every period and determined by a standard Nash bargain as follows:

$$\begin{equation*}

\max _{w_t} \left((1-\tau ^u_t-\tau ^r)\;w_t-b^u_t\right)^{\eta }\left((1-\alpha )\,\widetilde{k}_t^\alpha -w_t\right)^{1-\eta },\hspace{14.22636pt}\mbox{where}\;0\le \eta \le 1.

\end{equation*}$$

$$\begin{equation*}

\max _{w_t} \left((1-\tau ^u_t-\tau ^r)\;w_t-b^u_t\right)^{\eta }\left((1-\alpha )\,\widetilde{k}_t^\alpha -w_t\right)^{1-\eta },\hspace{14.22636pt}\mbox{where}\;0\le \eta \le 1.

\end{equation*}$$

The parameter η measures the worker’s bargaining power. From (6), the bargained wage is easily shown to be a fraction of marginal labor productivity as shown below:Footnote 4

$$\begin{equation}

w_t=\frac{\eta }{1-\rho ^u\,(1-\eta )}\;\,(1-\alpha )\,\widetilde{k_t}^{\alpha }.

\end{equation}$$

$$\begin{equation}

w_t=\frac{\eta }{1-\rho ^u\,(1-\eta )}\;\,(1-\alpha )\,\widetilde{k_t}^{\alpha }.

\end{equation}$$

The employment rate is then obtained by combining (9) with (11) as follows:

$$\begin{equation}

n_t = \lambda \;\widetilde{k_t}^{\frac{\alpha \;\nu }{1-\nu }},\\

\end{equation}$$

$$\begin{equation}

n_t = \lambda \;\widetilde{k_t}^{\frac{\alpha \;\nu }{1-\nu }},\\

\end{equation}$$

$$\begin{equation}

\mbox{where}\hspace{78.24507pt} \lambda \equiv \left((1-\alpha )\;\frac{\bar{m}^{\frac{1}{\nu }}}{\mathsf{a}} \;\frac{(1-\eta )(1-\rho ^u)}{(1-\rho ^u(1-\eta ))}\right)^{\frac{\nu }{1-\nu }}\,>\,0.

\end{equation}$$

$$\begin{equation}

\mbox{where}\hspace{78.24507pt} \lambda \equiv \left((1-\alpha )\;\frac{\bar{m}^{\frac{1}{\nu }}}{\mathsf{a}} \;\frac{(1-\eta )(1-\rho ^u)}{(1-\rho ^u(1-\eta ))}\right)^{\frac{\nu }{1-\nu }}\,>\,0.

\end{equation}$$

λ is a negative function of the unemployment benefit rate ρ u and depends neither on life expectancy θ nor on pension benefits τ r .

Capital accumulation

It is easily shown, by combining equations (9), (11), and (12), that profits are zero. Capital accumulation is then fully determined by the young household’s savings. In per worker terms, this leads to the following:

$$\begin{eqnarray}

\widetilde{k}_{t+1} &=& {\phi }\;\frac{s_t}{n_{t+1}},\nonumber \\

&=& \frac{\beta \theta {\phi }}{1+\beta \theta }\,(1-\tau ^{r})\,w_t\,\frac{n_t}{n_{t+1}} -\frac{\tau ^{r}}{1+\beta \theta }\,\frac{w_{t+1}}{1+r_{t+1}}.

\end{eqnarray}$$

$$\begin{eqnarray}

\widetilde{k}_{t+1} &=& {\phi }\;\frac{s_t}{n_{t+1}},\nonumber \\

&=& \frac{\beta \theta {\phi }}{1+\beta \theta }\,(1-\tau ^{r})\,w_t\,\frac{n_t}{n_{t+1}} -\frac{\tau ^{r}}{1+\beta \theta }\,\frac{w_{t+1}}{1+r_{t+1}}.

\end{eqnarray}$$

Equation (14) is obtained by combining (5)–(7). We next use equations (8), (11), and (12) to substitute out r, w, and n. We end up with the following dynamic capital equation:

$$\begin{equation}

\widetilde{k}_{t+1} = \left(\sigma ^{{1-\nu }}\;\widetilde{k_{t}}^{{\alpha }}\right)^\frac{1}{1-\nu (1-\alpha )},\\

\end{equation}$$

$$\begin{equation}

\widetilde{k}_{t+1} = \left(\sigma ^{{1-\nu }}\;\widetilde{k_{t}}^{{\alpha }}\right)^\frac{1}{1-\nu (1-\alpha )},\\

\end{equation}$$

$$\begin{equation}

\mbox{where}\hspace{42.67912pt} \sigma \equiv {\frac{\beta \theta {\phi }\;\eta \;(1-\alpha )\;(1-\tau ^r)}{(1+\beta \theta )\left[1-\rho ^u(1-\eta )\right]\;+\;\eta \;\tau ^r\;(1-\alpha )/\alpha }} \;>0.

\end{equation}$$

$$\begin{equation}

\mbox{where}\hspace{42.67912pt} \sigma \equiv {\frac{\beta \theta {\phi }\;\eta \;(1-\alpha )\;(1-\tau ^r)}{(1+\beta \theta )\left[1-\rho ^u(1-\eta )\right]\;+\;\eta \;\tau ^r\;(1-\alpha )/\alpha }} \;>0.

\end{equation}$$

As α < 1 − ν(1 − α), equation (15) is concave in

$\widetilde{k}_t$

. Moreover, σ is increasing in θ (life expectancy), ϕ (which is negatively related to fertility), and ρ

u

(unemployment benefits, which play the role of a reservation wage and increase the bargained wage and savings); it is decreasing in τ

r

(the generosity of the public pension scheme).

$\widetilde{k}_t$

. Moreover, σ is increasing in θ (life expectancy), ϕ (which is negatively related to fertility), and ρ

u

(unemployment benefits, which play the role of a reservation wage and increase the bargained wage and savings); it is decreasing in τ

r

(the generosity of the public pension scheme).

Population aging, labor-market institutions, and unemployment in the steady state

The concavity of equation (15) defines a non-trivial steady state for

$\widetilde{k}_t$

. Combining equation (15) with equation (12) yields the employment steady state of

$\widetilde{k}_t$

. Combining equation (15) with equation (12) yields the employment steady state of

$$\begin{equation}

{n}=\lambda \;\sigma ^\frac{\alpha \nu }{(1-\alpha )(1-\nu )}.

\end{equation}$$

$$\begin{equation}

{n}=\lambda \;\sigma ^\frac{\alpha \nu }{(1-\alpha )(1-\nu )}.

\end{equation}$$

Using u = 1 − n ≈ −log n if the unemployment rate is not too far from zero, we obtain the following from equation (17):Footnote 5

\begin{equation}

u \cong - \log \lambda -\frac{\alpha \nu }{(1-\alpha )(1-\nu )}\log \sigma .

\end{equation}

\begin{equation}

u \cong - \log \lambda -\frac{\alpha \nu }{(1-\alpha )(1-\nu )}\log \sigma .

\end{equation}

Proposition 1. In a closed economy, the steady-state unemployment rate is a negative function of life expectancy θ, and a positive function of fertility (via the parameter ϕ), and the pension replacement rate τ r . For plausible values of the parameters (for instance, when the bargaining power of the workers is not too close to zero), the steady-state unemployment rate is a positive function of the unemployment benefit rate ρ u .

Proof. We can see that ∂λ/∂θ = 0 from equation (13) and ∂σ/∂θ > 0 from equation (16). Then, ∂u/∂θ < 0 from equation (18). For fertility (or rather its inverse ϕ), we have ∂λ/∂ϕ = 0 and ∂σ/∂ϕ > 0. Similarly, ∂λ/∂τ r = 0 from equation (13) and ∂σ/∂τ r < 0 from equation (16), which gives ∂u/∂τ r > 0 from equation (18). As ∂λ/∂ρ u < 0 from equation (13) and ∂σ/∂ρ u > 0 from equation (16), the sign of ∂u/∂ρ u is ambiguous. However, from equations (13), (16), and (18), we can easily show that

$$\begin{equation*}

\frac{\partial u}{\partial \rho ^u}>0 \;\Longleftrightarrow \; \frac{\eta }{1-\eta }>\frac{\alpha }{1-\alpha }\;\;\underbrace{\frac{(1-\rho ^u)\;\alpha \;(1+\theta \;\beta )}{\alpha (1+\theta \;\beta )(1-\rho ^u(1-\eta ))\;+\;\eta \;\tau ^r\;(1-\alpha )}}_{<1}.

