1. Introduction

Medical technologies – comprising medical devices, pharmaceuticals, and diagnostic and treatment methods – are the cornerstone of modern medicine. While some have contributed to substantial improvements in medical outcomes and care, others may even jeopardise patients' safety (Rye and Kimberly, Reference Rye and Kimberly2007). It often takes years to distinguish the latter from the former and to determine their performance in routine practice (Callea et al., Reference Callea, Cavallo, Tarricone and Torbica2017). Due to considerable efforts and risks linked to research and development of medical technologies, new products are often more expensive than existing alternatives and are considered a decisive factor for high health expenditures (Willemé and Dumont, Reference Willemé and Dumont2015). Public health considerations on new technologies thus relate to the triangle of balancing patient access, safety and quality, and price setting. Worldwide, policy makers on statutory or insurance level, depending on the respective health system, are therefore responsible to weigh the potential benefits of ensuring timely access to new medical technologies against the risks of doing so in terms of safety and (cost-)effectiveness (Martelli and van den Brink, Reference Martelli and van den Brink2014; Sorenson and Drummond, Reference Sorenson and Drummond2014). The evaluation of a technology's cost-effectiveness allows for clear decion making in the case of increased effectiveness and decreased or equal costs compared to comperators (or even equal effectiveness and decreased costs). However, reimbursement decisions are more complex and depend on certain health system principles, if technologies show an increased effectivesness and higher costs (Black, Reference Black1990; Drummond et al., Reference Drummond, Sculpher, Claxton, Stoddart and Torrance2015). The reimbursement of technologies therefore plays a pivotal role for technology utilisation in health care while the particular design of the regulation depends on the kind of technology and usually differs between ambulatory and inpatient care.

Overall, the regulations on technology utilisation and coverage tend to facilitate an adoption in inpatient care, leading a majority of new technologies to enter the health system through the inpatient sector (Sorenson and Kanavos, Reference Sorenson and Kanavos2011). Hospitals have the highest share of expenditures in most health systems (Hatz et al., Reference Hatz, Schreyögg, Torbica, Boriani and Blankart2017), making technology adoption in inpatient care highly relevant from a system perspective. However, the immediate decision on the utilisation of respective medical technologies in inpatient care is taken on hospital level, where the seemingly same conditions cause some providers to adopt a new technology but others do not (Greenhalgh et al., Reference Greenhalgh, Robert, Macfarlane, Bate and Kyriakidou2004; Torbica and Cappellaro, Reference Torbica and Cappellaro2010; Sorenson and Kanavos, Reference Sorenson and Kanavos2011). High expenditures and increasing financial pressures such as prospective payment systems have led to an increased economic pressure for hospitals. A variety of studies have explored incentives of prospective payment systems and their effects on technology adoption while controlling for hospital characteristics. Results suggest that diagnosis-related group (DRG) payments incentivise hospitals to utilise those technologies that lead to lower costs per patient, while they negatively affect cost increasing new technologies (Romeo et al., Reference Romeo, Wagner and Lee1984; Lee and Waldman, Reference Lee and Waldman1985; Kesteloot and Voet, Reference Kesteloot and Voet1998; Scheller-Kreinsen et al., Reference Scheller-Kreinsen, Quentin and Busse2011).

With the aim to balance these financial disincentives for technologies that are currently not covered by health insurances – due to the time lack when introducing technologies in DRG systems – policy stakeholders use additional payment instruments to finance certain innovative technologies cost-neutrally. Studies investigating the utilisation of innovation payments in individual countries showed that these payments are overall correlated with adopting innovations (Bech et al., Reference Bech, Christiansen, Dunham, Lauridsen, Lyttkens, McDonald and McGuire2009; Bäumler, Reference Bäumler2013; Sorenson et al., Reference Sorenson, Drummond and Wilkinson2013; Wilkinson and Drummond, Reference Wilkinson and Drummond2014). To explore the effect of innovation payments, most of these studies investigate the uptake of one specific technology by the respective hospital departments in a certain region. However, many innovation payments are not paid to every hospital offering the service, but only to some providers based on negotiations. This is especially the case for separate payments and funding for cost outliers (Scheller-Kreinsen et al., Reference Scheller-Kreinsen, Quentin and Busse2011). As most of the previous studies analysed data regarding one medical device in one indication, our study evaluates a nationwide data set comprising all acute hospitals and the innovation payments for all diagnoses. More precisely, we aim at identifying factors at hospital and state levels that are associated with the agreement of innovation payments in German acute inpatient care as organisations are placed within special environments.

2. Background: innovation payments in Germany

Hospitals in Germany are permitted to use a newly approved technology before its benefits have been systematically assessed. This does not mean, however, that they will be reimbursed for its use. It takes approximately three years until a new technology is integrated in the DRG classification depending on the time when a new procedure code is established and depending on data availability to create a new DRG (Federal Association of Statutory Health Insurance Funds, 2016). Recognising that this time lag could hinder the adoption of potentially beneficial new technologies, policy-makers in Germany – as in many countries with DRG systems – have developed a system of innovation payments to provide additional funding for some of these technologies, if the price is above the existing DRG tariffs in inpatient care (Scheller-Kreinsen et al., Reference Scheller-Kreinsen, Quentin and Busse2011; Levaggi et al., Reference Levaggi, Moretto and Pertile2014; Sorenson et al., Reference Sorenson, Drummond, Torbica, Callea and Mateus2015). This system was established in 2005 and involves the so-called ‘NUB payments’, named after the German acronym for ‘New Diagnostic and Treatment Methods’ [Neue Untersuchungs- und Behandlungsmethoden, Section 6(2) KHEntgG, Hospital Payment Act]. From an international perspective, NUB payments can be classified as payments that are separate from the DRG system, involve additional funding (i.e. are paid on fee-for-service basis) and are negotiated locally (Scheller-Kreinsen et al., Reference Scheller-Kreinsen, Quentin and Busse2011; Sorenson et al., Reference Sorenson, Drummond and Wilkinson2013). We will refer to NUB payments as ‘innovation payments’ due to internationally different terms.

The process to receive the innovation payment consists of two steps. In a first step, a hospital submits a request to the German Institute for the Hospital Remuneration System (InEK, Institut für das Entgeltsystem im Krankenhaus). In its request, the hospital describes (1) the new technology and the features making it beneficial for patients, (2) the patients being treated, (3) additional staff and material costs and (4) the reason why the costs of the new technology are not appropriately covered by existing DRG tariffs. If the InEK decides that the technology satisfies the criteria for innovation payments, it designates the technology ‘Status 1’. In a second step, the hospital may subsequently negotiate a payment with representatives of the health insurances (Institut für das Entgeltsystem im Krankenhaus, 2015). This can take place as part of, or separately from, the annual budget negotiations between the hospital and the health insurances in the state within which the hospital is located. Health insurances are, however, not obliged to agree on a payment. The negotiated budget and innovation payments are valid for all insured patients treated at that hospital; this includes all statutory health insurances as well as all private health insurances (Loskamp et al., Reference Loskamp, Genett, Schaffer and Schulze-Ehring2017). Henschke et al. give a detailed introduction into this regulatory pathway (Henschke et al., Reference Henschke, Bäumler, Weid, Gaskins and Busse2010).

Innovation payments in Germany have received little research attention. To date, two commercial reports have used questionnaires and expert interviews to explore the importance of hospitals attached to innovation payments. One of these reports, commissioned by the German Medical Technology Association (BVMed), concluded that primarily university hospitals, large hospitals and hospitals with a medical specialisation considered innovation payments as a relevant funding source. The authors estimated that 40% of the payment requests that received approval for negotiations ultimately agreed a payment successfully with the health insurances (Blum and Offermanns, Reference Blum and Offermanns2009). The authors of the second report commissioned by Pfizer Pharma GmbH assessed based on a qualitative survey that hospitals valued innovation payments not only for financial reasons but as a marketing instrument for hospitals' innovativeness. Based on these findings, innovation payments were suggested to be especially relevant for large non-university hospitals (Wilke, Reference Wilke2007). However, we were unable to identify any studies that analysed secondary countrywide data to explore which factors might affect the likelihood of a hospital and health insurances contractually agreeing innovation payments.

3. Theoretical framework

Particularly in times of an increasing pace of innovations, technology adoption is a carefully considered decision (Lettieri and Masella, Reference Lettieri and Masella2009). Decision making is exacerbated by financial pressures based on the introduction of innovation payments. Identifying factors that explain differences in hospitals' adoption behaviour plays an important role in adoption research (Greenhalgh et al., Reference Greenhalgh, Robert, Macfarlane, Bate and Kyriakidou2004; Torbica and Cappellaro, Reference Torbica and Cappellaro2010; Sorenson and Kanavos, Reference Sorenson and Kanavos2011). According to our specific aim that focuses on examining hospitals' decision with regard to aggreeing innovation payments, Rogers' Innovation-Diffusion Theory, used in a variety of research fields, is used as a theoretical framework. It may be one of the most influential work to understand the comprehensive structure of adopting innovations, identifying three main sources that influence the adoption of innovations, namely the perception of innovation characteristics, the adopter characteristics and the contextual determinants also known as environmental determinants (Rogers, Reference Rogers2003, first published in 1962). Rogers additionally defines the steps of the decision-making process as knowledge, persuasion, decision, implementation and confirmation (Rogers, Reference Rogers2003). In the context of large complex organisations, this is accompanied by the division of duties as each step of technology adoption and assimilation may be executed by different people (Sáenz-Royo et al., Reference Sáenz-Royo, Gracia-Lázaro and Moreno2015), such as the treating physicians, chief physicians, hospital managers and controlling personnel (Kimberly and Evanisko, Reference Kimberly and Evanisko1981). The entity hospital as an organisation therefore depicts interactions beween different individuals. Furthermore, adoption theory suggests that technology adoption in hospitals depends on the kind of technology (Greer, Reference Greer1985). This is an important issue when focusing on different kinds of technologies. However, when focusing on medical technologies that are utilised in direct patient care – the so-called ‘medical-individualistic’ technologies in Greer's terms and that additionally exhibit similar characteristics such as being not adequately captured by DRG systems due to their novelty, technology characteristics might be neglected. We therefore focus on the role of organisational and environmantal determinants that play an essential role in technology adoption of hospitals (McCullough, Reference McCullough2008).

3.1 Organisational determinants

Organisational determinants of adopting innovations have been widely investigated. Previous research showed that internal organisational characteristics are associated with the adoption of innovations (Kimberly and Evanisko, Reference Kimberly and Evanisko1981; Greenhalgh et al., Reference Greenhalgh, Robert, Macfarlane, Bate and Kyriakidou2004; Rye and Kimberly, Reference Rye and Kimberly2007; Varabyova et al., Reference Varabyova, Blankart, Greer and Schreyögg2017). From the perspective of restricted resources, larger hospitals tend to have more complex resources in terms of technical equipment available in that hospital, and a better technological know-how (Weng et al., Reference Weng, Huang, Kuo, Huang and Huang2011). Additionally, there might be differences in the hospital's stance on new technologies. Large hospitals generally employ more administrative staff and have a separate finance and performance directorate (Blank and Valdmanis, Reference Blank and Valdmanis2015). Considering their regional importance, they may have a stronger negotiating position than smaller hospitals and may therefore be more successful at agreeing innovation payments.We therfore hypothesise that agreements on innovation payments will be positively influenced by hospital size.