\end{equation*}$$

$$\begin{equation*}

\frac{\partial u}{\partial \rho ^u}>0 \;\Longleftrightarrow \; \frac{\eta }{1-\eta }>\frac{\alpha }{1-\alpha }\;\;\underbrace{\frac{(1-\rho ^u)\;\alpha \;(1+\theta \;\beta )}{\alpha (1+\theta \;\beta )(1-\rho ^u(1-\eta ))\;+\;\eta \;\tau ^r\;(1-\alpha )}}_{<1}.

\end{equation*}$$

We observe that only implausible parameter values, for example, a very low value of worker bargaining power η, may violate the right-hand side condition. □

Higher life expectancy and lower fertility increase the amount of capital per worker: the first via its effect on savings and the second directly via the different size of successive generations. In both cases, higher capital stock per worker reduces unemployment. By the reverse argument, pensions have a negative effect on capital accumulation and, therefore, increase unemployment. The effect of unemployment compensation is a priori ambiguous, as on the one hand, it increases the reservation wage and creates unemployment and on the other hand, it increases income, which stimulates capital accumulation and reduces unemployment. A sufficient condition for the first effect to dominate is that worker bargaining power η is higher than the elasticity of output to capital α, which is a realistic restriction.

It is also worth noting that changes in life expectancy and fertility that produce the same change in the old-age dependency ratio have different quantitative effects on the capital stock per worker, and hence on unemployment. The effect on the capital stock per worker is larger in the case of a fertility change. It can also be shown that the difference in the effects of life expectancy and fertility on unemployment is a negative function of the unemployment benefit rate ρ u , the pension replacement rate τ r , and bargaining power η.

3.2. Perfect Capital Mobility

We consider two countries A and B with the same preferences β and the same production technology α. Labor-market frictions, as measured by the parameters

$\bar{m},\nu$

, and a, are also assumed to be identical, as is worker bargaining power η. The two countries differ only by the survival probability of the young generation (θ), the fertility rate (f or equivalently ϕ), and the generosity of unemployment and pension benefits (ρ

u

and τ

r

). If we furthermore assume perfect capital mobility, capital from the low-interest-rate region flows to the high-interest-rate region until interest rates are equalized (rA

t

= rB

t

= r*

t

), which implies the following from equation (8):

$\bar{m},\nu$

, and a, are also assumed to be identical, as is worker bargaining power η. The two countries differ only by the survival probability of the young generation (θ), the fertility rate (f or equivalently ϕ), and the generosity of unemployment and pension benefits (ρ

u

and τ

r

). If we furthermore assume perfect capital mobility, capital from the low-interest-rate region flows to the high-interest-rate region until interest rates are equalized (rA

t

= rB

t

= r*

t

), which implies the following from equation (8):

$$\begin{equation*}

\widetilde{k}^{A}_t=\widetilde{k}^{B}_t=\widetilde{k}^{*}_t.

\end{equation*}$$

$$\begin{equation*}

\widetilde{k}^{A}_t=\widetilde{k}^{B}_t=\widetilde{k}^{*}_t.

\end{equation*}$$

Equation (12) becomes

$$\begin{equation}

n^A_t = \lambda ^A\;\left(\widetilde{k}^*_t\right)^{\frac{\alpha \;\nu }{1-\nu }},\\

\end{equation}$$

$$\begin{equation}

n^A_t = \lambda ^A\;\left(\widetilde{k}^*_t\right)^{\frac{\alpha \;\nu }{1-\nu }},\\

\end{equation}$$

$$\begin{equation}

n^B_t = \lambda ^B\;\left(\widetilde{k}^*_t\right)^{\frac{\alpha \;\nu }{1-\nu }},

\end{equation}$$

$$\begin{equation}

n^B_t = \lambda ^B\;\left(\widetilde{k}^*_t\right)^{\frac{\alpha \;\nu }{1-\nu }},

\end{equation}$$

where λ A and λ B only differ in the unemployment-benefit parameters, respectively ρ u, A and ρ u, B . Using the same approximation as before (u = 1 − n ≈ −log n), if the unemployment rate is not too far from zero, we obtain from equations (19) and (20):

$$\begin{equation}

\Delta u_t^*= u_t^B- u_t^A\cong \frac{\nu }{1-\nu }\;\left(\log \left(\frac{1-\rho ^{u,A}}{1-\rho ^{u,A}(1-\eta )}\right) -\log \left(\frac{1-\rho ^{u,B}}{1-\rho ^{u,B}(1-\eta )}\right)\!\right)\!,

\end{equation}$$

$$\begin{equation}

\Delta u_t^*= u_t^B- u_t^A\cong \frac{\nu }{1-\nu }\;\left(\log \left(\frac{1-\rho ^{u,A}}{1-\rho ^{u,A}(1-\eta )}\right) -\log \left(\frac{1-\rho ^{u,B}}{1-\rho ^{u,B}(1-\eta )}\right)\!\right)\!,

\end{equation}$$

so that the unemployment gap no longer depends on differences in saving behavior but only on differences in reservation wages, and therefore job creation behavior.

Proposition 2. In open economies with perfect capital mobility, differences in life expectancy, fertility, and pension benefits no longer affect the unemployment gap. The unemployment gap is uniquely and unambiguously determined by differences in the unemployment-replacement rate.

Proof. Straightforward from equation (21). □

The corollary of this proposition is that ignoring the effects of population aging and the pension system when considering the determinants of equilibrium unemployment may be an acceptable approximation if, and only if, there is perfect capital mobility. The reason is that savings are then exported, which sterilizes this channel.

3.3. Discussion

The key mechanisms behind the above results are (i) the effects of life expectancy and fertility on the capital-labor ratio (equations (15) and (16)), and hence labor productivity, and (ii) the effect of labor productivity on job creation (equations (9) and (11)) and equilibrium unemployment. In this stylized model, the job-creation effect works solely via labor demand. With higher labor productivity, the value of a job increases and firms can afford to post more vacancies, even though the probability of filling a vacancy is lower. The final outcome is lower unemployment and a tighter labor market. The specification of vacancy costs of course plays a crucial role. We have adopted the most common representation, although it is now well understood that this fails to account for the volatility of job creation over the business cycle [the so-called Shimer (Reference Shimer2005), puzzle]. In this context, Pissarides (Reference Pissarides2009), for example, argues in favor of a slightly more general specification including a fixed sunk cost per filled vacancy. As the focus here is not on cyclical properties, we can safely neglect these refinements. It may be worth noting that in our stylized model, a cost per vacancy that is proportional to the wage rather than constant would render the equilibrium unemployment rate insensitive to labor productivity (see again equations (9) and (12)), so that higher life expectancy would leave equilibrium employment unchanged. This specification is however rather counter-intuitive, as it would for instance exacerbate the difficulty in accounting for the cyclical volatility of the job-creation rate. The result is also not robust and disappears with a fixed sunk cost à la Pissarides. Furthermore, in our stylized model, all jobs are destroyed after one period. In a more general setup (like the one we will use in the next section), jobs last for a number of periods and the value of a job rises as the interest rate falls due to the capitalization effect. This also restores the link between life expectancy and equilibrium unemployment. We should also keep in mind that job creation may be affected by the supply channel. For instance, we have so far ignored search effort (see footnote 3). This channel would re-introduce the link between aging/pensions and the unemployment gap. Higher wages have a positive impact on participation rates and search behavior, which increases the probability of filling a vacancy and the equilibrium employment rate. Last, in the open-economy case, our measure of the unemployment gap is affected by the log approximation (see footnote 5). The sections below aim to produce a quantitative evaluation of these effects. We build on this stylized model, with endogenous search effort for some working generations and without the unemployment approximation, and introduce more detail regarding the demographic structure (more generations, changing fertility, survival rates, and immigration) and the tax and benefit schemes. The model is calibrated to match EU15 and US data, and simulated numerically.