Being a university hospital is likely to be associated with a greater willingness to adopt and develop new technologies given their teaching and research mission (Weng et al., Reference Weng, Huang, Kuo, Huang and Huang2011). With regard to the utilisation rate of new technologies, Mitchell et al. found that the proportion of MR imaging was higher in teaching hospitals compared with non-teaching hospitals (Mitchell et al., Reference Mitchell, Parker, Sunshine and Levin2002). Furthermore, evidence suggests that university hospitals may have a strong negotiating position with the health insurances (Blum and Offermanns, Reference Blum and Offermanns2009; Bäumler, Reference Bäumler2013; White et al., Reference White, Reschovsky and Bond2014). We therefore hypothesise that aggreements on innovation payments will be positively associated with the university status of a hospital.

As the mission of an organisation may affect strategic decision making with regard to the adoption of innovative technologies, for-profit organisations are the most market-orientated providers. Consequently, they may have higher incentives to use new technologies with the aim of attracting more patients (Banaszak-Holl et al., Reference Banaszak-Holl, Zinn and Mor1996). In the context of successful agreements on innovation payments, we hypothesise that for-profit hospitals have greater incentives to agree innovation payments due to their market orientation. However, evidence on the relationship between hospital ownership and the uptake of new technologies is mixed. The findings of several studies suggest that private for-profit hospitals adopt new technologies faster than other providers (Bäumler, Reference Bäumler2013), while Bech et al. (Reference Bech, Christiansen, Dunham, Lauridsen, Lyttkens, McDonald and McGuire2009) could not show that a higher share of private hospital beds was positively associated with procedure rates for new technologies.

There is some evidence to suggest that the uptake of new technologies may be associated with the specialisation of hospitals (Blum and Offermanns, Reference Blum and Offermanns2009; Bonastre et al., Reference Bonastre, Chevalier, van der Laan, Delibes and de Pouvourville2014; Augurzky et al., Reference Augurzky, Pilny and Wübker2015). However, one has to bear in mind, that hospitals are considered as specialised in different ways. (I) If a hospital treats a large share of cases in one field (Daidone and D'Amico, Reference Daidone and D'Amico2009; Herwartz and Strumann, Reference Herwartz and Strumann2012; Lindlbauer and Schreyögg, Reference Lindlbauer and Schreyögg2014; Kim et al., Reference Kim, Kim, Woo and Hyun2015) it might be specialised due to the concentration of cases in terms of a narrow range of services. (II) Hospitals with cases assigned to a high degree of severity are also considered to be specialised (Farley and Hogan, Reference Farley and Hogan1990; Zwanziger et al., Reference Zwanziger, Melnick and Simonson1996; Bonastre et al., Reference Bonastre, Chevalier, van der Laan, Delibes and de Pouvourville2014). There are intensive discussions in scientific research as the first definition might not adequately explain specialisation, e.g. when using the hospital level. University hospitals may have many cases in one clinical field while their share of cases compared with all other cases might be small. We therefore expect a negative association for specialisation in terms of concentration which is defined according to the range of services. Regarding a hospital's specialisation in terms of a high degree of severity, one can assume that the uptake of new technologies tends to be quicker and more comprehensive in university hospitals compared with a general hospital, making it worthwhile for the former to apply for extra funding. We hypothesise that a high severity level is associated with agreeing innovation payments.

3.2 Environmental determinants

In addition, a high degree of competition in the vicinity of a hospital may act as an incentive to adopt new technologies (Castro et al., Reference Castro, Calogero, Pignataro and Rizzo2014; Blank and Valdmanis, Reference Blank and Valdmanis2015). Many studies also analyse the effects of competition on hospitals' patient volume, average length of stay, costs of care and efficiency (Robinson and Luft, Reference Robinson and Luft1985; Schmid and Ulrich, Reference Schmid and Ulrich2012; Tiemann et al., Reference Tiemann, Schreyögg and Busse2012). The regulatory and competitive environment in the German hospital sector has been part of consolidation and reorganisation processes (Schmid and Ulrich, Reference Schmid and Ulrich2012). Overcapacities in urban areas result in increasing competitive pressure (Tiemann and Schreyögg, Reference Tiemann and Schreyögg2009). Therefore, it is likely to assume that high competition leads to successful negotiations of innovation payments to further increase hospitals' competitiveness in terms of attracting more patients. Robinson and Luft concluded that higher costs of hospitals operating in highly competetive areas have been a result of higher demand in wealthy areas for technologically sophisticated and expensive clinical medicine (Robinson and Luft, Reference Robinson and Luft1985).

Lastly, the bed occupancy rate is a measure of the overall supply of and demand for hospital services within a state (Dayhoff and Cromwell, Reference Dayhoff and Cromwell1993). It is the share of occupied inpatient bed days divided by the available inpatient bed days over a year in each state. With regard to innovation payments, hospitals in a state with a low bed occupancy rate might have a greater incentive to offer additional services compared with a hospital with a high occupancy rate and thus request more funding.