4. THE QUANTITATIVE MODEL

This section sets out a two-region general-equilibrium model with OLG dynamics. The representation of each region closely follows the closed-economy model of de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013). More precisely (and as in the stylized model of Section 3), we have frictions à la Diamond–Mortensen–Pissarides with (exogenous) job destruction and a matching function. There is perfect substitution between all workers, although labor productivity is age dependent. Perfect substitution means that there is one single matching function (all vacancies can be filled by any worker of any age). Age-directed search is not a credible strategy as the value of an unfilled vacancy is zero in equilibrium (the free-entry condition). As a result, a firm opening a vacancy targeted at young workers, for example, would eventually hire the first worker it meets, provided that the surplus to be shared is positive. Bargained wages reflect differences in work efficiency. From the modeling point of view, the main departure from de la Croix et al. (Reference de la Croix, Pierrard and Sneessens2013) is that the capital markets of the two regions are integrated. We calibrate regions i ∈ {A, B} to represent, respectively, the EU15 and the US. We present the model below. When possible, we omit the regional index i for notational convenience.

4.1. Demography

People live between the ages of 25 and 104 years. One time period is 5 years and we, therefore, have 16 coexisting generations, indexed by a ∈ {0, 1, . . .15}. The size of the new generations changes over time at an exogenous rate x t :

$$\begin{equation}

Z_{0,t}=(1+x_t)\,Z_{0,t-1},\;\;\;\forall t>0,

\end{equation}$$

$$\begin{equation}

Z_{0,t}=(1+x_t)\,Z_{0,t-1},\;\;\;\forall t>0,

\end{equation}$$

where x t includes both fertility and migration shocks at age zero. The size of the subsequent generations is determined by the cumulative survival probabilities 0 < θ a, t + a < 1 and migration flows X a, t + a :

$$\begin{equation}

Z_{a,t+a}=\theta _{a,t+a}\,Z_{0,t}+ X_{a, t+a},\;\;\;\;\forall a\in \lbrace 1,2,...15\rbrace .

\end{equation}$$

$$\begin{equation}

Z_{a,t+a}=\theta _{a,t+a}\,Z_{0,t}+ X_{a, t+a},\;\;\;\;\forall a\in \lbrace 1,2,...15\rbrace .

\end{equation}$$

The total (adult) population at time t is Zt = ∑15 a = 0 Z a, t . Demographic growth and the survival-probability and migration-flow vectors can vary over time. These changes are assumed to be exogenous.Footnote 6

We assume a mandatory retirement age of 65 years, so that all people older than 64 years (generations 8 ⩽ a ⩽ 15) are inactive. We, therefore, define the population of working age as

$$\begin{equation}

P_{a,t+a}=z_{a,t+a}\,Z_{a,t+a},

\end{equation}$$

$$\begin{equation}

P_{a,t+a}=z_{a,t+a}\,Z_{a,t+a},

\end{equation}$$

where z a, t + a = 1 for 0 ⩽ a ⩽ 7 and zero otherwise. We further assume that the participation rate between the ages of 25 and 54 years is exogenous and normalized to unity. Between ages 55 and 64 years, workers can choose to retire early. People of working age are thus either employed (N), unemployed (U), or in an early-retirement scheme (E) as follows:

$$\begin{eqnarray}

P_{a,t} &=& N_{a,t}+U_{a,t}+E_{a,t},\nonumber \\

&=& \Big [n_{a,t}+u_{a,t}+e_{a,t}\Big ]\,P_{a,t},\hspace{31.2982pt} 0\,\le \,a\,\le \,7 \, \nonumber \\

\Leftrightarrow \hspace{28.45274pt} 1 &=& n_{a,t}+u_{a,t}+e_{a,t},

\end{eqnarray}$$

$$\begin{eqnarray}

P_{a,t} &=& N_{a,t}+U_{a,t}+E_{a,t},\nonumber \\

&=& \Big [n_{a,t}+u_{a,t}+e_{a,t}\Big ]\,P_{a,t},\hspace{31.2982pt} 0\,\le \,a\,\le \,7 \, \nonumber \\

\Leftrightarrow \hspace{28.45274pt} 1 &=& n_{a,t}+u_{a,t}+e_{a,t},

\end{eqnarray}$$

where lower case letters denote the proportion of individuals in each status and with e a, t = 0 for a < 6. For later use, we also define λ a, t as the fraction of people who choose to retire early and leave the labor market at age a. We therefore have the following relationships:

$$\begin{eqnarray*}

e_{a,t} &=& \lambda _{a,t}\;=\;0\;\;\;\;\;\forall a\in \lbrace 1,2,...5\rbrace ,\nonumber \\

e_{6,t} &=& \lambda _{6,t},\\

e_{7,t} &=& \lambda _{6,t-1}+\lambda _{7,t}\,(1-\lambda _{6,t-1}).\nonumber

\end{eqnarray*}$$

$$\begin{eqnarray*}

e_{a,t} &=& \lambda _{a,t}\;=\;0\;\;\;\;\;\forall a\in \lbrace 1,2,...5\rbrace ,\nonumber \\

e_{6,t} &=& \lambda _{6,t},\\

e_{7,t} &=& \lambda _{6,t-1}+\lambda _{7,t}\,(1-\lambda _{6,t-1}).\nonumber

\end{eqnarray*}$$

4.2. Labor-Market Flows

We assume a constant returns to scale matching function as follows:

$$\begin{equation}

M_{t}=M(V_{t}, \Omega _{t}),

\end{equation}$$

$$\begin{equation}

M_{t}=M(V_{t}, \Omega _{t}),

\end{equation}$$

where V t and Ω t stand, respectively, for the total number of vacancies and job seekers at the beginning of period t, with

$$\begin{equation}

\Omega _t = P_{0,t} + \sum _{a=1}^{7}\;[u_{a-1,t-1}+\chi \,n_{a-1,t-1}]\,(1-\lambda _{a,t})\,P_{a,t}.

\end{equation}$$

$$\begin{equation}

\Omega _t = P_{0,t} + \sum _{a=1}^{7}\;[u_{a-1,t-1}+\chi \,n_{a-1,t-1}]\,(1-\lambda _{a,t})\,P_{a,t}.

\end{equation}$$

At the beginning of time t, all new entrants P 0, t are job seekers. Job seekers also represent the combination of past unemployment and new job separations. These job separations are determined by an exogenous job-destruction rate χ. The parameters λ a, t introduce the effects of early retirement when possible.

The probabilities of finding a job and of filling a vacancy are

$$\begin{equation}

p_t=\frac{M_{t}}{\Omega _{t}} \hspace{28.45274pt}\mbox{and}\hspace{28.45274pt} q_{t}=\frac{M_{t}}{V_{t}}.

\end{equation}$$

$$\begin{equation}

p_t=\frac{M_{t}}{\Omega _{t}} \hspace{28.45274pt}\mbox{and}\hspace{28.45274pt} q_{t}=\frac{M_{t}}{V_{t}}.