While German innovation payments are regulated by federal law, we assume they are implemented differently in each of Germany's 16 federal states. Indeed, decisions on hospital planning and financing are the responsibility of the states rather than of the federal government. Hospitals' operational costs are covered primarily by DRG payments made by statutory and private health insurers, while capital investment is primarily financed from state budgets. Furthermore, the representatives of health insurances responsible for negotiating innovation payments differ between states. In short, hospitals in Germany operate within a state-specific financial and political context. We hypothesise that the variation in hospitals agreeing innovation payments can in part be explained by hospitals being clustered in the 16 states in Germany because of distinct financial and political circumstances.

With these points in mind, we hypothesise that:

(a) the odds of agreeing innovation payments with health insurances vary considerably among hospitals;

(b) this variation can be explained in part by hospital characteristics; and

(c) in part by hospitals being clustered in the 16 states in Germany because of distinct financial and political circumstances.

4. Materials and methods

4.1 Data

We conducted an empirical analysis of all acute hospitals operating within the G-DRG system. The data set was compiled by the Scientific Institute of the AOK (WIdO, Wissenschaftliches Institut der AOK) as an appendix to its annual hospital report in 2015 (Klauber et al., Reference Klauber, Geraedts, Friedrich and Wasem2015). The data stem mainly from the annual hospital budget agreements. The WIdO supplemented this data set with data from quality assurance records and emails that the health insurances must send to InEK to inform it that an innovation payment has been agreed.

The data set encompasses all acute hospitals that treat patients insured by health insurance – i.e. hospitals forming part of the hospital plans of the states and hospitals with provision contracts. In the data, a hospital is defined as the entity with which a budget agreement has been made. In cases where a chain or network of hospitals within one state is registered as one institution (i.e. with just one institutional code), it is considered to be one hospital. We obtained data on variables at the state level from the German Federal Statistical Office. All data are presented for the year 2013. We used Stata 12.1 to estimate our regression model.

4.2 Model specification

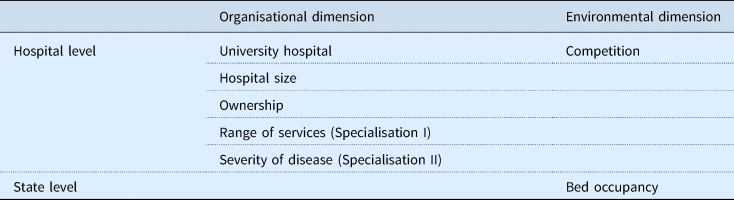

The outcome variable in our statistical model was dichotomous, assuming a value of 1 if one or more innovation payments were successfully negotiated between a hospital and the health insurances in 2013 and 0 otherwise. We undertook a multilevel analysis with hospitals clustered in states to consider the distinct financial and political contexts within which hospitals operate in a state. Based on the dimensions relevant for technology adoption, we considered relevant covariates corresponding to the organisational and the environmental dimensions. We estimated the following explanatory variables measured on hospital and state level, derivered from the framework described above (see Table 1).

Table 1. Explanatory variables by dimension

We operationalised the explanatory variables as decribed in the following. The variable university status is dichotomous in our model, assuming a value of 1 if a hospital had university status and 0 if not.

Hospital size is operationalised by the number of hospital beds (<50; 50–199; 200–499; 500–999; ⩾1000 beds), with the smallest category serving as reference. In line with the German Federal Statistical Office (DESTATIS), we distinguish between three types of hospital ownership (Bölt and Graf, Reference Bölt and Graf2012) by including two dummy variables, one for not-for-profit and one for private for-profit ownership, with public ownership as the reference category.

Since specialisation is not observable but needs to be interpreted from other data, there have been various attempts to find proxy variables to measure specialisation: The information theory index (ITI) and the gini coefficient of the hospital's major diagnostic categories or DRGs consider a hospital specialised when it treats a large share of cases in one field, focusing on the relative number of patient cases (Daidone and D'Amico, Reference Daidone and D'Amico2009; Herwartz and Strumann, Reference Herwartz and Strumann2012; Lindlbauer and Schreyögg, Reference Lindlbauer and Schreyögg2014; Kim et al., Reference Kim, Kim, Woo and Hyun2015). Besides that, a distance measure of a hospital's case-mix index, depicting the distance from a hospital's level of severity to a baseline, has been used to measure specialisation in terms of severity level. Hospitals with cases assigned to a higher degree of severity compared with a baseline are considered to be specialised following this definition (Farley and Hogan, Reference Farley and Hogan1990; Zwanziger et al., Reference Zwanziger, Melnick and Simonson1996; Bonastre et al., Reference Bonastre, Chevalier, van der Laan, Delibes and de Pouvourville2014). Selecting an appropriate measurement thus depends on the contextual notion of specialisation. In the context of adoption decisions of new technologies, we use both definitions: (I) the specialisation as the concentration in terms of a narrow range of services and (II) the level of severity of the treated cases. To account for (I) the range of services within a hospital, the Gini coefficient measures the extent to which a hospital's distribution of base DRGs deviates from an equal distribution of the entire catalogue of base DRGs (Augurzky et al., Reference Augurzky, Pilny and Wübker2015; Klauber et al., Reference Klauber, Geraedts, Friedrich and Wasem2015). The Gini coefficient assumes values between 0 and 1, with higher values suggesting a higher degree of specialisation (narrow range of services). A Gini coefficient of 0 would mean that a hospital's services are spread evenly across all base DRGs and the hospital would be considered unspecialised (wide range of services). In contrast, a Gini coefficient of 1 would indicate a maximum degree of specialisation as all services would be assigned to one base DRG. To account for (II) a hospital's level of severity, we assume that hospitals with a higher case-mix index have a higher level of sophistication. We thus measure this as a distance of the hospital's case-mix index deviating from the state mean (≥20.00%, 10.00 to 19.99%, 0.00 to 9.99%, −10.00 to −0.01%, −20.00 to −10.01%, <−20%).