\end{equation}$$

The law of motion of employment is therefore

$$\begin{equation}

\begin{array}{lll} n_{a,t}&=p_t,&\qquad \mbox{for}\;a=0\,;\\

&=(1-p_t)(1-\chi )\,n_{a-1,t-1}+p_t,&\qquad \mbox{for}\;1\le a \le 5\,;\\

&=(1-p_t)(1-\lambda _{a,t})\,(1-\chi )\,n_{a-1,t-1}+p_t(1-\lambda _{a,t}),&\qquad \mbox{for}\;a = 6\,;\\

&=(1-p_t)(1-\lambda _{a,t})\,(1-\chi )\,n_{a-1,t-1}&\qquad \mbox{for}\; a = 7.\\

&\quad +\,p_t(1-\lambda _{a,t})(1-\lambda _{a-1,t-1}),& \end{array}

\end{equation}$$

$$\begin{equation}

\begin{array}{lll} n_{a,t}&=p_t,&\qquad \mbox{for}\;a=0\,;\\

&=(1-p_t)(1-\chi )\,n_{a-1,t-1}+p_t,&\qquad \mbox{for}\;1\le a \le 5\,;\\

&=(1-p_t)(1-\lambda _{a,t})\,(1-\chi )\,n_{a-1,t-1}+p_t(1-\lambda _{a,t}),&\qquad \mbox{for}\;a = 6\,;\\

&=(1-p_t)(1-\lambda _{a,t})\,(1-\chi )\,n_{a-1,t-1}&\qquad \mbox{for}\; a = 7.\\

&\quad +\,p_t(1-\lambda _{a,t})(1-\lambda _{a-1,t-1}),& \end{array}

\end{equation}$$

The same equations can be written in terms of the probability of filling a vacancy, q t , by using p t = q t V t /Ω t . Total employment will then be

$$\begin{equation*}

N_t=\sum _{a=0}^{7}\,N_{a,t},\hspace{14.22636pt}\mbox{with}\;N_{a,t}=n_{a,t}\,P_{a,t}.

\end{equation*}$$

$$\begin{equation*}

N_t=\sum _{a=0}^{7}\,N_{a,t},\hspace{14.22636pt}\mbox{with}\;N_{a,t}=n_{a,t}\,P_{a,t}.

\end{equation*}$$

4.3. Households

Each individual belongs to a representative household, of which there is one for each age category. There is no aggregate uncertainty, and all households have perfect foresight. There is perfect insurance against the adverse effects of individual lifetime uncertainty. There are no intended bequests. The household’s choice variables are consumption and early retirement, subject to the lifetime budget constraint.

The optimization program of the representative household

We can write the objective function of the household (effectively one cohort) as follows:

$$\begin{eqnarray}

W_{t}^{H}&=&\max _{c_{a, t+a},\, \lambda _{6, t+6},\, \lambda _{7, t+7}}\;\sum _{a=0}^{15} \beta ^a\,\theta _{a,t+a} \Bigg \lbrace {\cal U}(c_{a, t+a}) - d^n\,n_{a,t+a}\,z_{a, t+a}\nonumber\\

&&+\, d^e_a\,\frac{\left(e_{a, t+a}\right)^{1-\kappa }}{1-\kappa }\,z_{a, t+a}\, \Bigg \rbrace \,Z_{0,t},

\end{eqnarray}$$

$$\begin{eqnarray}

W_{t}^{H}&=&\max _{c_{a, t+a},\, \lambda _{6, t+6},\, \lambda _{7, t+7}}\;\sum _{a=0}^{15} \beta ^a\,\theta _{a,t+a} \Bigg \lbrace {\cal U}(c_{a, t+a}) - d^n\,n_{a,t+a}\,z_{a, t+a}\nonumber\\

&&+\, d^e_a\,\frac{\left(e_{a, t+a}\right)^{1-\kappa }}{1-\kappa }\,z_{a, t+a}\, \Bigg \rbrace \,Z_{0,t},

\end{eqnarray}$$

where β is a subjective discount factor.Footnote 7 Instantaneous utility is separable in c, n, and e. The utility of per capita consumption is represented by a standard concave function (we shall use a logarithmic function), whereas the disutility of working is linear with d n ⩾ 0 being marginal disutility.Footnote 8 The function describing the extra utility from early retirement is concave, i.e., 0 < κ < 1. The employment n a, t + a and early-retirement e a, t + a rates are linked to λ a, t + a through equations (26) and (29).

The household’s flow budget constraint at time t + a takes the following form:

$$\begin{equation}

I_{a,t+a}+\frac{\theta _{a-1,t+a-1}}{\theta _{a,t+a}}\;[1+r^{*}_{t+a}({1-\tau ^k_{t+a}})]\cdot s_{a-1,t+a-1}={(1+\tau ^c_{t+a})c_{a,t+a}+s_{a,t+a}},

\end{equation}$$

$$\begin{equation}

I_{a,t+a}+\frac{\theta _{a-1,t+a-1}}{\theta _{a,t+a}}\;[1+r^{*}_{t+a}({1-\tau ^k_{t+a}})]\cdot s_{a-1,t+a-1}={(1+\tau ^c_{t+a})c_{a,t+a}+s_{a,t+a}},

\end{equation}$$

where I a, t + a includes labor income and various transfers as follows:

$$\begin{eqnarray*}

I_{a,t+a} &=& z_{a,t+a}\cdot \big [(1-\tau ^w_{t+a}) w_{a,t+a}\cdot n_{a,t+a}+b^u_{a,t+a}\cdot u_{a,t+a}+b^e_{a,t+a}\cdot e_{a,t+a}\big ]\nonumber\\

&& +\,(1-z_{a,t+a}) b^r_{a,t+a}.

\end{eqnarray*}$$

$$\begin{eqnarray*}

I_{a,t+a} &=& z_{a,t+a}\cdot \big [(1-\tau ^w_{t+a}) w_{a,t+a}\cdot n_{a,t+a}+b^u_{a,t+a}\cdot u_{a,t+a}+b^e_{a,t+a}\cdot e_{a,t+a}\big ]\nonumber\\

&& +\,(1-z_{a,t+a}) b^r_{a,t+a}.

\end{eqnarray*}$$

The wage and consumption tax rates are τ w t + a and τ c t + a , respectively; bu a, t + a , be a, t + a , br a, t + a are the replacement benefits received, respectively, by the unemployed, early retirees, and pensioners; s a, t + a is the financial wealth accumulated at time t + a in per-capita terms. This financial wealth is held in the form of either shares or physical capital. As there is perfect insurance against individual lifetime uncertainty (as if there were a perfect annuity market), the total return to savings is equal to one plus the risk-free international interest rate r* t + a , net of capital taxes τ k t + a , divided by the survival probability θ a, t /θ a − 1, t − 1.

Appendix A sets out the first-order conditions. For later use, we also note that the value of an additional job for a household of age a is as follows:

$$\begin{eqnarray}

\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\frac{\partial W^H_t}{\partial N_{a,t}} &=&\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\,\frac{1}{z_{a,t}\,Z_{a,t}}\; \frac{\partial W^H_t}{\partial n_{a,t}},\nonumber\\

&=&\sum _{j=0}^{7-a} \frac{\theta _{a+j,t+j}}{\theta _{a,t}}\;\beta ^j\; \frac{{\mathcal {U}}^\prime _{c_{a+j,t+j}}}{{\mathcal {U}}^\prime _{c_{a,t}}}\nonumber\\

&&\times\,\Bigg \lbrace \frac{(1-\tau ^w_{t+j})\,w_{a+j,t+j}-b^u_{a+j,t+j}}{(1+\tau ^c_{t+j})\,}\; -\frac{d^n}{{\mathcal {U}}^\prime _{c_{a+j,t+j}}} \Bigg \rbrace \; \frac{\partial n_{a+j,t+j}}{\partial n_{a,t}},\qquad

\end{eqnarray}$$

$$\begin{eqnarray}

\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\frac{\partial W^H_t}{\partial N_{a,t}} &=&\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\,\frac{1}{z_{a,t}\,Z_{a,t}}\; \frac{\partial W^H_t}{\partial n_{a,t}},\nonumber\\

&=&\sum _{j=0}^{7-a} \frac{\theta _{a+j,t+j}}{\theta _{a,t}}\;\beta ^j\; \frac{{\mathcal {U}}^\prime _{c_{a+j,t+j}}}{{\mathcal {U}}^\prime _{c_{a,t}}}\nonumber\\

&&\times\,\Bigg \lbrace \frac{(1-\tau ^w_{t+j})\,w_{a+j,t+j}-b^u_{a+j,t+j}}{(1+\tau ^c_{t+j})\,}\; -\frac{d^n}{{\mathcal {U}}^\prime _{c_{a+j,t+j}}} \Bigg \rbrace \; \frac{\partial n_{a+j,t+j}}{\partial n_{a,t}},\qquad

\end{eqnarray}$$

where ∂n a + j, t + j /∂n a, t can be obtained from equation (29).