In addition, the degree of competition in commercial markets is measured by the use of the Herfindahl–Hirschman Index (HHI). By summing the squared market shares of all hospitals within a radius of 10 km, the HHI represents not only the number of competitors within a market but also ‘the equity of distribution of market share’ (Sethi et al., Reference Sethi, Henry, Hevelone, Lipsitz, Belkin and Nguyen2013). The HHI ranges from 0 (highly competitive) to 1 (monopoly).

Lastly, the bed occupancy rate is reflected by the share of occupied inpatient bed days divided by the available inpatient bed days over a year in each state.

4.3 Statistical analysis

We estimated two-level logistic regression models with state-level fixed effects (random intercept models) to consider clustering of hospitals within states. State-level variance in agreed innovation payments was assessed by estimating an unconditioned model (null model). It may be written as:

$${\rm log}it(\pi _{ij}) = \Pr (y_{ij} = 1) = \beta _0 + u_j,$$

$${\rm log}it(\pi _{ij}) = \Pr (y_{ij} = 1) = \beta _0 + u_j,$$where y ij is the dependent variable (subscript i referring to the hospital and subscript j to the state), ß 0 is the intercept and u j the state-level random effect, assumed to be independent from one another and normally distributed with a mean of zero.

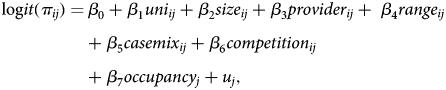

In the next step, we added the explanatory variables to the model:

$$\eqalign{{\rm log}it(\pi _{ij}) = &\,\beta _0 + \beta _1uni_{ij} + \beta _2size_{ij} + \beta _3provider_{ij} + \; \beta _4range_{ij} \cr & + \beta _5casemix_{ij} + \beta _6competition_{ij} \cr & + \beta _7occupancy_j + u_j,} $$

$$\eqalign{{\rm log}it(\pi _{ij}) = &\,\beta _0 + \beta _1uni_{ij} + \beta _2size_{ij} + \beta _3provider_{ij} + \; \beta _4range_{ij} \cr & + \beta _5casemix_{ij} + \beta _6competition_{ij} \cr & + \beta _7occupancy_j + u_j,} $$where ß 0 is the intercept, ß 1–ß 6 are the hospital parameters and ß 7 is a state parameter associated with the covariates, and u j the random error for the state level. We conducted the Hausman test with the bed occupancy variable as random effect to determine that the fixed effect does not capture a part of the bed occupancy. According to the results do not justify using random effects. The goodness of fit of the models was compared using the likelihood ratio test, estimating how much more probable the data were in the fitted model compared with the null model.

5. Results

5.1 Descriptive statistics

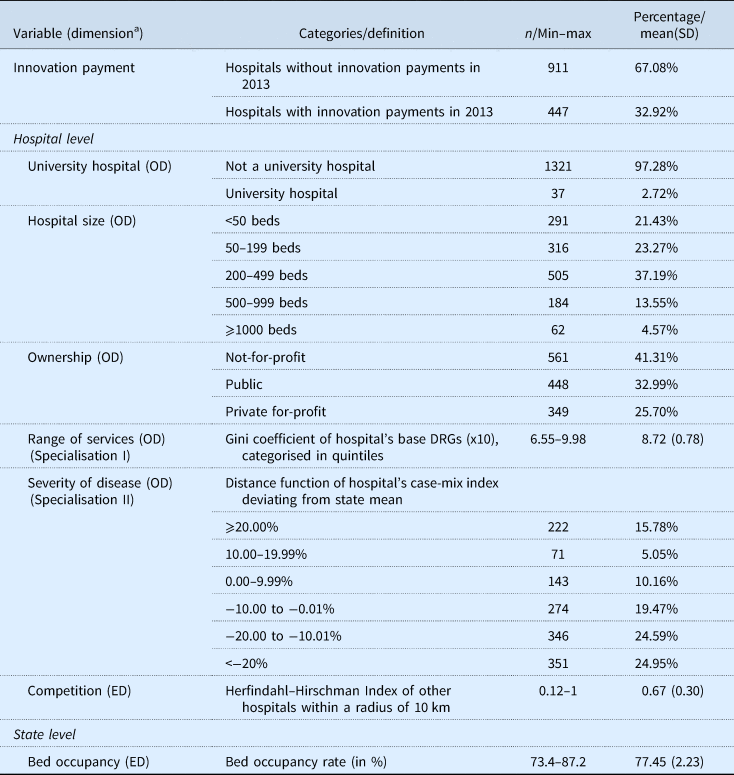

Our analysis included 1358 hospitals in Germany, for which we had complete data on the chosen variables. Of all the hospitals in our sample, 2.7% had university status. The most common hospitals were those with 200–499 beds (37.2%) and with not-for-profit ownership (41.3%). Table 2 gives a summary of the descriptive statistics.

Table 2. Variable definitions and descriptive statistics (n = 1358)

Note: Hospitals were included in the study if details on all considered categories were available in the hospital index (information was missing in 174 out of 1532 cases.

OD, organisational dimention; ED, environmental dimension.

a Dimension: variables and dimensions are part of Table 1.

In total, 32.9% of the hospitals in our sample agreed one or more innovation payments with the health insurances in 2013 (447 of 1358 hospitals). Of the university hospitals, 91.9% successfully negotiated innovation payments compared with 31.3% of the non-university hospitals.