4.4. Firms

There are two productive factors, labor and capital. Labor is measured in efficiency units. Efficiency may vary with age (due to experience) and across generations (via education).Footnote 9 We define total labor input as follows:

$$\begin{equation*}

H_t=\sum _{a=0}^7 h_{a,t}.N_{a,t},

\end{equation*}$$

$$\begin{equation*}

H_t=\sum _{a=0}^7 h_{a,t}.N_{a,t},

\end{equation*}$$

where the h a, t are age-specific human-capital parameters. We assume a constant returns to scale production function in labor and capital:

$$\begin{equation}

Y_t=A_t\,F(K_t, H_t),

\end{equation}$$

$$\begin{equation}

Y_t=A_t\,F(K_t, H_t),

\end{equation}$$

where A

t

stands for total factor productivity. Firms rent capital at a cost of vt

= r*

t

+ δ and pay a gross wage w

a, t

to workers of age a. We denote the employer wage tax by τ

f

t

. Firms also open vacancies at a cost per vacancy of

$\mathsf{a}$

. As the representative firm maximizes the discounted value of all the dividends (profits) distributed to its shareholders, its value function is as follows:

$\mathsf{a}$

. As the representative firm maximizes the discounted value of all the dividends (profits) distributed to its shareholders, its value function is as follows:

$$\begin{equation}

W_t^F=\max _{K_{t}, V_{t}} \Bigg \lbrace Y_t-v_t\,K_t-\sum _{a=0}^7\,(1+\tau ^f_{t})\,w_{a,t}\,N_{a,t}-\mathsf{a}\,V_{t}\,\Bigg \rbrace +(R^*_{t+1})^{-1}\,W_{t+1}^{F}

\end{equation}$$

$$\begin{equation}

W_t^F=\max _{K_{t}, V_{t}} \Bigg \lbrace Y_t-v_t\,K_t-\sum _{a=0}^7\,(1+\tau ^f_{t})\,w_{a,t}\,N_{a,t}-\mathsf{a}\,V_{t}\,\Bigg \rbrace +(R^*_{t+1})^{-1}\,W_{t+1}^{F}

\end{equation}$$

subject to equation (29) with p t = q t V t /Ω t and R* t ≡ 1 + r* t (1 − τ k t ).Footnote 10 Appendix A shows the first-order optimality conditions.

Finally, we also note that the value for a firm of an additional worker of age a is

$$\begin{equation}

\begin{array}{ll} \displaystyle\frac{\partial W^F_t}{\partial N_{a,t}} &=\displaystyle\frac{1}{z_{a,t}\,Z_{a,t}}\;\frac{\partial W^F_t}{\partial n_{a,t}}\\[16pt]

&=\displaystyle\sum _{j=0}^{7-a}\, \frac{\theta _{a+j,t+j}}{\theta _{a,t}}\;(R^*_{t,t+j})^{-1} (1-\lambda _{a+j-1,t+j-1})\,(1-\lambda _{a+j,t+j})\,(1-\chi )^j\,\\[16pt]

&\quad\times\big \lbrace h_{a+j,t+j}\,A_tF_{H_{t+j}} -\big(1+\tau ^f_{t+j}\big)\,w_{a+j,t+j} \big \rbrace , \end{array}

\end{equation}$$

$$\begin{equation}

\begin{array}{ll} \displaystyle\frac{\partial W^F_t}{\partial N_{a,t}} &=\displaystyle\frac{1}{z_{a,t}\,Z_{a,t}}\;\frac{\partial W^F_t}{\partial n_{a,t}}\\[16pt]

&=\displaystyle\sum _{j=0}^{7-a}\, \frac{\theta _{a+j,t+j}}{\theta _{a,t}}\;(R^*_{t,t+j})^{-1} (1-\lambda _{a+j-1,t+j-1})\,(1-\lambda _{a+j,t+j})\,(1-\chi )^j\,\\[16pt]

&\quad\times\big \lbrace h_{a+j,t+j}\,A_tF_{H_{t+j}} -\big(1+\tau ^f_{t+j}\big)\,w_{a+j,t+j} \big \rbrace , \end{array}

\end{equation}$$

where R* t, t + j is defined by R* t, t = 1 and R* t, t + j = ∏ j k = 1 R* t + k for j ⩾ 1.

4.5. Wages

Wages are renegotiated every period. They are determined by a standard Nash bargaining rule as follows:

$$\begin{equation}

\max _{w_{a,t}}\; \left(\frac{\partial W_{t}^{F}}{\partial N_{a,t}}\right)^{1-\eta } \,\left(\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\frac{\partial W_t^{H}}{\partial N_{a,t}}\right)^{\eta }\;,

\end{equation}$$

$$\begin{equation}

\max _{w_{a,t}}\; \left(\frac{\partial W_{t}^{F}}{\partial N_{a,t}}\right)^{1-\eta } \,\left(\frac{1}{{\mathcal {U}}^\prime _{c_{a,t}}}\;\frac{\partial W_t^{H}}{\partial N_{a,t}}\right)^{\eta }\;,

\end{equation}$$

where 0 ⩽ η ⩽ 1 is household bargaining power. Appendix A presents the first-order optimality condition.

4.6. Government

We assume that unemployment and (early or legal) retirement benefits are an exogenous fraction of the relevant gross wage, so that

$$\begin{equation}

\begin{array}{lc@{\qquad}l}b^u_{a,t}=\rho ^u_t\,w_{a,t}&\mbox{for}&0\,\le \, a\,\le 7,\\

b^e_{a,t}=\rho ^e_{a,t}\,w_{a,t}&\mbox{for}&6\,\le \, a\,\le 7,\\

\displaystyle b^r_{a,t}=\rho ^r_t\,\sum _{i=0}^3 \frac{w_{7-i,t}}{4}&\mbox{for}&8\,\le \, a\,\le 15, \end{array}

\end{equation}$$

$$\begin{equation}

\begin{array}{lc@{\qquad}l}b^u_{a,t}=\rho ^u_t\,w_{a,t}&\mbox{for}&0\,\le \, a\,\le 7,\\

b^e_{a,t}=\rho ^e_{a,t}\,w_{a,t}&\mbox{for}&6\,\le \, a\,\le 7,\\

\displaystyle b^r_{a,t}=\rho ^r_t\,\sum _{i=0}^3 \frac{w_{7-i,t}}{4}&\mbox{for}&8\,\le \, a\,\le 15, \end{array}

\end{equation}$$

where ρ u , ρ r , and ρ e represent the gross replacement rates for unemployment and mandatory and early retirement, respectively. The earnings-related component of retirement benefits is 10 years in France, the entire working period in Germany and 35 years in the US. For simplicity, we choose a similar specification in both regions i ∈ A, B, that is for the EU15 and the US, and calculate retirement benefits using the average wage of the last four working generations (20 years).Footnote 11 Total transfer expenditures are then:

$$\begin{equation}

T_t=\rho ^u_t\, \sum _{a=0}^{7} \,w_{a,t}\,u_{a,t}\,Z_{a,t} + \sum _{a=6}^{7} \, \rho ^e_{a,t}\,w_{a,t}\,e_{a,t}\,Z_{a,t} +\rho ^r_t\,\sum _{i=0}^3 \frac{w_{7-i,t}}{4}\,\sum _{a=8}^{15}\,Z_{a,t}.

\end{equation}$$

$$\begin{equation}

T_t=\rho ^u_t\, \sum _{a=0}^{7} \,w_{a,t}\,u_{a,t}\,Z_{a,t} + \sum _{a=6}^{7} \, \rho ^e_{a,t}\,w_{a,t}\,e_{a,t}\,Z_{a,t} +\rho ^r_t\,\sum _{i=0}^3 \frac{w_{7-i,t}}{4}\,\sum _{a=8}^{15}\,Z_{a,t}.