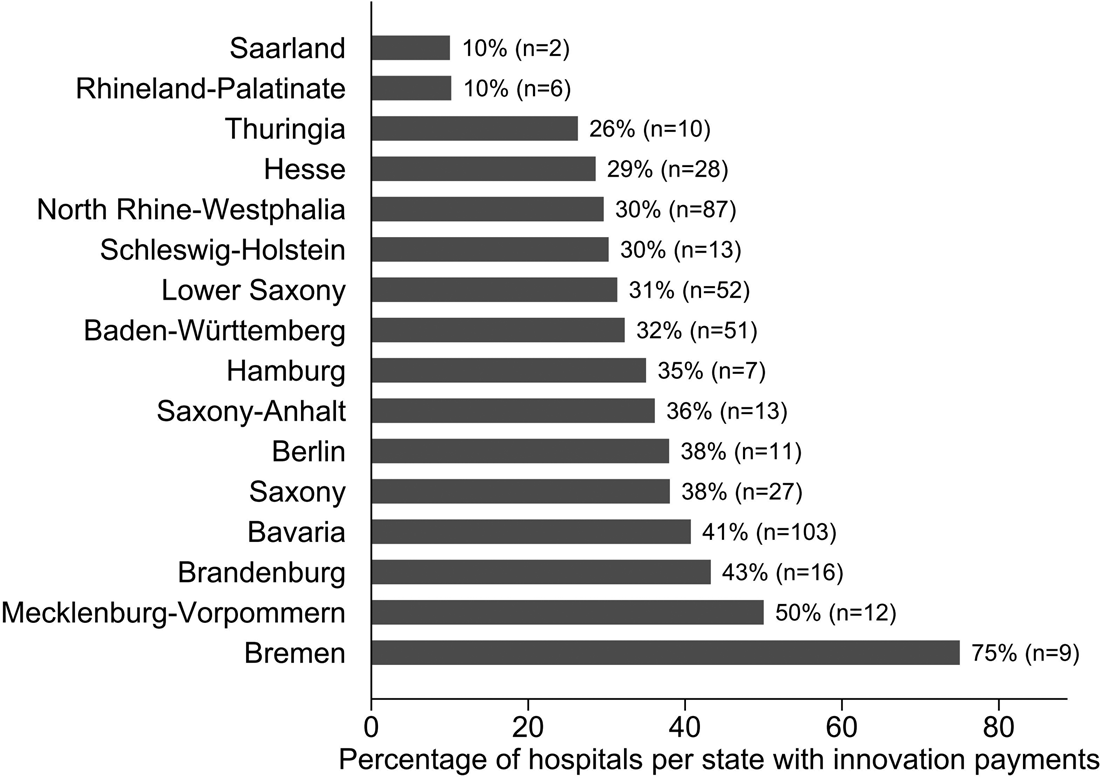

The share of hospitals that successfully negotiated innovation payments varied considerably among the states. In Rhineland-Palatinate and Saarland, for example, 10.0% of hospitals agreed innovation payments with the health insurances. At the other end of the spectrum is the city-state of Bremen, where 75.0% of hospitals successfully negotiated innovation payments that same year. Figure 1 gives descriptive statistics on the variation among the 16 states in Germany.

Figure 1. Percentage of hospitals in each of Germany's 16 states that agreed innovation payments with the sickness funds in 2013.

5.2 Factors that explain the agreement of innovation payments

We estimated a null model (Model I) first to test our observation of clustering on state level. The estimate for the intercept produces a mean of 0.38 (95% CI 0.18–0.82) and the intraclass-correlation coefficient, calculated as the ratio of the between variance to the total variance, is 0.042. This coefficient suggests that observations of hospitals within the same region are not fully independent from one another but clustered in states. As even small levels of dependence can lead to biased results (Cohen, Reference Cohen2010), we chose to investigate variation between the states in our further models by including state-specific explanatory variables. We added the hospital and state variables into the analysis in the next step (Model II). The detailed results of our two regression models are provided in Table 3.

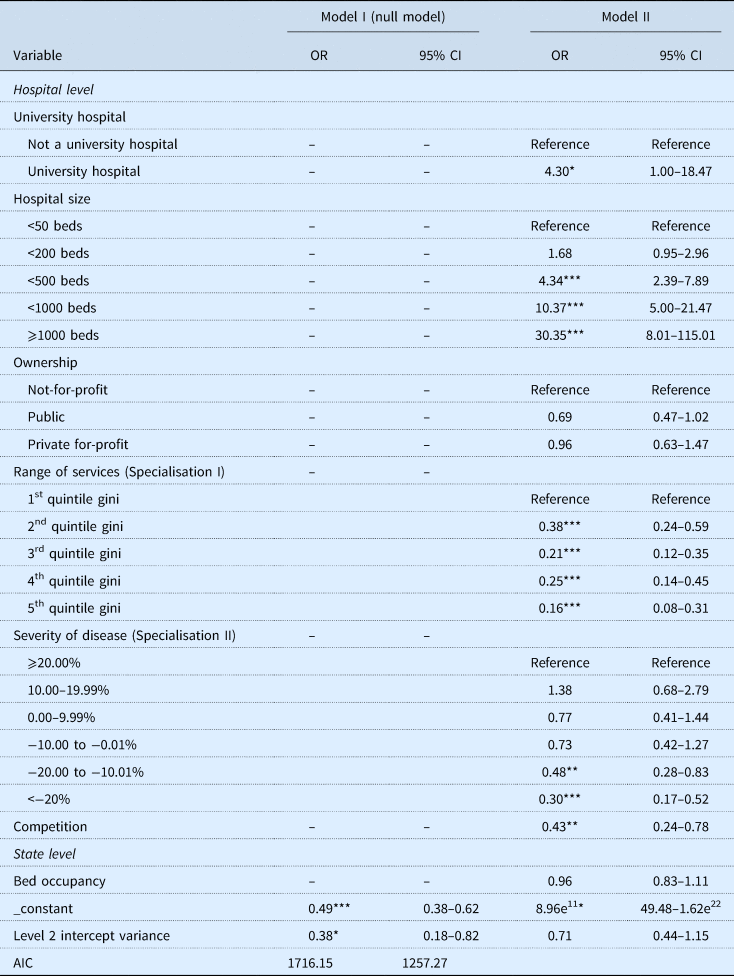

Table 3. Odds ratios and 95% confidence intervals for hospitals agreeing innovation payments in 2013

Note: ***p < 0.001, **p < 0.01, *p ⩽ 0.05.

When the other variables were held constant, the status as university hospital was associated with an odds ratio of 4.30 (95% CI 1.00–18.47) compared with non-university hospitals. Furthermore, large hospitals had greater odds of agreeing innovation payments compared with small hospitals. The odds ratio rose as the number of beds increased, reaching 30.35 (95% CI 8.01–115.01) for hospitals with at least 1000 beds compared with hospitals with fewer than 50 beds (reference). The odds of agreeing innovation payments were lower for public hospitals (0.69, 95% CI 0.47–1.02) and slightly lower for private for-profit hospitals (0.96, 95% CI 0.63–1.47) than for not-for-profit hospitals. The Gini coefficient of base DRGs (OR 0.38; 95% CI 0.24–0.59 second quintile compared with first quintile) suggests that the odds of agreeing innovation payments decreases with increasing centralisation in services. Opposed to this, we estimate a positive correlation between hospitals with a higher case-mix index than state mean and the chance of successfully negotiating innovation payments. Estimating the influence of competition and market share on the agreement of innovation payments resulted in an odds ratio of 0.43 (95% CI 0.24–0.78).

On state level, the bed occupancy rate was also negatively associated with agreeing innovation payments. The estimated odds ratio of 0.96 (95% CI 0.83–1.11) suggests that the odds of agreeing innovation payments decreases by 0.04 for each per cent that the bed occupancy rate increases.

6. Discussion

One criterion for the success of health systems is their ability to innovate. Health policy making thus balances patient access, safety and quality of innovative health technologies, based on coverage decisions and price setting mechanisms. The implementation of temporary innovation payments aimed at balancing the disincentive of prospective payment systems to use new more expensive technologies compared to those integrated in the current DRG system (Scheller-Kreinsen et al., Reference Scheller-Kreinsen, Quentin and Busse2011). In order to assess in how far policy making achieves the aim to bridge the gap between the introduction of a new medical technology and its reimbursement through DRGs, we examined hospital and state variables that might be associated with receiving innovation payments. Each variable is assigned to the organisational and environmental dimension of Rogers' framework (Rogers, Reference Rogers2003). However, variables of the product dimension which are also a part of Rogers' framework were not included in analyses as technologies concerned exhibit similar characteristics such as being not adequately captured by DRG systems due to their novelty.

The results show that hospitals with certain characteristics of the organisational and environmental dimension have a higher likelihood to access innovation payments as additional source of financing than others. In accordance with literature on this subject, a substantial share of the variance was explained on hospital level and a smaller one on state level. We found that hospitals had greater odds to agree innovation payments if they were large, had university status and were located in a region with high competition, which is consistent with previous studies (Bech et al., Reference Bech, Christiansen, Dunham, Lauridsen, Lyttkens, McDonald and McGuire2009; Blum and Offermanns, Reference Blum and Offermanns2009; Bäumler, Reference Bäumler2013). One explanation for the effect of hospital size may be found in the ability of larger hospitals to employ more staff skilled in medical finance and performance, facilitating the elaborate process of requesting innovation payments. For smaller hospitals, it may be more efficient to avoid this process altogether and use new technologies only in exceptional cases and without adequate reimbursement. Moreover, it is plausible that larger and university hospitals have more power to negotiate innovation payments (Blum and Offermanns, Reference Blum and Offermanns2009). Additionally, university hospitals are commissioned to undertake teaching and research activities (as described in the individual state laws). The positive relationship between innovation payments and the level of competition in a hospital's vicinity suggests that the presence of competing hospitals may serve as incentive to offer new procedures and technologies. This complements the notion that the demand for, and use of, medical services increases with their supply (Nolting et al., Reference Nolting, Zich, Deckenbach, Gottberg, Lottmann, Klemperer, Grote-Westrick and Schwenk2011; Schreyögg et al., Reference Schreyögg, Bäuml, Krämer, Dette, Busse and Geissler2014). One explanation may be that innovation payments serve as a marketing instrument, allowing hospitals to stand apart from their regional competitors. Because it has been an explicit political goal to foster competition in the German health system, these effects can be classified as intended consequences of the payment instrument (Knieps, Reference Knieps2009).

We hypothesised that when a hospital serves as a specialist centre for a certain diagnosis, this specialisation might be linked to the use of new technologies. Our estimations suggest that the odds of agreeing innovation payments were lower for hospitals with a narrow range of services (i.e. high concentration of cases). One reason may be that a centralisation of a hospital's services on very few DRGs entails that there are only few innovation payments eligible for funding. There may be years in which no innovation payment exists for this area of specialisation. However, this information is not included in our data set. As the Gini coefficient only focuses on centralisation, hospitals with a wide range of services but with a high level of severity in some of their fields may be specialised despite a low Gini coefficient, such as some university hospitals. We thus also estimated the effect of hospitals' level of severity through the hospital case-mix index as distance from the state mean. Hospitals treating more severe patient cases are more likely to agree innovation payments. Interestingly, after adjusting for case-mix, the chance to agree innovation payments is slightly smaller for private for-profit hospitals than for not-for-profit hospitals. If the regression is not adjusted for the case-mix index, however, private hospitals seem to adopt innovation payments faster, which is actually due to a larger average case-mix (Bonastre et al., Reference Bonastre, Chevalier, van der Laan, Delibes and de Pouvourville2014).