\end{equation}$$

Public consumption is assumed to be a fraction of output, net of vacancy costs, i.e.,

$$\begin{equation}

G_t=\bar{g}\,(Y_t-\mathsf{a}\, V_t).

\end{equation}$$

$$\begin{equation}

G_t=\bar{g}\,(Y_t-\mathsf{a}\, V_t).

\end{equation}$$

For convenience, there is no public debt and we assume that the government balances its budget in every (5-year) period via the consumption tax τ c t :

$$\begin{eqnarray}

&&\tau ^c_{t}C_t+(\tau ^w_t+\tau ^f_t)\bigg (\sum _{a}\omega _{a,t}n_{a,t}P_{a,t}\bigg )+\tau ^k_t\bigg (\sum _{a}\;r^*_t\;s_{a-1,t+a-1}\;Z_{a-1,t+a-1}\bigg )\nonumber\\

&&\quad=G_t+T_t,

\end{eqnarray}$$

$$\begin{eqnarray}

&&\tau ^c_{t}C_t+(\tau ^w_t+\tau ^f_t)\bigg (\sum _{a}\omega _{a,t}n_{a,t}P_{a,t}\bigg )+\tau ^k_t\bigg (\sum _{a}\;r^*_t\;s_{a-1,t+a-1}\;Z_{a-1,t+a-1}\bigg )\nonumber\\

&&\quad=G_t+T_t,

\end{eqnarray}$$

where aggregate consumption C t = ∑ a c a, t Z a, t . The tax effects of changes in the generosity of the welfare state are thus taken into account by endogenous movements in the consumption tax.Footnote 12

4.7. International Capital Markets

Let Q t denote the total financial value of firms at time t. In our deterministic setup, the return to equities must equal the market interest rate. In other words, the value of equities must be such that, for all t ⩾ 0:

$$\begin{equation}

\frac{Q_{t+1}+\Pi _{t+1}}{Q_{t}}=1+r^*_{t+1}.

\end{equation}$$

$$\begin{equation}

\frac{Q_{t+1}+\Pi _{t+1}}{Q_{t}}=1+r^*_{t+1}.

\end{equation}$$

where

$\Pi _t = Y_t -v_t\,K_t-\sum _{a=0}^7\,(1+\tau ^f_{t})\,w_{a,t}\,N_{a,t}-\mathsf{a}\,V_{t}$

. The left-hand side is the return of one unit of savings invested in equities, while the right-hand side is the return from investment in firm bonds.

$\Pi _t = Y_t -v_t\,K_t-\sum _{a=0}^7\,(1+\tau ^f_{t})\,w_{a,t}\,N_{a,t}-\mathsf{a}\,V_{t}$

. The left-hand side is the return of one unit of savings invested in equities, while the right-hand side is the return from investment in firm bonds.

The aggregate stocks of capital in the two regions are as follows:

$$\begin{equation}

K^A_{t+1}+Q^A_t+FA_t = \sum _{a=0}^{14}\,s^A_{a,t}\,Z^A_{a,t}, \\

\end{equation}$$

$$\begin{equation}

K^A_{t+1}+Q^A_t+FA_t = \sum _{a=0}^{14}\,s^A_{a,t}\,Z^A_{a,t}, \\

\end{equation}$$

$$\begin{equation}

K^B_{t+1}+Q^B_t-FA_t = \sum _{a=0}^{14}\,s^B_{a,t}\,Z^B_{a,t},

\end{equation}$$

$$\begin{equation}

K^B_{t+1}+Q^B_t-FA_t = \sum _{a=0}^{14}\,s^B_{a,t}\,Z^B_{a,t},

\end{equation}$$

where FAt ( ≡ FAA t ) denotes the NFA position of region A, and region B’s external wealth is FAB t = −FAt .

The current-account surplus of region A (or the net capital outflow from region A to region B) is given by the change in the NFA position of region A,

$$\begin{equation}

CA^A_{t}\equiv CA_{t}=FA_{t+1}-FA_t.

\end{equation}$$

$$\begin{equation}

CA^A_{t}\equiv CA_{t}=FA_{t+1}-FA_t.

\end{equation}$$

As a result, region B’s current account is CAB t = −CAt .

4.8. Intertemporal General Equilibrium

The intertemporal general equilibrium is formally defined as follows:

Definition 1 Given the following exogenous processes and initial conditions:

-

− Demographic variables {x t } t = 0.. + ∞ (fertility), {θ a, t } a = 1..15 t = 0.. + ∞ (longevity), and {X a, t } a = 1..15 t = 0.. + ∞ (migration).

-

− Policy variables {ρ u t , ρ e a, t , ρ r t } a = 6, 7 t = 0.. + ∞ (replacement rates) and {τ k t , τ w t , τ f t } t = 0.. + ∞ (tax rates).

-

− Initial population {Z a, −1} a = 0..15, assets {s a, −1} a = 0..14, and capital stocks

$ \bar{K}^A_0+K^B_0 \le \sum _{a=0}^{14} s^A_{a,-1}Z^A_{a,-1}+ \sum _{a=0}^{14} s^B_{a,-1}Z^B_{a,-1}$

.

$ \bar{K}^A_0+K^B_0 \le \sum _{a=0}^{14} s^A_{a,-1}Z^A_{a,-1}+ \sum _{a=0}^{14} s^B_{a,-1}Z^B_{a,-1}$

.

An intertemporal equilibrium with perfect foresight is such that

-

1. consumption {c a, t } a = 0..15 t = 0.. + ∞ and retirement decisions {λ a, t } a = 6, 7 t = 0.. + ∞ maximize household utility (30) subject to the budget constraint (31) and (26) and (29),

-

2. the capital input {K t } t = 0.. + ∞ and posted vacancies {V t } t = 0.. + ∞ maximize firms’ profits (34) subject to (28), (29), (33), and

$K_0=\bar{K}_0$

, -

3. the number of new hires {M t } t = 0.. + ∞, the probabilities of finding a job {p t } t = 0.. + ∞ and of filling a vacancy {q t } t = 0.. + ∞, and the employment rates {n a, t } a = 0..7 t = 0.. + ∞ satisfy the matching technology (26), (28), and (29),

-

4. total population {Z a, t } a = 0..15 t = 0.. + ∞, population of working age {P a, t } a = 0..7 t = 0.. + ∞, and number of job seekers {Ω t } t = 0.. + ∞ satisfy the population-dynamics equations (22), (23), (24), and (27),

-

5. unemployment {u a, t } a = 0..7 t = 0.. + ∞ is such that the population constraint (25) holds,

-

6. wages {w a, t } a = 0..7 t = 0.. + ∞ are negotiated following the Nash bargaining rule (36),

-

7. government benefits {bu a, t , be a, t , br a, t } a = 0..15 t = 0.. + ∞ follow the rules defined by (37), and government spending {G t } t = 0.. + ∞ follows (39),

-

8. consumption taxes {τ c t } t = 0.. + ∞ are set by the government to balance its budget (40),

-

9. stock-market prices {Q t } t = 0.. + ∞ satisfy the arbitrage condition (41),

-

10. and the international interest rate {r* t } t = 0.. + ∞ clears the world capital market, i.e., equations (42) and (43).

5. CALIBRATION

The model starts from an initial steady state in 1900 and reaches the final steady state in 2300. The model is solved with Dynare [see Adjemian et al. (Reference Adjemian, Bastani, Karamé, Juillard, Maih, Mi-houbi, Perendia, Ratto and Villemot2011) for details]. Our analysis focuses on the sub-period from 1960 to 2050 within the transition path.Footnote

13

These dynamics are driven by the exogenous demographic variables {θ

a, t

, x

t

, X

a, t

}

a = 1..15 and the exogenous LMI variables {ρ

u

t

, ρ

e

6, t

, ρ

e

7, t

, ρ

r

t

} in each region. Since we want to focus on the effects of changes in demographics and LMIs, we assume that the exogenous fiscal variables {τ

k

t

, τ

w

t

, τ

f

t

} and the exogenous productivity variables {A

t

, h

a, t

}

a = 0..7 are constant over time. Along with the exogenous parameters related to production and consumption

$\lbrace \delta ,\,\alpha ,\,\bar{g}\rbrace$

, preferences {β, κ, dn

, de

6, de

7}, and the labor market

$\lbrace \delta ,\,\alpha ,\,\bar{g}\rbrace$

, preferences {β, κ, dn

, de

6, de

7}, and the labor market

$\lbrace \mathsf{a},\,\nu ,\,\eta ,\,\chi \rbrace$

, these are calibrated to reflect the economic conditions of the EU15 (region A) and the US (region B) in 2005.Footnote

14

Table 1 provides an overview of the calibrated values, and we set out the whole calibration process in detail below.

$\lbrace \mathsf{a},\,\nu ,\,\eta ,\,\chi \rbrace$

, these are calibrated to reflect the economic conditions of the EU15 (region A) and the US (region B) in 2005.Footnote

14

Table 1 provides an overview of the calibrated values, and we set out the whole calibration process in detail below.

Table 1. Exogenous variable and parameter values

Notes: We do not show the exogenous demographic variables {θ a, t , x t , X a, t } a = 1..15 (the file with these inputs can be obtained upon request). We show the 2005 values for the labor-market institution variables {ρ u t , ρ e 6, t , ρ e 7, t , ρ r t } and Figure B.1 displays the full historical (and future) values. The fiscal and productivity variables are time invariant.

Demographic variables. In the EU15 (region A), we take the survival probabilities θ a, t from 1900 to 2100 from French data [Vallin and Meslé (Reference Vallin and Meslé2001)], as they are relatively similar across EU15 countries. By way of comparison, US death probabilities were quite different to those in EU countries until the 1990s, although these differences disappeared in the early 2000s.

After 2100, we hold the survival probabilities constant. We take the population by age classes Z a, t over the 1950–2050 period from the United Nations (2010). We calibrate x t to reproduce the evolution of the first generation Z 0, t and we calibrate X a, t to reproduce the evolution of the subsequent generations Z a, t , with a ∈ {1, 2, ..15}. We keep these changes constant before 1950 and after 2050. We apply a similar method to the US (region B), for which the survival-probability data come from the US Social Security Administration [Bell and Miller (Reference Bell and Miller2005)]. We take the population by age classes Z a, t over the 1950–2050 period from the United Nations (2010), and we extend this data to 2100 using projections from the US Census (2000). We calculate x t and X a, t as explained above. This calibration reproduces the historical data and projections of the EU15 and US population pyramids between 1950–2050 (for age classes 25–29 to 100–104). The last line of Table 2 shows, for example, that our model matches the EU15–US 25+ years population ratio in 2005.

Table 2. Data match given in the parameter settings

Notes: The data refer to 2005 and the numbers are in percentages. Ypc stands for GDP per capita net of vacancy costs, Pop for population aged 25+ years and both are normalized to 100 in the US.

According to these estimates, the population of the United States is on a rising trend over the second half of the 20th century and the first half of the 21st century, and will overtake Europe’s population soon after the middle of this century. In the EU15, the dependency ratio (the population aged over 64 years divided by the population aged 25–64 years) increased by 10 pp from 1960 until 2000 and will more than double between 2000 and 2050 to reach a level of about 50% , as illustrated in panel b of Figure 2. Over the whole 21st century, the dependency ratio of the United States is never higher than that in Europe, and only reaches a figure of 35% in 2050.

Figure 2. EU15–US labor market and demography. Panel a: Relative retirement and unemployment replacement rates. These are calculated as the difference between the EU15 and US replacement rates. A positive number indicates that EU institutions are more generous than their US counterparts. The data in the gray area are based on projections (see Section 5 and Appendix B for details). Panel b: The dependency ratio is the percentage of people aged 65+ years over people aged 25–64 years. The data are from the United Nations. 1960–2010 are historical data and the data in the gray area (2010–2050) are based on projections (medium scenario).

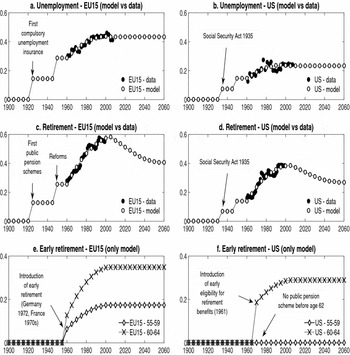

Labor-market institutions. The generosity of transfers, i.e., the replacement rates for unemployment and mandatory and early retirement, increased greatly over the 20th century, especially in the EU15. However, a number of reforms were implemented in the beginning of the 21st century that will, over the coming decades, progressively and partially reduce the current generosity of social transfers (see panel a of Figure 2 for a synthetic indicator). As a number of contributions have shown that LMIs are important determinants of the unemployment gap between the EU15 and the US, we want to use the full set of historical and expected values in the simulation exercises. Appendix B describes the calculation of these historical and expected values from the available data and known reforms. It is worth noting that our calibration of mandatory pension retirement rates produces a cost of public pensions of 12.75% of GDP in the EU15 and 6.23% in the US in 2005. These values are remarkably close to those reported by the OECD for 2005 [OECD (2009b), p.139] and the official estimate by the European Commission (2009) for the EU15.

Tax variables. We assume that all tax variables (except the consumption tax, which is used to balance the budget) are time invariant (see Section 6.3 and Appendix E for a discussion). The data on employers’ and employees’ wage taxes (τ f and τ w , respectively) come from the OECD Tax Database [OECD (2010b)]. In detail, we use the 2000–2009 average of the “Employer SSC” item to calculate τ f and that of the “Employee SSC” item for τ w . Employers’ wage taxes are 7.65% in the US and 25.64% in the EU15 (population weighted), whereas employees’ wage taxes are 7.65% in the US and 12.27% in the EU15. The data on capital taxation come from Bosca et al. (Reference Bosca, Garcia and Taguas2005). The capital tax rate τ k in 2001 is 24.45% in the EU15 (population-weighted average) and 34.7% in the US.Footnote 15

Productivity variables. To focus on the effects of demographic changes, we leave technological progress to one side and assume constant values of the TFP and age-specific human-capital parameters (A t and h a, t , respectively). TFP is set to 20 in the EU15 and 24.101 in the US to match the GDP per capita ratio between the EU15 and the US of 72.64% over the 2003–2007 period [see Table 2, data from the IMF (2009)]. Moreover, to reproduce the life-cycle profile of wages, we assume that worker productivity increases up to age 50 years and then slowly falls, as suggested by empirical work [see, for instance, Kotlikoff and Gokhale (Reference Kotlikoff and Gokhale1992), Johnson and Neumark (Reference Johnson and Neumark1996), and Aubert and Crépon (Reference Aubert and Crépon2003)].

Production and consumption parameters.

We assume a constant returns-to-scale Cobb–Douglas production function. The elasticity of output with respect to capital is set to α = 0.33. The depreciation rate of capital is set at 2.5% per quarter. These parameters are the same in each region. Government consumption is a constant fraction

$\bar{g}=$

19.37% of GDP in the EU15 and

$\bar{g}=$

19.37% of GDP in the EU15 and

$\bar{g}=$

14.49% in the US on average over the 2000–2005 period [WDI (2006)].

$\bar{g}=$

14.49% in the US on average over the 2000–2005 period [WDI (2006)].