Overall, the results suggest that variables of the organisational dimension (e.g. university status, hospital size) and the environmental dimension (e.g. competition, bed occupancy) are associated with negotiating innovation payments. In particular, hospitals in rural areas with a low competition and those with a low bed occupancy do not adopt new technologies in the same way as hospitals in an area of high hospital competition and a high bed occupancy. Patient access to new technologies can thus be restricted in rural areas with few competing hospitals in the vicinity and in small hospitals. Hospitals may not innovate due to uncertainities and risk combined with the use of new medical devices, e.g. limited skills and a lack of experience that might cause risks for patients and users (Altenstetter, Reference Altenstetter1996).

The effects of variables might be politically desired: especially large hospitals and those with research focus negotiated innovation payments. Due to their responsibility for testing new therapies at an early point in time and because of their elaborate medical hierarchies and structures, patient safety may in average be higher if new technologies are utilised and reimbursed in large and university hospitals first. In addition, when a new technology is used frequently by one entity, adverse effects and dangers may faster become evident. This is especially relevant since requirements for market access are relatively low for medical devices in the European Union (Hatz et al., Reference Hatz, Schreyögg, Torbica, Boriani and Blankart2017). This raises the question in how far new technologies should be assessed regarding patient value in terms of effectiveness and safety issues while being reimbursed through innovation payments. Starting in 2016, the German government has implemented an early benefit assessment for certain procedures, when an innovation payment is requested. The federal joint committee now assesses the clinical effectiveness, risks and potentials for highly invasive procedures using ‘high-risk’ medical devices (i.e. medical device of risk class IIb or III or active implantable medical devices exhibiting a novel theoretical–scientific concept) and decides if patient value has been proven sufficiently.

Besides these results, our study has certain limitations regarding the data set. First, regarding the dependent variable, a more robust analysis would be possible if more details on the number of technologies accepted for payments were available. Additionally, details on the number of innovation payments per hospital, the number of applications per hospital, and the process and outcomes of hospitals' annual budget negotiations would contribute to an analysis considering more specific variables. However, these data are not publicly available. Nevertheless, to our knowledge, this data set is the best available resource covering a nationwide data set of innovation payments. Furthermore, it is the first study using a nationwide data set that includes all hospitals being allowed to negotiate innovation payments with health insurers, i.e. all technologies assessed positively in the process of innovation payment are included. While it is unlikely that a hospital would incorrectly record to have received a payment when it had not, it is conceivable that the receipt of an innovation payment is not always included in a hospital's records of its main budget negotiations because innovation payments can be agreed outside of these. To correct for this, the WIdO used data from quality assurance records and the emails that health insurances must send to InEK to inform it that innovation payments have been agreed with a hospital to verfify the information on innovation payments. Based on these limitations and based on the fact that health insurances are not obliged to negotiate innovation payments, our outcome variable captures two steps: (1) a hospital's successful request to InEK allowing it to negotiate a payment and (2) the successfull negotiation of a payment with the health insurances. Lastly, due to the limitations of the data set, we were unable to consider interactions beween different individuals within the entity of hospitals as an organisation. Since most countries with DRG systems use some form of time-limited innovation payments to encourage innovation and improve access to new technologies, we recommend that similar studies be conducted in other countries, preferably using data from all hospitals and all diagnoses, to research the matter in other prospective payment systems. As innovation payments are time-limited and most new technologies are integrated into the DRG system over time by splitting DRGs or introducing supplementary payments, further studies should investigate the link between innovation payments and permanent reimbursement in relation to the technology's benefits.

7. Conclusion

Evidence shows that remuneration systems such as the DRG system affect decision making of hospitals. In order to balance timely utilisation of new technologies and cost coverage, policy makers use temporary innovation payments to compensate disincentives inherent in the DRG system. Our findings shed light on the effect of hospital and state characteristics for agreeing innovation payments in German inpatient care. We thereby reveal implicit incentives of the reimbursement mechanism. The results might be of interest for the German government as well as for stakeholders in the context of prospective payment systems.

Key findings of this study are that policy making generally compensates disincentives of the DRG system by disbursing innovation payments. Patient safety may be implicitly fostered by favouring university hospitals and large hospitals to use new technologies. However, the innovation payments may impede patient access in rural areas since hospitals in regions with low competition have a smaller chance to receive innovation payments. This shows that the tradeoff between patient access and safety requires an adequate balance, which could be incentivised by financing mechanisms. Our study shows an implicit self-controlled selection of hospitals receiving innovation payments. Policy makers should instead choose a more direct and transparent process of distributing innovation payments in prospective payment systems. They should probably consider which hospitals are most suitable to generate further evidence on the effectiveness of new medical technologies to link safety issues with patient access regarding the use of new medical technologies.

Acknowledgements

The authors thank for the constructive and positive feedback from the participants at the EuHEA Conference in Hamburg where the study was presented. Also, we want to thank for the advice from Professor Martin Siegel. The first author receives a scholarship from Cusanuswerk, the episcopal scholarship foundation. The project was partly funded through the Berlin Centre for Health Economics Research by the German Federal Ministry of Education and Research (grant no. 01EH1604A).

Conflict of interest

None.