Preference parameters. We assume identical preferences in both regions. Utility is logarithmic in consumption, so the income and substitution effects of a change in the interest rate cancel each other out. The parameter κ is set to 0.80, implying a Frisch elasticity of about 0.6, which is in line with estimated values [Den Haan and Kaltenbrunner (Reference Den Haan and Kaltenbrunner2009)]. As in Attanasio et al. (Reference Attanasio, Kitao and Violante2007), we fix the subjective rate of time preference at 0.77% per quarter (i.e., a quarterly discount factor of 0.9924) to obtain a capital-output ratio in 2005 of 2.50 annually in the United States. With these values, individual consumption rises over the life cycle, and savings are negative during the first two periods of life. Our calibration yields a real interest rate of 5.77% per annum in 2005 in line with the equilibrium interest rates in similar models [e.g., 6.6% in 2005 in Attanasio et al. (Reference Attanasio, Kitao and Violante2007) and 7.4% in Krueger and Ludwig (Reference Krueger and Ludwig2007)]. Although these interest rates may seem high at first sight, Attanasio et al. (Reference Attanasio, Kitao and Violante2007, p.165) note that they are still lower than the postwar real return on US equity (of about 8%). The labor-disutility parameter and the leisure (early retirement) parameters are set at d n = 0.25, de 6 = 0.1547, and de 7 = 0.1674 to reproduce the unemployment and activity rates calculated in the data (see below for details). Note that, in the model, activity rates for the age classes 55–59 years and 60–64 years are less than one and correspond to the share of the employed and unemployed in the age class, while the activity rates are one for the age groups 25–29 years to 50–54 years (see equation 25). It is worth noting that the value of d n also represents a marginal disutility of employment (divided by the marginal disutility of consumption) of 15% to 22% of wage income, depending on the generation, in both regions in 2005. Using German data, Frick et al. (Reference Frick, Grabka and Groh-Samberg2012) show that the average wage income advantage from home production is between 30% and 60%, depending on the method. However, using a GDP approach, Giannelli et al. (Reference Giannelli, Mangiavacchi and Piccoli2012) find that Germany has by far the highest value of home production in the EU15. Our values, therefore, seem acceptable in light of these results.

Labor-market parameters. A number of pieces of work have concluded that job-destruction rates differ in the US and the EU15. Bassanini and Marianna (Reference Bassanini and Marianna2009, Figure 4) use inter-industry data that are comparable across 11 OECD countries to suggest an average annual job destruction rate of about 13% in the US. This number is close to that in Klein et al. (Reference Klein, Schuh and Triest2003, p. 244), who report 10.2 jobs destroyed each year per 100 positions in US manufacturing over the 1974–1993 period. Moreover, quarterly job destruction rates over the 1990–2005 period range between 5% and 8% across US industries [excluding the Construction sector, which is characterized by a job destruction rate of 14% per quarter, Davis et al. (Reference Davis, Faberman, Haltiwanger, Jarmin and Miranda2010)]. In the EU15, Bassanini and Marianna (Reference Bassanini and Marianna2009, Figure 4) report an average job-destruction rate of about 8% per annum in some European countries (Germany, Finland, and Sweden). In their model applied to the Euro Area, Christoffel et al. (Reference Christoffel, Costain, de Walque, Kuester, Linzert, Millard and Pierrard2009a) use a quarterly rate of 6%. We fix the quarterly job destruction rate χ at 3% for the US and 2% for the EU15. The values for our quarterly χ’s may seem low compared to some of the figures above, but imply high values of χ over the 5-year period (45.62% in the US and 33.24% in the EU15) and are, therefore, reasonable. The bargaining power η of workers is set to the conventional value of 0.5 [see, e.g., Mortensen and Pissarides (Reference Mortensen and Pissarides1994)].

Following Den Haan et al. (Reference Den Haan, Ramey and Watson2000), we adopt the following constant returns-to-scale matching function:

$$\begin{equation}

M(V_{t}, \Omega _{t})=\frac{V_t\;\Omega _t}{(V_t^\nu +\Omega _t^\nu )^\frac{1}{\nu }}.

\end{equation}$$

$$\begin{equation}

M(V_{t}, \Omega _{t})=\frac{V_t\;\Omega _t}{(V_t^\nu +\Omega _t^\nu )^\frac{1}{\nu }}.

\end{equation}$$

The major advantage of this approach, compared to the standard Cobb–Douglas specification used in the literature, is that it guarantees matching probabilities of between zero and one for all Ω

t

and V

t

(0 < p

t

, q

t

< 1).Footnote

16

On the contrary, RBC models, which look at the effects of (smaller) shocks in the short term, tend to use the Cobb–Douglas specification. However, function (45) is more appropriate in our case, as labor markets are subject to demographic changes over a longer period. We assume that the matching-efficiency parameter ν is the same in the EU15 and the US. A similar ν in both regions implies that the matching process is the same in the US and the EU15 (although this does not exclude the possibility that other labor-market parameters, such as the cost of posting a vacancy, the job-destruction rate, and the generosity of unemployment benefits, may differ across regions). We calibrate ν and the two vacancy costs

$\mathsf{a}$

(one for each region) along with the three preference parameters d

n

, de

6, and de

7 (see above), to reproduce the activity rates for the groups aged 55–59 years and 60–64 years and the unemployment rates of workers aged 25–54 years, both in the EU15 and the US in 2005. We calculate these 2005 target values from OECD (2010a) data: they are shown in Table 2. Appendix C provides more detail on the calculation of the targets for the activity and early-retirement rates, and the calibration of the matching-efficiency parameter ν, worker bargaining power η, and the vacancy-cost parameter a.

$\mathsf{a}$

(one for each region) along with the three preference parameters d

n

, de

6, and de

7 (see above), to reproduce the activity rates for the groups aged 55–59 years and 60–64 years and the unemployment rates of workers aged 25–54 years, both in the EU15 and the US in 2005. We calculate these 2005 target values from OECD (2010a) data: they are shown in Table 2. Appendix C provides more detail on the calculation of the targets for the activity and early-retirement rates, and the calibration of the matching-efficiency parameter ν, worker bargaining power η, and the vacancy-cost parameter a.

6. BASELINE RESULTS

The baseline scenario illustrates the effects of the two exogenous changes discussed in Section 2 (and described in Section 5), those in LMIs and demographics, on the EU and US unemployment rates between 1960 and 2010. First, as shown in Figure 1 (panel c) and Figure 2 (panel a), LMIs became more generous until the early 2000s, with this rise being stronger in the EU15 than in the US. Second, in the US, population aging started in 2010, whereas in the EU15, this started much earlier (Figure 2, panel b). In Section 6.1, we produce some back-fitting exercises for the 1960–2010 period to see whether and how the model can explain the EU15–US unemployment puzzle. In Section 6.2, we focus on the evolution of capital flows, and in Section 6.3, we discuss possible changes to the way in which we represent capital flows. It is worth noting that 1960 and 2010 are sufficiently removed from the initial and the final steady states respectively to avoid any significant impact of the initial and terminal constraints on the observed dynamics.

It is moreover useful to separate out the individual effects of LMIs, demography, and capital flows. To do so, we consider different versions of the model as follows:

-

• Model LMI: here only LMIs change, holding demographics constant in a closed economy.

-

• Model LMID: this adds demographic changes to the above, but remains in a closed economy.

-

• Model LMIDO: this adds international capital flows (with perfect mobility) to the above.

To better grasp the extent to which each model can reproduce the unemployment rate in each country, we construct the metric

$$\begin{equation}

d^i=\frac{1}{11}\;\sum _{t=1960}^{2010}\;\sum _{c\in \lbrace \text{US},\,\text{EU}\rbrace }\;n_{t,c}\;\left|u^i_{t,c}-\tilde{u}_{t,c}\right|\;,

\end{equation}$$

$$\begin{equation}

d^i=\frac{1}{11}\;\sum _{t=1960}^{2010}\;\sum _{c\in \lbrace \text{US},\,\text{EU}\rbrace }\;n_{t,c}\;\left|u^i_{t,c}-\tilde{u}_{t,c}\right|\;,

\end{equation}$$

where i ∈ {LMI, LMID, LMIDO}, n

t, c

is the population share in country c at time t, ui

t, c

is the predicted unemployment rate in country c at time t in model i, and

$\tilde{u}_{t,c}$

is the effective unemployment rate in country c at time t. We also construct an analogous metric for the unemployment-rate gap:

$\tilde{u}_{t,c}$